1 Source: Goldman Sachs Asset management. As of December 2020. See more explanations on the methodology below the table in the section How Risky is it to Ignore China Bonds in a Global Aggregate Bond Portfolio?

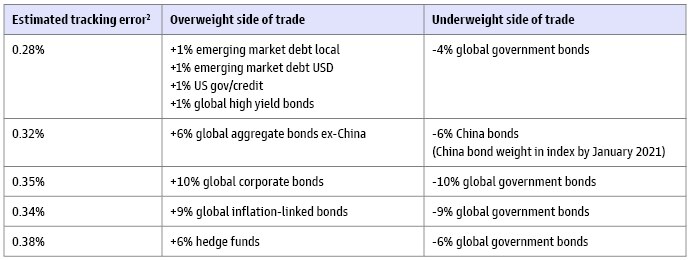

2 Source: The figures published here are estimated and unaudited as of December 2020, and are subject to potentially significant revisions over time. Actual tracking error may vary significantly from the information presented above.

3 Source: Haver, IMF and GSAM. GDP data are PPP measures (current international dollars). Data as of March 29, 2022, using IMF WEO figures from October 2021 projections. All developed nations as categorised by the IMF.

4 Source: IMF and Goldman Sachs Asset Management. Percentage changes are in real GDP. Data as of December 31, 2021.

5 Source: Goldman Sachs Asset Management. As of March 30, 2022. Assuming China equities represent 1/3 of the MSCI Emerging market equities index.

6 Source: Bloomberg and Goldman Sachs Asset Management. Correlations on weekly returns for the last 5 years (Dec-2016 to Dec 2021), as of December 31, 2021.

7 Source: Bloomberg and Goldman Sachs Asset Management. As of March 30, 2022.

8 Source: FTSE and GSAM. As of March 30, 2022.

Disclosures

Glossary:

Correlation is a statistic that measures the degree to which two variables move in relation to each other which has a value that must fall between -1.0 and +1.0.

The Bloomberg Global Aggregate Bond Index measures global investment grade debt from 24 local currency markets, including treasury, government related, corporate, and securitized fixed rated bonds from both developed and merging market issuers.

The FTSE World Government Bond Index (FTSE WGBI) measures exposure to the global sovereign fixed income market, the index measures the performance of fixed-rate, local currency, investment-grade sovereign bonds.

The JPMorgan GBI-EM Index is an unmanaged index tracking foreign currency denominated debt instruments of emerging markets.

The FTSE Goldman Sachs China Government Bond Index measures the performance of Chinese Yuan-denominated, fixed-rate government bonds issued in mainland China. Any bonds with maturity greater than 30 years from issuance are excluded from the index.

Risk Considerations

All investing involves risk.

Bonds are subject to interest rate, price and credit risks. Prices tend to be inversely affected by changes in interest rates.

Investments in foreign securities entail special risks such as currency, political, economic, and market risks. These risks are heightened in emerging markets. Emerging markets securities may be less liquid and more volatile and are subject to a number of additional risks, including but not limited to currency fluctuations and political instability.

The currency market affords investors a substantial degree of leverage. This leverage presents the potential for substantial profits but also entails a high degree of risk including the risk that losses may be similarly substantial. Such transactions are considered suitable only for investors who are experienced in transactions of that kind. Currency fluctuations will also affect the value of an investment.

General Disclosures

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Tracking Error (TE) is one possible measurement of the dispersion of a portfolio’s returns from its stated benchmark. More specifically, it is the standard deviation of such excess returns. TE figures are representations of statistical expectations falling within “normal” distributions of return patterns. Normal statistical distributions of returns suggests that approximately two thirds of the time the annual gross returns of the accounts will lie in a range equal to the benchmark return plus or minus the TE if the market behaves in a manner suggested by historical returns. Targeted TE therefore applies statistical probabilities (and the language of uncertainty) and so cannot be predictive of actual results. In addition, past tracking error is not indicative of future TE and there can be no assurance that the TE actually reflected in your accounts will be at levels either specified in the investment objectives or suggested by our forecasts.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices. The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources. This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA):This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), Goldman Sachs Asset Management, LP (GSAMLP) or Goldman Sachs & Co. LLC (GSCo). Both GSCo and GSAMLP are regulated by the US Securities and Exchange Commission under US laws, which differ from Australian laws. Both GSI and GSAMI are regulated by the Financial Conduct Authority and GSI is authorized by the Prudential Regulation Authority under UK laws, which differ from Australian laws. GSI, GSAMI, GSCo, and GSAMLP are all exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences. Any financial services given to any person by GSI, GSAMI, GSCo or GSAMLP by distributing this document in Australia are provided to such persons pursuant to ASIC Class Orders 03/1099 and 03/1100. No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

Confidentiality

No part of this material may, without by Goldman Sachs Asset Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

280109-OTU-1623412