August 4, 2022 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsSeptember 2, 2022 | 9 Minute Read

Amit SinhaCIO of Goldman Sachs Life Sciences Amit Sinha |

Josh Richardson, M.D.Life Sciences Investing Josh Richardson, M.D. |

Kevin XuLife Sciences Investing Kevin Xu |

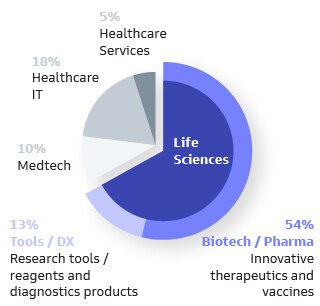

Healthcare is an integral part of the global economy that impacts every individual. The largest segment of the healthcare sector is Life Sciences (LS), which applies the study of living organisms and life processes towards the development of novel medicines and related technologies. The COVID-19 pandemic highlighted the importance and impact of the innovation and structural changes that are driving LS growth globally. We believe the current landscape provides opportunities to drive research forward in critical LS areas and explore new avenues for streamlining drug development and approval processes.

Source: PitchBook. As of December 31, 2021. Statista. As of February 28, 2021. Grand View Research. As of March 1, 2022.

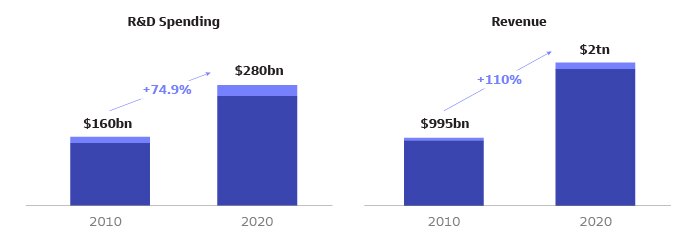

In our view, the foundation for LS innovation is supported by several key drivers, underpinned by decades of strong investment from both the private and public sectors. Tailwinds from sustained growth in funding and research are leading to a proliferation of scientific publications and new patents, with breakthroughs across disciplines including genetics, immunology, and cell biology. In parallel, technological advancements, such as the use of artificial intelligence (AI), are leading to faster drug development timelines and the creation of more personalized therapeutics. Advancements in the understanding of disease and a convergence of innovation across many scientific disciplines are enabling the development of new drug platforms that create novel ways to treat disease and solve patients’ unmet needs. Separately, regulatory bodies are creating policies to better leverage new technology and create new approval pathways, with a concerted effort in many geographies to support domestic LS innovation and development.

As the drug development process is evolving so are company formation timelines, creating a need for new financing models and capital solutions. In the next decade, 15 of the top-selling drugs in 2020 will lose patent exclusivity, resulting in a loss of $100bn+ in sales for large pharma companies.1As such, large pharma is reevaluating its long-standing strategy of developing most drugs in-house, and increasingly looking to smaller biotech companies as a way to acquire innovative drugs to replenish pipelines. However, small biotechs often have limited access to financing to efficiently progress through clinical trials while remaining private and independent. Going forward, we believe the next decade will see an acceleration of some of the critical trends that have shaped pharma strategies and pipelines historically. This will create challenges for incumbents, but opportunities for innovative new companies and technologies to come to the forefront.

Source: Goldman Sachs Asset Management. For illustrative purposes only.

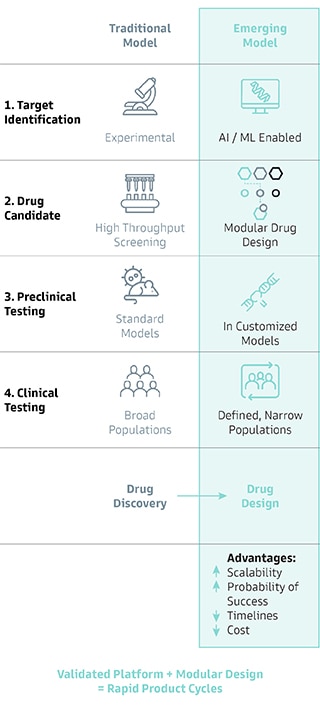

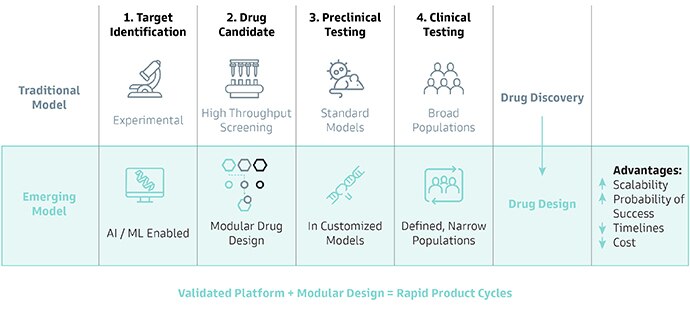

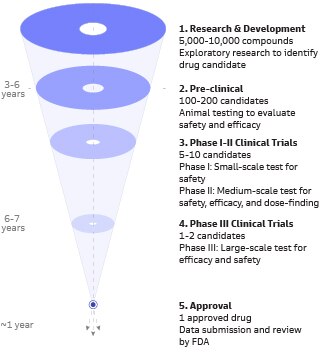

Drug development is the most resource- and time-intensive segment of LS, historically requiring about 9 years (Investigational New Drug to approval) and $1-2bn to advance a single drug to approval.2 These long development timelines are the result of a traditionally rigid regulatory structure that was developed to ensure the safety and efficacy of products for human use. The drug development process continues to benefit from advancements in tools, diagnostics, technology, and regulation. As a result, we expect timelines to compress and the process to become more cost-efficient in the coming years.

Source: Goldman Sachs Asset Management. For illustrative purposes only.

New applications of AI and machine learning (ML), adaptation of modular drug design, and improvements in clinical trial design and operations are creating a paradigm shift from a traditional model of drug discovery to an emerging model of rational drug design. This more engineering-based approach to drug development is enabling faster scalability, increased probability of success, accelerated timelines, and reduced cost.

Improved computing power and advancements in AI/ML techniques have made it possible to glean insights from an exponentially growing set of healthcare data. As techniques become more sophisticated, AI/ML has the potential to increase efficiency and reduce costs at many stages of drug development. One recent application is protein structure prediction, which is expected to have groundbreaking implications for science and medicine given the pivotal role that protein structure has for enabling drug discovery efforts and the arduous experimental approaches that are often needed to obtain protein structure.3 Many other examples of the value of AI/ML in drug discovery continue to emerge, with novel insights being derived for faster target identification and prioritization, more accurate identification of disease-relevant phenotypes, streamlined compound design and optimization, and precise predictions from high content imaging and digital pathology.

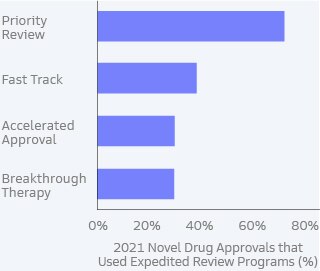

Companies engage a broad system of stakeholders that changes over the course of development—ranging from academic and research organizations in early development, to regulatory bodies and payers (i.e., insurers) that play a critical role in the approval and commercialization of drugs. To that end, advancements in the drug development process are complemented by an evolving regulatory environment, which is enabling greater flexibility. Recent regulatory modifications have more clearly defined situations where the clinical development process can be modified to better meet patient needs, ethical considerations, or specific requirements of the disease or drug modality. In the U.S., which produces the most biotech patents worldwide, the FDA has introduced new policies that are providing support for access to innovation and novel therapies.4 The result has been that annual FDA approvals doubled in the decade from 2010 to 2020.5 Similar initiatives are being undertaken by regulators in other regions, including the EMA (Europe) and NHMP (China).

Example: Oncology products approved using the accelerated approval pathway are brought to market 4.7 years faster than traditionally approved oncology therapies.4

Designation for drugs that show significant improvements in safety or efficacy; directs FDA resources to shorten decision timeline to 6 months

Process designed to facilitate development, expedite review of drugs to treat conditions with an unmet medical need, to get drugs to patients faster

For drugs that require an extended period to measure intended effects, approval can be granted based on surrogate endpoints in some cases

Ability to gain approval based on preliminary clinical evidence if data indicates drug may provide substantial improvement over available therapy

Source: US Food and Drug Administration. As of December 31, 2021.

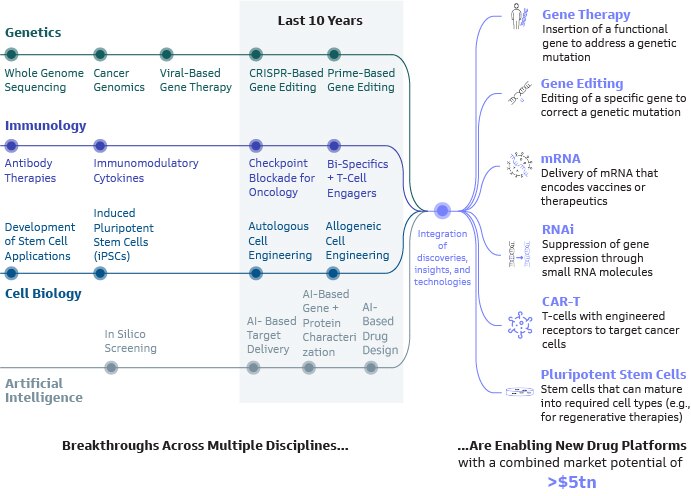

Drug development is becoming increasingly interdisciplinary, with breakthroughs across key disciplines such as genetics, immunology, cell biology, and AI converging to create new modalities and drug platforms. Over the last ten years, the emergence of CRISPR-based gene editing has created an ability to precisely edit and manipulate genes, to correct genetic mutations, potentially treating genetic diseases at the source. A greater understanding of immunology has enabled more targeted therapies that use a patient’s own immune system to fight disease. Immune checkpoint inhibitors (i.e., drugs that block signals used by cancer cells to evade the immune system, allowing the body to recognize and kill cancer cells) are now widely used to treat a range of cancers. Engineered immunotherapies created with bi-specific antibodies and T-cell engagers (i.e., modalities that direct the immune system to target and kill cancer cells) are creating more targeted cancer therapies that greatly increase the standard of care over traditional chemotherapy and radiation approaches. Advancements in cell biology offer a complex, context-dependent ability to treat disease, with potential applications in regenerative medicine. The rapid growth in AI capabilities provide a powerful tool, not only for improved computational screening, but also for the identification of novel targets and design of new drugs. Collectively, the integration of discoveries, insights, and technologies across disciplines yields a more targeted, innovative, and effective way to treat disease through new drug platforms.

Source: Goldman Sachs Asset Management. FDA (FDA Policies, Use of Policies).For illustrative purposes only.

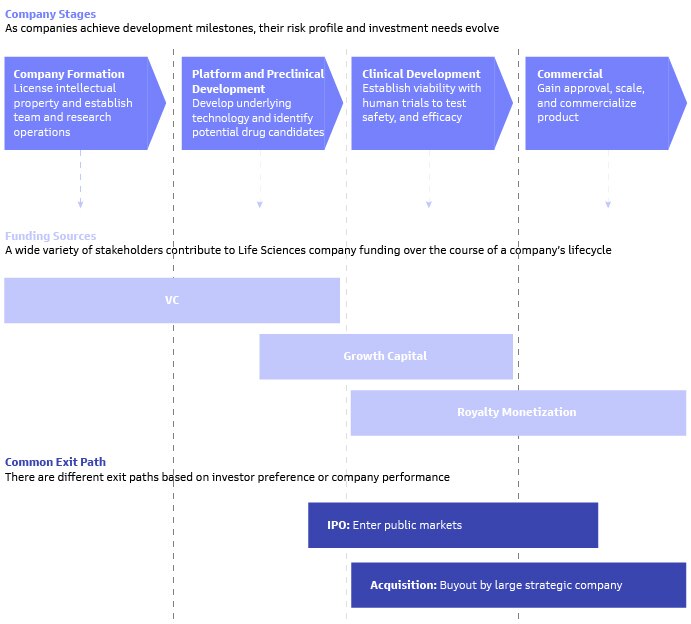

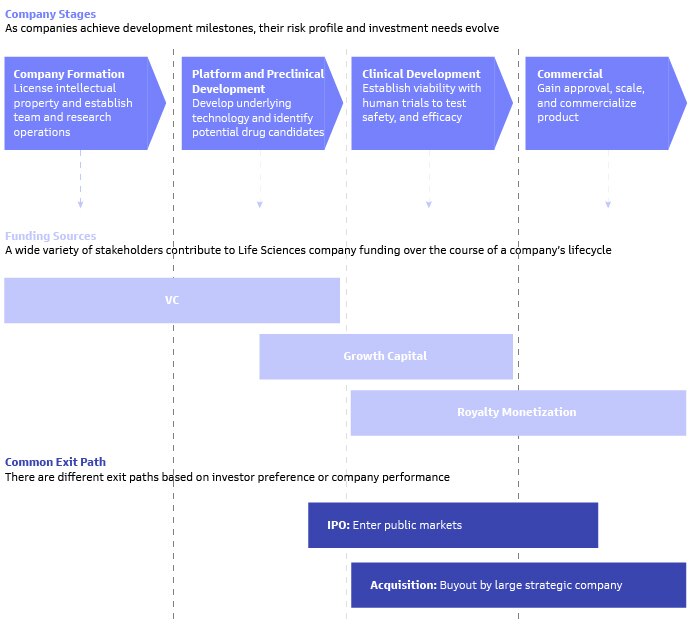

Scientific breakthroughs and improved regulatory frameworks are leading to structural changes that are shifting how LS innovation takes place. The evolution of life sciences startups can often mirror the drug development process, with companies experiencing different risks, opportunities, and financing needs as they reach new milestones and phases of development. As drug development processes evolve, the timeline of company formation and maturation is shifting too.

Smaller biotechs are often more specialized, agile, and closer to key sources of innovation (e.g., universities) than large pharma, making them better suited to advance novel therapies from concept to clinical trials. The cost of launching an LS startup and developing new IP has fallen as technology and processes have improved—similar to how cloud computing, no-code programs, and SaaS products have reduced the cost to launch a tech startup. While it is now cheaper to launch a new company and establish an initial proof of concept, it is more capital-intensive than ever to navigate clinical trial design and operations, as well as the ever-changing regulatory approval process.

Traditional financing models for LS have not yet adapted to the changing landscape. Not only have the number of LS startups increased, but the shift to more platform-based companies has resulted in increased capital requirements beyond the capacity of traditional sources. LS companies in the early research stage rely heavily on government or philanthropic capital that is generally not seeking a financial return (e.g., grants) to help establish a viable idea. The falling costs of launching a startup enable this initial funding to take a company further than before. Early-stage LS venture firms have been integral in supporting company formation around early ideas, with annual investment more than tripling to $18bn in the decade through 2020.6 Traditionally, LS venture firms funded companies for long periods through initial clinical trials when scientific and clinical risk remained high. However, while upfront costs have gone down, longer term capital requirements have intensified. Simultaneously, VC financing has been insufficient to meet the needs of LS startups. As a result, we believe that private growth capital provides a unique solution to companies that have a different growth curve.

Source: Goldman Sachs Asset Management. For illustrative purposes only.

Drug development at small companies is often facilitated through partnerships with large pharma companies, whose operational capabilities are more conducive to clinical trials, drug manufacturing, and distribution rather than drug development. The more recent focus of developing platform technologies with non-binary outcomes, as opposed to single assets, also means that biotech companies can produce diversified product lines while scaling more quickly than in the past. Large pharma companies, who are increasingly facing loss of exclusivity on top-selling drugs, look to these products developed by smaller companies to replenish existing and future drug pipelines.

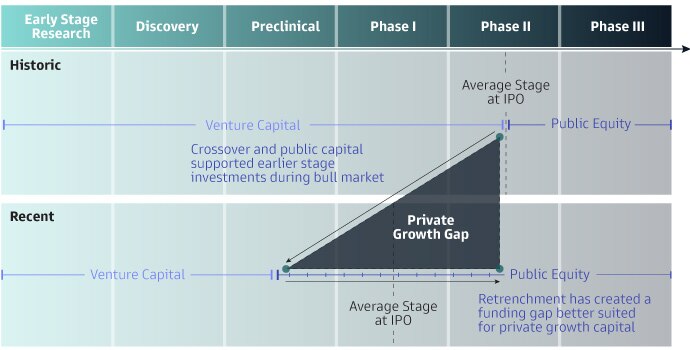

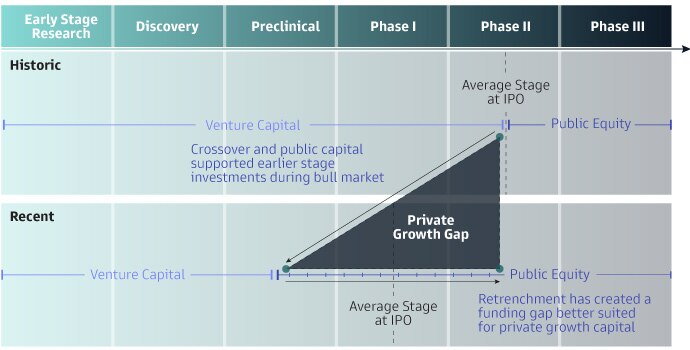

For companies that choose to remain independent, the increased capital needs of clinical development have led them to go public earlier in their development. Between 2014 and 2021, the percentage of biotech companies going public in pre-clinical or phase 1 stage surged from 12% to 59%.7 While biotech/pharma companies account for less than 10% of VC deals annually, the industry has consistently accounted for at least 25% of VC-backed IPOs, reflecting the need for companies to tap public markets.8

Many LS companies today still have high levels of scientific, clinical and regulatory risk at the time of IPO, often with binary options for success. This risk can be difficult to price in public markets, with many investors preferring opportunities at the late-clinical or commercial phase when scientific and regulatory risk has largely been minimized. To that end, the median returns 12-months post IPO declined from 59% in 2014 to -11% in 2020/21. Additionally, the daily volatility of public markets can lead LS companies to trade with broad market conditions, rather than based on the development of the underlying technology. These issues are particularly pertinent when additional financing is needed to support further clinical development, as is often the case for many early-stage companies entering public markets today. As a result, public markets are often a sub-optimal financing option for financing throughout clinical trials.

Traditional VCs continue to support robust idea and company formation; however, these companies require substantial capital beyond this stage to fund definitive experiments to de-risk and scale the platform and develop associated therapeutics. With the increasing number of companies being formed and decreasing ability to access public equity capital, we expect this to result in an opportunity set of high quality private companies that require private capital to scale.

Source: Goldman Sachs Asset Management. For illustrative purposes only.

As macro-trends drive demand for better healthcare, we believe that innovations in tools, technologies, and processes for treating disease, combined with a supportive regulatory environment, has created a golden age for LS that will enable faster, better innovation globally. While significant advancements have been made in recent years, we believe we are still in the early stages of a multi-decade era of unprecedented growth. As funding for research, a growing workforce, and better global drug development infrastructure continues to enable greater supply of novel ideas, new financing models will be needed to support company formation and development. This is presenting an opportunity for private market investors with the requisite expertise and network to capitalize on a timely opportunity to advance the future of healthcare innovation through investment in LS.

Committed to providing you with the insights you need to build your practice.

1 “The Top 15 Blockbuster Patent Expirations Coming This Decade.” Higgins-Dunn, Noah. Fierce Pharma, July 12, 2021.

2 “Research and Development in the Pharmaceutical Industry.” Congressional Budget Office, April 2021.

3 Callaway, “It will change everything”. AI makes gigantic leap in solving protein structures, Nature, 588, December 2020..

4 "Understanding the History and Use of the Accelerated Approval Pathway," Avalere. January 4, 2022.

5 U.S. Food and Drug Administration.

6 PitchBook. As of March 30, 2022.

7Goldman Sachs.

8 Pitchbook.

General Disclosures

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

This material represents the views of Goldman Sachs Asset Management. It is not financial research or a product of Goldman Sachs Global Investment Research (GIR). It was not a product nor financial research of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed herein may vary significantly from those expressed by GIR or any other groups at Goldman Sachs. Investors are urged to consult with their financial advisers before buying or selling any securities. The information contained herein should not be relied upon in making an investment decision or be construed as investment advice. Goldman Sachs Asset Management has no obligation to provide any updates or changes.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes.

These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. It should not be assumed that investment decisions made in the future will be profitable or will equal the performance of the securities discussed in this document.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness.

We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

Supplemental Risk Disclosure for All Potential Direct and Indirect Investors in Hedge Funds and other private investment funds (collectively, “Alternative Investments")

In connection with your consideration of an investment in any Alternative Investment, you should be aware of the following risks:

Alternative Investments are subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains, and such fees may offset all or a significant portion of such Alternative Investment’s trading profits. An individual’s net returns may differ significantly from actual returns. Alternative Investments are not required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of the Alternative Investment.

Alternative Investments often engage in leverage and other investment practices that are extremely speculative and involve a high degree of risk.

Such practices may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested.

Alternative Investments may purchase instruments that are traded on exchanges located outside the United States that are “principal markets”

and are subject to the risk that the counterparty will not perform with respect to contracts.

Alternative Investments are offered in reliance upon an exemption from registration under the Securities Act of 1933, as amended, for offers and sales of securities that do not involve a public offering. No public or other market is available or will develop. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers.

Alternative Investments may themselves invest in instruments that may be highly illiquid and extremely difficult to value. This also may limit your ability to redeem or transfer your investment or delay receipt of redemption or transfer proceeds.

Alternative Investments are not required to provide their investors with periodic pricing or valuation information.

Alternative Investments may involve complex tax and legal structures and accordingly are only suitable for sophisticated investors. You are urged to consult with your own tax, accounting and legal advisers regarding any investment in any Alternative Investment.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from

Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), Goldman Sachs Asset Management, LP (GSAMLP) or Goldman Sachs & Co. LLC (GSCo). Both GSCo and GSAMLP are regulated by the US Securities and Exchange Commission under US laws, which differ from Australian laws. Both GSI and GSAMI are regulated by the Financial Conduct Authority and GSI is authorized by the Prudential Regulation Authority under UK laws, which differ from Australian laws. GSI, GSAMI, GSCo, and GSAMLP are all exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences. Any financial services given to any person by GSI, GSAMI, GSCo or GSAMLP by distributing this document in Australia are provided to such persons pursuant to ASIC Class Orders 03/1099 and 03/1100. No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

Malaysia: This material is issued in or from Malaysia by Goldman Sachs (Malaysia) Sdn Bhd (880767W)

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited.

Singapore: This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser.

The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en

Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Confidentiality

No part of this material may, without Goldman Sachs Asset Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

Date of First Use: September 2, 2022. 282953-OTU-1634164