October 6, 2022 |

GSAM Connect

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsOctober 11, 2022 | 6 Minute Read

For the past decade, investors have benefitted from an environment of relatively stable prices, falling interest rates, rising corporate profits, and manageable volatility. The annualized return on the S&P 500 Index over the last 10 years, for example, was approximately 12 percent as of September 26, 2022. In these conditions, the objective was simple: get invested and stay invested. The precise mix of assets was less important.

We’re in a different world now. Rates have been rising rapidly with inflation, growth has been slowing, profit margins appear to have peaked and volatility has been elevated. Today, what investors own matters more. This is a market that we believe calls for bottom-up portfolio construction and active management. It’s a market that has been rewarding profits over revenues, and may reward managers who embrace an active strategy, provide exposure to public and private assets, or can add value through tax management.

At the recent Goldman Sachs Asset Management Professional Investor Forum, our portfolio managers shared a few thoughts about portfolio construction in a market that is slowly settling into what appears to be a new era.

Generating steady public equity returns has become more challenging against today’s economic backdrop. Yet we believe there are opportunities in strong companies that offer attractive valuations. To make the most of them, investors will need to stay invested, stay active—passive strategies are unlikely to do as well in the coming decade as they did in the prior one—and stay balanced across market capitalization, style and region.

An immediate challenge will be inflation, which is running near a 40-year high. In this environment, we believe investors should prioritize profits over revenue and consider value-oriented strategies, which tend to outperform growth when interest rates are rising. Value has higher exposure to sectors that may act as an inflation hedge and benefit from higher rates, including financials and real assets such as energy and real estate. There are potential opportunities in Europe as well, which has more value exposure than the US. For instance, the MSCI EAFE Index has roughly 30% exposure to real assets, compared to about 20% for the S&P 500 as of September 2022 and the MSCI EAFE Value Index has outperformed the S&P 500 year to date. Long duration growth stocks in sectors such as information technology and communication services have struggled as higher rates erode future cash flows now discounted back to the present at higher rates. That doesn’t mean growth stocks don’t deserve a place in a diversified portfolio. But it does mean investors may need more balance between the two styles than they’ve had in the past.

Equity investors must also prepare for the risk that central bank tightening pushes major economies into recession. We believe this calls for an active approach that can zero in on companies with pricing power. Active managers can identify companies most likely to benefit from current conditions and avoid those that are most vulnerable.

Quantitative equity strategies can also help investors stay invested with a defensive tilt. For example, we see opportunities in buy-write strategies that typically involve investing in a basket of high-dividend paying equities in the S&P 500. That’s the “buy” part. This approach then seeks to generate additional income by selling—or “writing”—call options giving other investors the right to purchase those shares at a fixed price in exchange for a premium.

Exposure to liquid alternatives, which offer hedge-fund like characteristics in a liquid, publicly-traded vehicle, may also help to reduce the effects of equity market drawdowns.

If nothing else, today’s macroeconomic conditions and policy prescriptions have done what few things could over the past decade: they’ve put the income back in fixed income. Most major developed market yield curves are inverted, but investors are being compensated for investing in bonds in a way that we have not seen for roughly a decade. We think this offers investors an opportunity to do three things: get fixed income allocations back to neutral, increase income potential and rebalance their overall asset allocations.

First, we believe investors have nothing to fear from duration. Current yields on high quality securities make it easier to reduce overweight positions in lower-quality credit while locking in attractive income; at roughly 4.08% as of October 4th, 2022, two-year US Treasuries offer significant income per unit of duration. This will look even more attractive if the long-term real, inflation-adjusted rate of roughly 2 percent declines in the decades ahead, as we suspect it may amid slowing US population and productivity growth. It’s a similar story for quality investment-grade corporate debt, some of which offers yields above 5 percent for five-year maturities.

In fact, yields have climbed high enough, in our view, to consider rebalancing overall allocations by shifting some capital back to fixed income from risk-seeking assets such as equities. This would help address recent under-allocation to core fixed income in many portfolios, making them more diversified while boosting their income-generating potential.

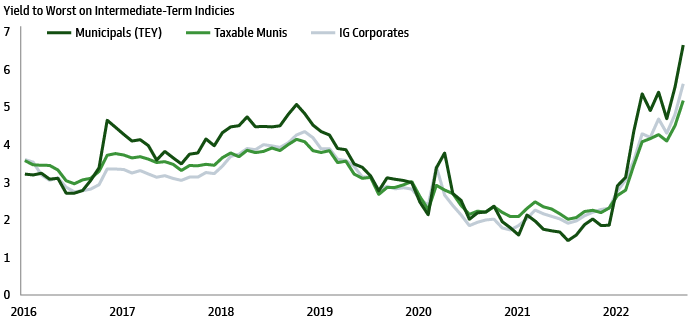

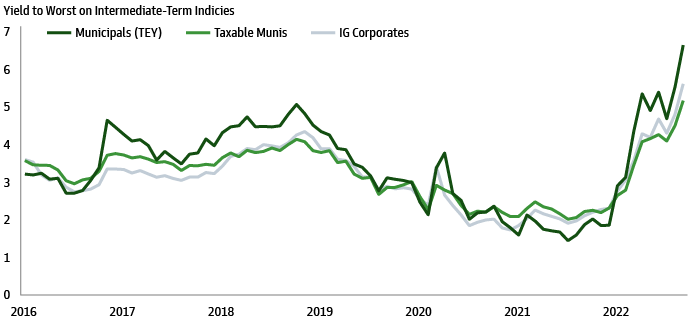

For investors who pay US taxes, municipal bonds also look more attractive than they have in some time. Yields on the Bloomberg Municipal Bond Index have moved from roughly 1 percent to 4%, while the tax-equivalent yield is above 6.8% (Exhibit 1).

We think that presents very attractive potential opportunities for active investors. And there’s additional value to be had by venturing out the curve to longer maturity bonds.

Source: Bloomberg Barclays, as of September 29th, 2022. Assumes top federal rate of 37% and Medicare Surcharge of 3.8%.

Six months ago, when muni yields were lower, it made more sense for many to invest in comparable corporate bonds, whose yields offered a better return on an after-tax basis. Today, the situation has reversed. This opens up new opportunities to customize portfolios for investors based on their individual tax rate. Investors may also want to consider opportunities in lower-rated municipal credit, which has benefitted from strong state revenues and low default rates.

Private alternative strategies can provide access to differentiated source of return, offering diversification that we believe may help portfolios weather today’s increasingly volatile markets.

Real estate, for instance, has historically provided a strong inflation hedge since rents typically rise when overall prices do. But real estate markets today are not monolithic and opportunities in residential, office space, and warehouses to support the logistics of ecommerce operations vary across regions and countries. This heightens the importance of experienced managers with the ability to analyze the operating performance potential of each asset and its ability to underwrite each asset to be sure it can service its debt.

Private markets may provide opportunities, too, as increased investment in recent years has left many limited partners over-allocated to the space. The potential result: we expect to see more secondary market sales of attractive assets that may offer entry into the market for investors who want to diversify. Private credit transactions offer floating rate income in a rising rate environment. But sourcing high quality deals is critical to success—and that requires access to a large pool of transactions and an asset manager appropriate scale.

Investors face a variety of challenges in today’s market conditions. But with those challenges come what we consider a compelling opportunity to add value and make the most of market volatility.

Committed to providing you with the insights you need to build your practice.

Risk Considerations

All investing is subject to risk, including the possible loss of the money you invest.

Equity securities are more volatile than bonds and subject to greater risks. Dividends are not guaranteed and a company’s future ability to pay dividends may be limited.

Investments in fixed income securities are subject to the risks associated with debt securities including credit and interest rate risk.

Investments in foreign securities entail special risks such as currency, political, economic, and market risks. These risks are heightened in emerging markets.

Investments in commodities may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity.

High-yield, lower-rated securities involve greater price volatility and present greater credit risks than higher-rated fixed income securities.

Private equity investments are speculative, highly illiquid, involve a high degree of risk, have high fees and expenses that could reduce returns, and subject to the possibility of partial or total loss of fund capital; they are, therefore, intended for experienced and sophisticated long-term investors who can accept such risks.

Alternative investing is not suitable for all investors and liquid alternatives are not riskless investments, so investors can lose money.

Alternative investments are suitable only for sophisticated investors for whom such investments do not constitute a complete investment program and who fully understand and are willing to assume the risks involved in. Alternative Investments. Alternative Investments by their nature, involve a substantial degree of risk, including the risk of total loss of an investor’s capital.

The value of securities issued by technology and technology-related companies may be adversely affected by intense market volatility, aggressive competition and pricing, consumer preferences, short product cycles, lack of commercial success for new products, product obsolescence or incompatibility, government regulation and excessive investor optimism or pessimism, among other factors.

Real estate investments are speculative and illiquid, involve a high degree of risk and have high fees and expenses that could reduce returns. These risks include, but are not limited to, fluctuations in the real estate markets, the financial conditions of tenants, changes in building, environmental, zoning and other laws, changes in real property tax rates or the assessed values of Partnership Investments, changes in interest rates and the availability or terms of debt financing, changes in operating costs, risks due to dependence on cash flow, environmental liabilities, uninsured casualties, unavailability of or increased cost of certain types of insurance coverage, fluctuations in energy prices, and other factors, such as an outbreak or escalation of major hostilities, declarations of war, terrorist actions or other substantial national or international calamities or emergencies. The possibility of partial or total loss of an investment vehicle’s capital exists, and prospective investors should not invest unless they can readily bear the consequences of such loss.

Further, some real estate investments may require development or redevelopment, which carries additional risks relating to the availability and timely receipt of zoning and other regulatory approvals, the cost and timely completion of construction, and the availability of permanent financing on favorable terms. Real estate investments will be highly illiquid and will not have market quotations. As a result, the valuation of real estate investments involves uncertainty and may be based on assumptions. Accordingly, there can be no assurance that the appraised value of a real estate investment will be accurate or further, that the appraised value would in fact be realized on the eventual disposition of such investment. In addition, real estate assets may be highly leveraged, which leverage could have significant adverse consequences to the assets and therefore an investment vehicle. In particular, an investment vehicle will lose its investment in a leveraged asset more quickly than a non-leveraged asset if the asset declines in value. You should understand fully the risks associated with the use of leverage before making an investment in a real estate investment vehicle.

Investments in real estate companies, including REITs or similar structures are subject to volatility and additional risk, including loss in value due to poor management, lowered credit ratings and other factors.

Hedge funds and other private investment funds (collectively, “Alternative Investments”) are subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains and an individual’s net returns may differ significantly from actual returns. Such fees may offset all or a significant portion of such Alternative Investment’s trading profits. Alternative Investments are not required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of such Alternative Investments.

Alternative Investments often engage in leverage and other investment practices that are extremely speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested. There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers.

Alternative Investments such as private equity funds are subject to less regulation than other types of pooled investment vehicles such as mutual funds, may make speculative investments, may be illiquid and can involve a significant use of leverage, making them substantially riskier than the other investments. An Alternative Investment Fund may incur high fees and expenses which would offset trading profits. Alternative Investment Funds are not required to provide periodic pricing or valuation information to investors. The Manager of an Alternative Investment Fund has total investment discretion over the investments of the Fund and the use of a single advisor applying generally similar trading programs could mean a lack of diversification, and consequentially, higher risk. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of the Fund.

Alternative Investments by their nature, involve a substantial degree of risk, including the risk of total loss of an investor’s capital. Fund performance can be volatile. There may be conflicts of interest between the Alternative Investment Fund and other service providers, including the investment manager and sponsor of the Alternative Investment. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers. Private Equity investments are speculative, involve a high degree of risk and have high fees and expenses that could reduce returns; they are, therefore, intended for long-term investors who can accept such risks. The ability of the underlying fund to achieve its targets depends upon a variety of factors, not the least of which are political, public market and economic conditions.

Alternative Investments are offered in reliance upon an exemption from registration under the Securities Act of 1933, as amended, for offers and sales of securities that do not involve a public offering. No public or other market is available or will develop. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers.

Alternative Investments may involve complex tax and legal structures and accordingly are only suitable for sophisticated investors. You are urged to consult with your own tax, accounting and legal advisers regarding any investment in any Alternative Investment.

Conflicts of Interest - There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. These activities and interests include potential multiple advisory, transactional and other interests in securities and instruments that may be purchased or sold by the Alternative Investment. These are considerations of which investors should be aware and additional information relating to these conflicts is set forth in the offering materials for the Alternative Investment.

Buy-write strategies are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. They are also subject to the risks associated with writing (selling) call options, which limits the opportunity to profit from an increase in the market value of stocks in exchange for up-front cash at the time of selling the call option. In a rising market, the strategy could significantly underperform the market, and the options strategies may not fully protect it against declines in the value of the market. A Buy Write Strategy's maximum loss is equal to the full value of shares minus the premium collected from the options.

The above are not an exhaustive list of potential risks. There may be additional risks that should be considered before any investment decision.

Definitions

Bloomberg Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market.

MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries around the world, excluding the US and Canada. With 799 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI EAFE Value Index captures large and mid-cap securities exhibiting overall value style characteristics across Developed Markets countries around the world, excluding the US and Canada. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield.

S&P 500 is an index that tracks the stock performance of approximately 500 large companies listed on stock exchanges in the US.

General Disclosures

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this publication and may be subject to change, they should not be construed as investment advice. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

The views and opinions expressed are as of September 21, 2022 and for informational purposes only and do not constitute any investment advice or recommendation by Goldman Sachs Asset Management, and may be subject to change. We have relied upon and assumed (without independent verification) the accuracy and completeness of such information and neither agree nor disagree with the content herein.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Goldman Sachs does not provide legal, tax or accounting advice, unless explicitly agreed between you and Goldman Sachs (generally through certain services offered only to clients of Private Wealth Management). Any statement contained in this presentation concerning U.S. tax matters is not intended or written to be used and cannot be used for the purpose of avoiding penalties imposed on the relevant taxpayer. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you may disclose to any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be aware that a determination of the tax consequences to them should take into account their specific circumstances and that the tax law is subject to change in the future or retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

Diversification does not protect an investor from market risk and does not ensure a profit.

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence (“S&P”) and is licensed for use by Goldman Sachs. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the portfolio will achieve similar results. The index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark.

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein.

Date of First Use: October 11, 2022. 293263-OTU-1679682