Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsINTRODUCTION TO PRIVATE EQUITY

August 1, 2022 | 6 Minute Read

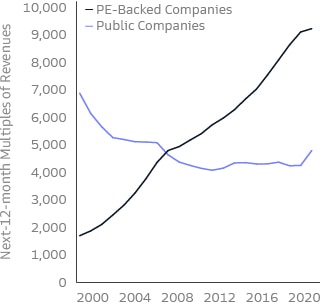

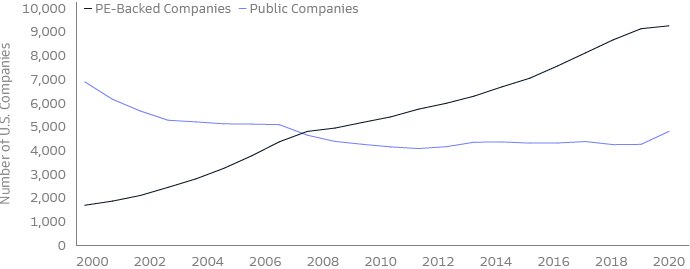

As an asset class, private equity has gained increasing attention among both companies looking to access capital and investors looking to diversify beyond traditional public markets. Over the last two decades, the number of companies backed with private capital has grown significantly, while the number of publicly listed firms has contracted (see below figure). This trend has been driven in part by increasing regulatory requirements of public companies and the accumulation of investor capital looking for alternative sources of return. Given the increased complexity and higher thresholds governing investor access to private equity (including potential illiquidity and higher investment minimums), it’s important to understand the nuances of investing in this growing asset class.

The Universe of PE-Backed Companies Has Grown While The Universe of Public Companies Has Shrunk

Source: PitchBook as of 6/30/2021. Public companies over time: World Bank, McKinsey.

What is Private Equity?

Private equity refers to investments in the equity of companies not listed on a public stock exchange. Most investors access these opportunities through private equity funds— pooled investment vehicles where a private equity manager, or General Partner (GP), identifies, evaluates, acquires, and manages investments on behalf of a group of investors, or Limited Partners (LPs).* The fund manager draws down the capital committed to the fund to invest in companies as opportunities arise, typically over multiple years.

The ultimate goal of a private equity fund is to increase the value of its stakes in companies and to realize a profit upon exiting each investment, through an initial public offering, sale, or other liquidity event. As exits occur, the realized proceeds are returned to investors until the final investment is sold and the fund is liquidated.

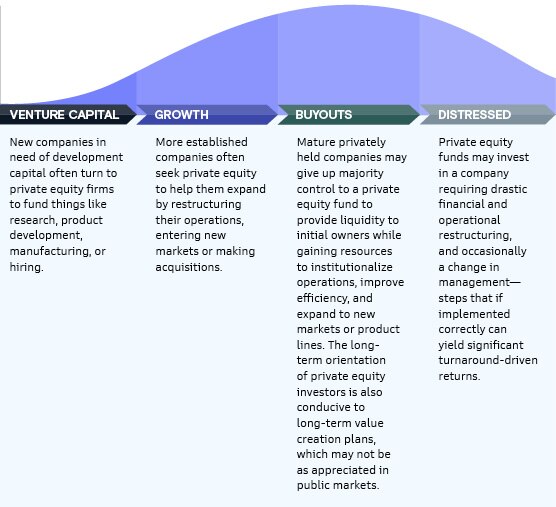

Private Equity Funds Tend to Focus on One of Four Main Investment Strategies That Span the Maturity Spectrum:

Why Invest in Private Equity?

Private equity can add value to investor’s portfolios in two main ways.

First, by giving access to investment opportunities that are simply not available in public markets. As companies stay private for longer, much of the value that was previously generated in public markets is now being built under private ownership.

Second, by private equity managers working hand-in-hand with their portfolio companies, boosting growth trajectories and operating efficiency. Since private fund managers have more concentrated ownership, it is easier for them to influence the companies they own. Experienced managers have extensive expertise in everything from growing and scaling businesses, to improving strategy and operations, to integrating technology for growth and efficiency. Such expertise is more important than ever in today’s environment of accelerated growth and emphasis on resiliency, agility and innovation.

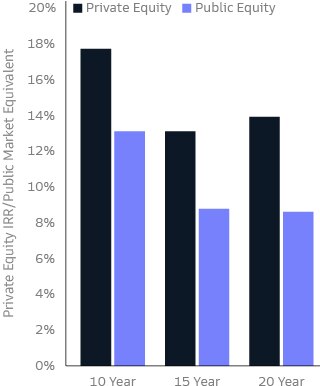

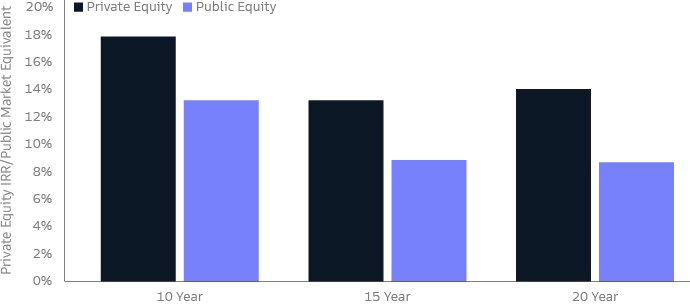

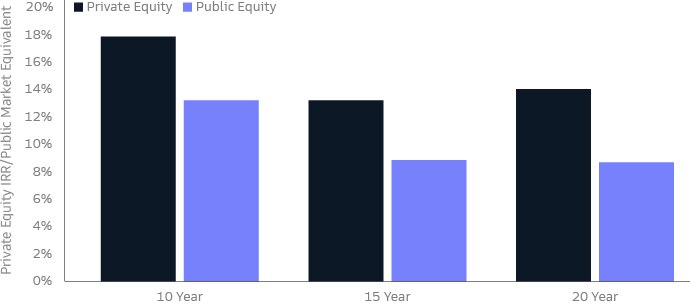

Aided by these sources of value creation, private equity can offer differentiated, attractive returns—complementing traditional investment portfolios. Historically, private equity has achieved returns that have significantly exceeded those of public equity markets, over various time horizons (below figure).

Private Equity Has Outperformed Over Various Time Horizons

Source: Cambridge Associates, data as of December 2021. Private equity returns shown net of fees. Past performance does not guarantee future results, which may vary. Public equity data shown via a public market equivalent (PME) methodology, which reflect the performance of a public market index (MSCI World Index) expressed in terms of an internal rate of return and takes into account the timings of a private equity fund’s cash flows. PME returns do not represent the actual performance of the index. Indices are unmanaged and investors cannot invest in indices. The index returns used to calculate PME returns are gross total return, with dividends reinvested and do not reflect the deduction of any fees or expenses, which would reduce returns.

Evolution of the Asset Class

The first expression of private equity was in the form of venture capital firms formed in the 1940s as a way to finance innovative new ideas. Since then, private equity has played an important role in financing innovation and supporting the growth of the global economy.

Venture capital firms funded groundbreaking technologies that laid the foundation for the explosive growth of personal computing and the internet, continually evolving their strategy to meet the changing needs of startup companies. Today, venture capital strategies have proliferated to target specific sectors and stages of company development.

The buyout strategy has grown and evolved significantly since it first came to prominence in the 1980s. In its early stages, a meaningful component of its returns came from using a large amount of debt to finance the purchase of portfolio companies— an approach that amplified returns on the equity investment. As a result, buyout managers tended to seek companies with stable cash flows, typically in steadier but slower-growth sectors such as industrials and consumer staples. With much of the cash flow used for repaying the debt, less funding was available to reinvest in the company’s growth—which moderated portfolio companies’ growth prospects.

Today, buyout strategies take a different approach, focusing on growing and creating value within their portfolio companies. They have become active owners, working closely alongside their portfolio companies’ management teams. Some of the largest private equity managers have teams dedicated exclusively to value creation initiatives, with members specializing in discrete aspects of driving company value, such as customer acquisition, supply chain optimization, and talent management. A recent academic study has found that these activities have been the largest driver of value creation of private equity funds over the past 15 years.

With an increased focus on growth, resiliency, agility, and innovation, the mix of companies being acquired by buyout managers has shifted as well. Increasingly, focus has shifted towards companies powering the economy of the future, including companies developing software and other technologies. The typical buyout today features a lower portion of debt than three decades ago. However, buyout portfolio companies still have higher debt levels than their public counterparts, so cash flow generation continues to be important. As such, emphasis continues to be on companies with resilient business models and steady, predictable cash flows—and with the evolution of the technology industry towards such business models, buyout managers have been capitalizing on a growing opportunity set.

Finding the Right Partner

While aggregate performance is strong, dispersion of returns across individual investments, and, indeed, across different managers in private equity can be substantial. This makes finding the right partner critical. Manager skill is not evenly distributed, as evidenced by the high degree of performance dispersion among private equity funds, magnifying the importance of manager selection. Firms with deep experience through market cycles and extended global reach are better positioned to effectively deploy investor capital in value-creating investments.

Save A Copy of this PDF

Introduction to Private Equity

Related Insights

-

-

August 12, 2022 | GSAM Featured Insights

August 12, 2022 | GSAM Featured InsightsIncome Generating Alternatives

August 12, 2022 Over the past decade, private credit and private real estate have emerged as attractive income-generating alternatives for investors searching for yield in a low rate environment. While interest rates have started rising, these asset classes can continue to be attractive alternatives due to risk-adjusted return potential and ability to access parts of the market that are not available in publicly-traded instruments. Read More

×

Start the Conversation

Committed to providing you with the insights you need to build your practice.