Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsWOMEN & RETIREMENT SECURITY: DIGESTING THE DATA

Navigating the Financial Vortex

December 7, 2022 | 7 Minute Read

This year’s Retirement Survey & Insights Report, Navigating the Financial Vortex: From Retirement Readiness to Retirement Income, highlighted the challenges that working and retired individuals face as they save and invest for their retirement, especially in today's environment. The report shared detailed insights on prominent retirement trends experienced by generation and outlined potential difficulties these age groups may face on their retirement journey.

In this supplemental report, we take a deeper look at the gender differences from both working and retired Americans to better understand the challenges women face on their retirement journey.

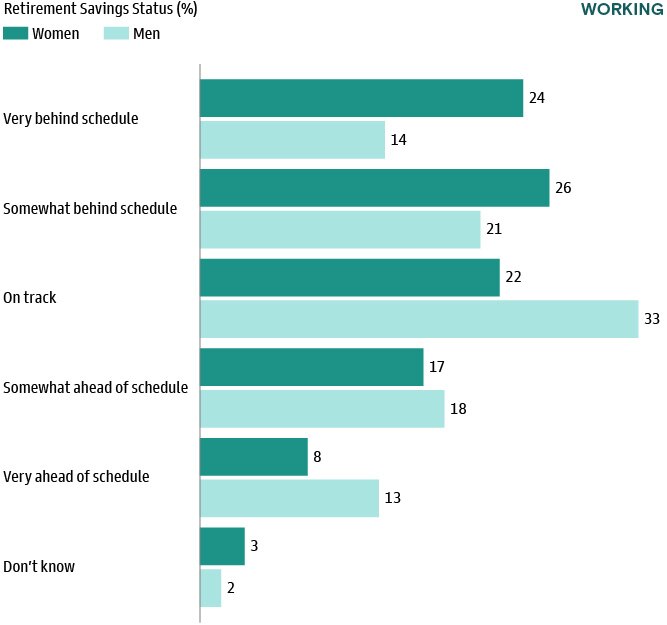

Half of Working Women Believe Their Savings are Behind Schedule

More women reported that their retirement savings are behind schedule relative to men. While more retired women are living on limited income, this data illustrates that some working women may be on a similar trajectory. Half of working women reported being behind schedule vs. 35% of men and almost a quarter of working women reported feeling they are very behind schedule.

In aggregate, 47% of working women reported feeling they are on track or ahead of schedule (vs. 64% of men).

Where would you say your retirement savings are at this moment?

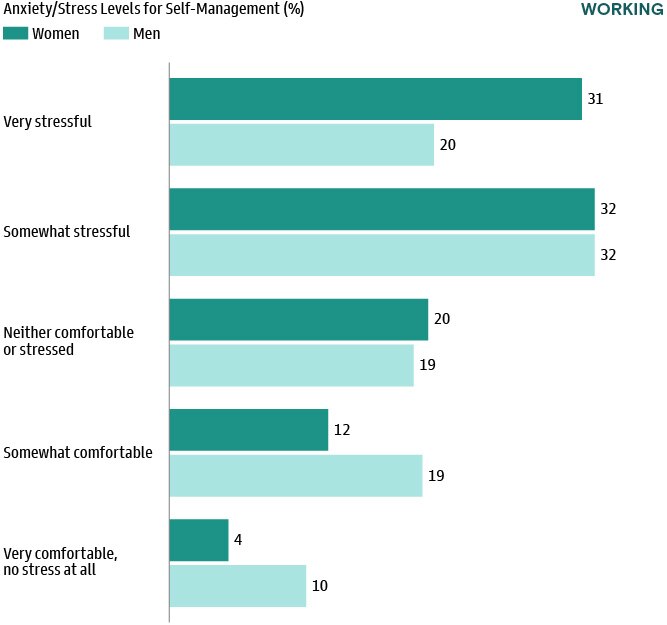

Financial Stress From Managing Retirement Savings

Some women expressed less comfort managing their retirement savings. The majority of women (63%) reported stress or anxiety managing their retirement savings, while 52% of men reported experiencing a similar level of concern. Notably, 31% of women reported that managing their own retirement savings is very stressful.

How much financial anxiety/stress do you feel managing your retirement savings?

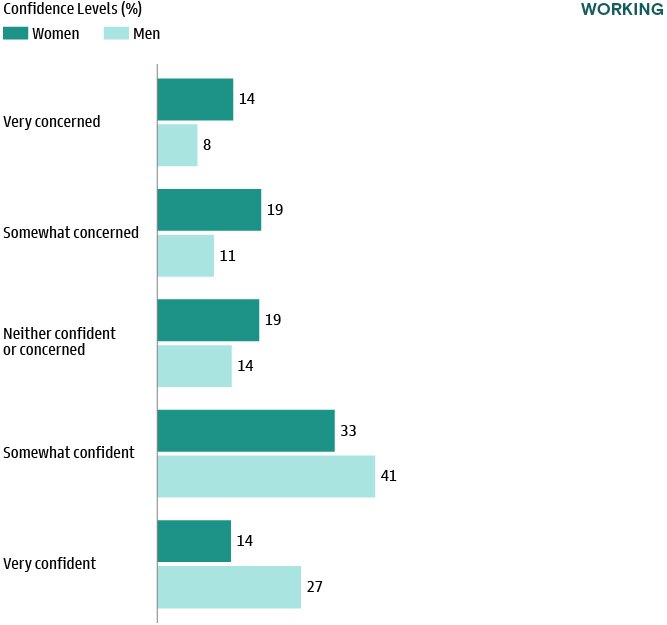

Lower Confidence in Meeting Retirement Saving Goals

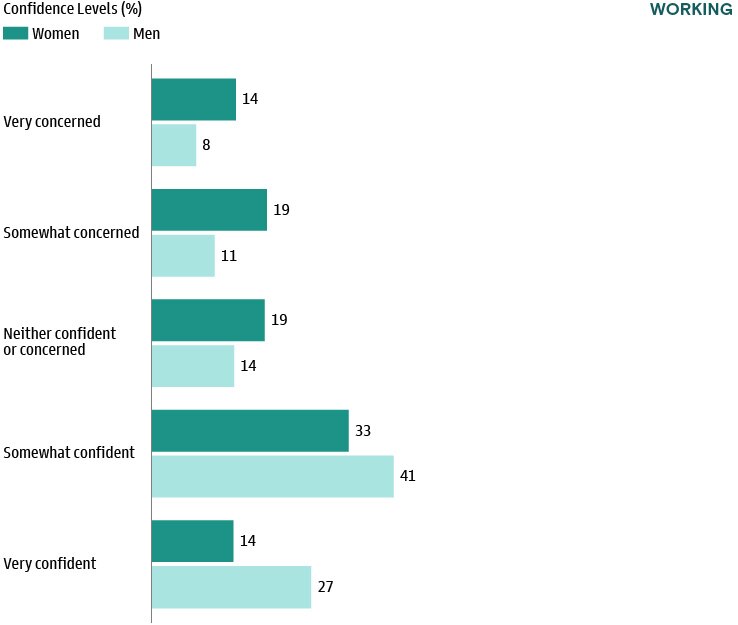

Women respondents (47%) were less confident than men (68%) in meeting retirement savings goals. Additionally, 33% of women reported concern that they will be able to meet their retirement goals, while 19% of men reported similar concerns. Of course, one’s confidence in their ability to reach their retirement goal is not the same as their actual ability. Empowering and building confidence is an important part of retirement planning support.

How confident are you that you will be able to meet your retirement goals/needs?

The Financial Vortex Has Greater Impact on Women's Ability To Save For Retirement

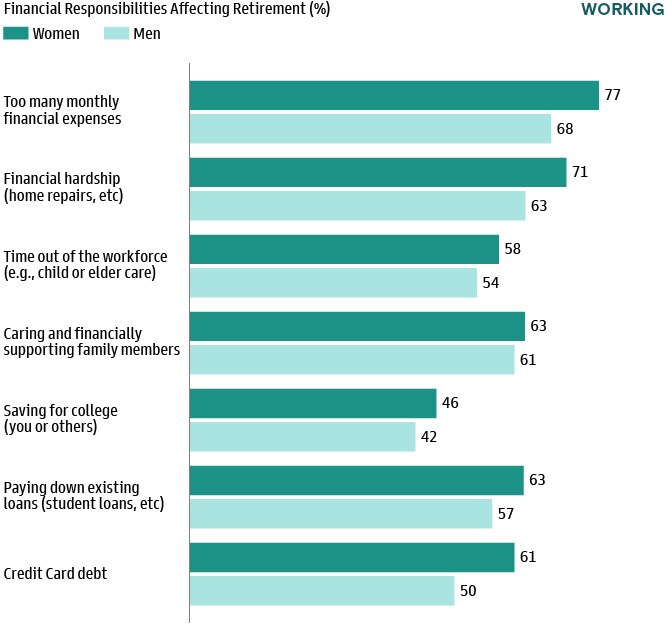

In the Retirement Survey & Insights Report 2022, we examined how the financial vortex affected workers at a generational level. Generation X, Millennials and Generation Z were increasingly affected by financial responsibilities in their ability to save for retirement, in part due to the transition from defined benefit plans to defined contribution plans.

From a gender perspective, women reported that financial responsibilities have a greater impact on their ability to save for retirement than men across all factors. This chart illustrates the need to successfully navigate competing short-term needs and the long-term need to reach retirement with sufficient savings.

How strongly do the below affect your ability to save for retirement? (Select from extremely, very, moderately, slight and did not affect).

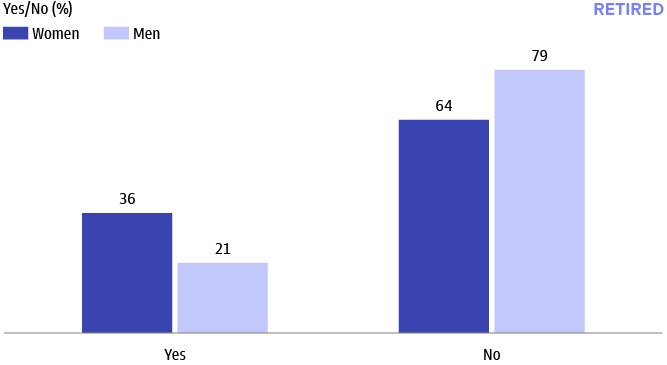

Women are More Likely to Take Time Away from the Workforce for Caregiving

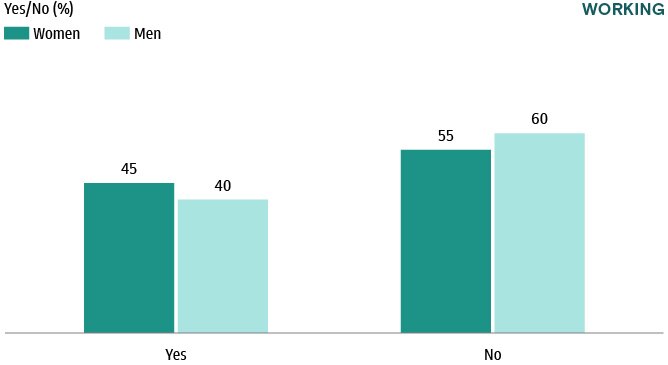

Women are often the primary childcare or elder care provider for their family. Caregiving can have a meaningful impact on retirement savings because an individual may often need time out of the workforce. Not working can have multiple long-term impacts: no current income, no earned income from a Social Security perspective (which lowers your overall Social Security benefit), and more limited ability to save. In addition, there may be immediate financial responsibilities to support the family member.

According to our study, 45% of working women (compared to 40% of working men) reported taking time away from the workforce to provide care. Both are significantly higher than retired respondents, where 36% of women and 21% of men reported taking time out of the workforce for caregiving.

Have you ever needed to take time away from the workforce to provide care for a family member?

Have you ever needed to take time away from the workforce to provide care for a family member?

Women Are More Likely to Take Time Away from the Workforce for Caregiving

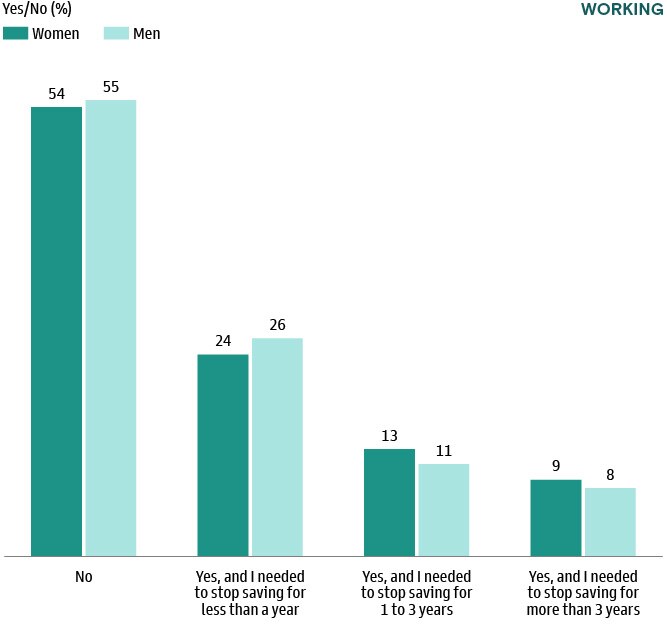

For both men and women respondents, we see that almost half reported having a financial hardship in their career that caused them to stop saving for retirement. Of those women who experienced a financial hardship and needed to stop saving for retirement, 22% reported needing to stop saving for one year or more.

Have you experienced a financial hardship that caused you to stop saving directly for retirement (e.g., in your 401(k))?

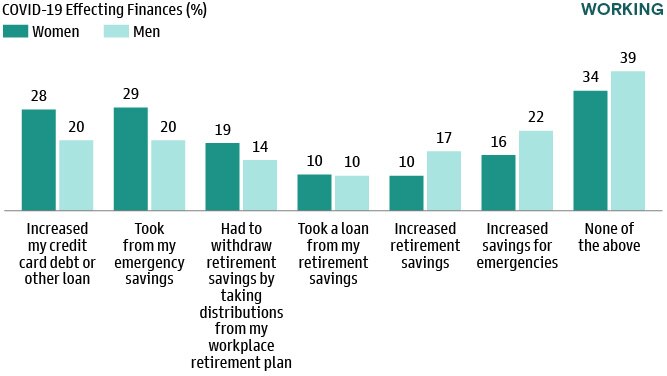

The Effect of the COVID-19 Pandemic on Retirement Savings

We reported on how the COVID-19 pandemic has affected working individuals in our Retirement Survey & Insights Report 2022.

Women were more likely to report being negatively impacted by the pandemic, with 29% being forced to withdraw funds from their emergency savings. On the other hand, only 20% of men reported withdrawing from their emergency fund during the pandemic. Additionally, 19% of women respondents withdrew from their retirement savings during the pandemic compared to only 14% of men.

Women respondents were also less likely to increase their retirement savings and emergency savings during the pandemic.

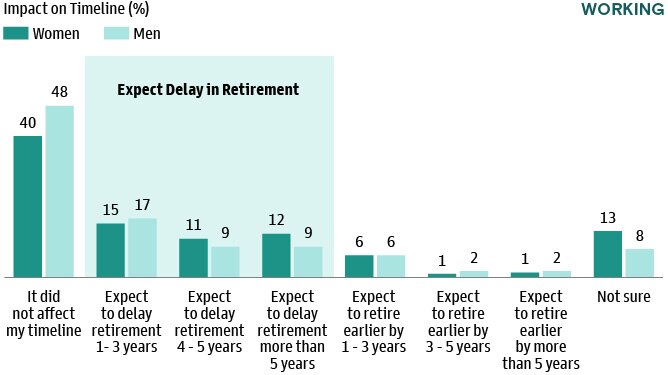

Supporting family needs (home schooling and childcare) and in some cases, the cost of childcare, cause some women to exit the workforce. While both men (35%) and women (38%) report expecting to delay their retirement due to the pandemic, women are more likely to report longer delays (23% women, more than four years vs. 18% of men).

Did any of the following happen to you during the Covid-19 pandemic?

How, if at all, did COVID-19 affect your expected retirement timeline?

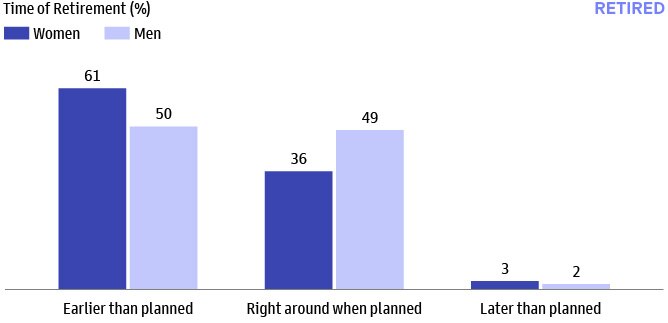

Women Are More Likely to Retire Early and for Reasons Outside Their Control

Retiring earlier than planned is an important reality many face in retirement. For women respondents, 61% retired earlier than planned vs. 50% of men, which means that only about two in five women respondents retired when they planned.

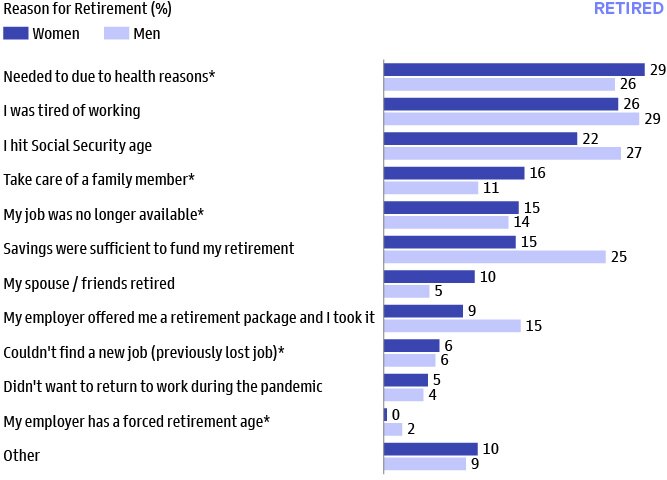

Additionally, there are notable differences in the reported reasons men and women retired. Health reasons was the top factor for women (29%) and tired of working was the top factor for men (29%). However, men were also more likely to report reaching Social Security age and that their savings were sufficient to fund retirement than women. Women were more likely to report taking care of a family member and retiring because a spouse or friend retired.

Overall, 66% of women retired for reasons outside of their control.

Did you retire earlier, right around, or later than planned?

Which of the following are reasons that you retired? (*Reasons considered outside the individual’s control)

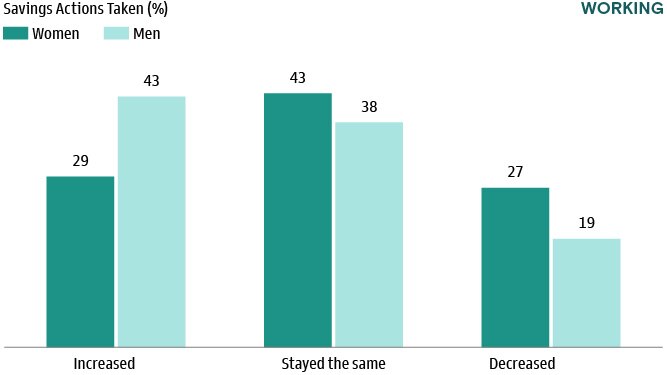

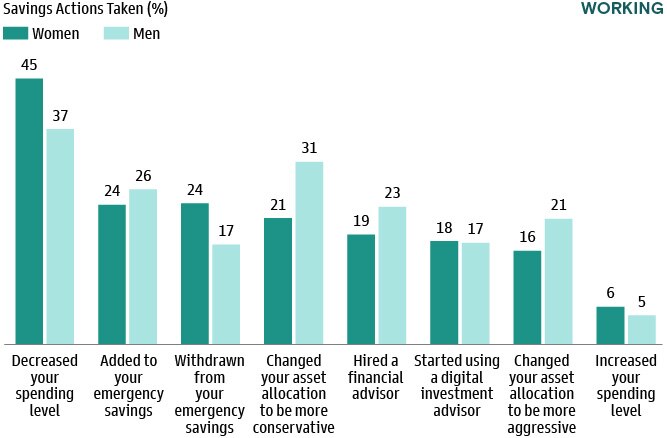

Market Volatility Leads to Lower Spending and Lower Savings

Market volatility can be difficult to navigate and can shake confidence in one’s saving strategy.

Women were more likely (27% vs. 19% for men) to report a decrease in their retirement savings relative to last year. Conversely, men were more likely to report an increase in savings relative to last year (43% vs. 29% for women). Broadly speaking, decreasing spending was reported as the top action being taken during the current market volatility. Additionally, 45% of women and 37% of men report decreasing spending.

Secondarily, 24% of women reported withdrawing from emergency savings (vs. 17% of men) and 31% of men reported moving to a more conservative asset allocation (vs. 21% of women).

Compared to the last year, has your annual retirement savings...

During this recent market volatility, what actions did you take?

Eight of Ten Retired Women May Not Have Enough Savings for Retirement

It is commonly suggested that 70% pre-retirement income is needed to maintain one’s standard of living in retirement. However, 80% of retired women respondents receive less than the 70% target (compared with 70% for men). Even more notable, 58% of women respondents generate less than 50% of their pre-retirement income in retirement (vs. 44% of men) and only 20% generate more than 70% (vs. 30% of men).

Plan sponsors may be able to support their plan participants by providing resources that offer personalized insight into their savings trajectory with recommendations on how to adjustment the strategy to help keep overall savings on track.

How much total annual income do you receive in retirement (including Social Security) relative to your pre-retirement income? (e.g., your final annual compensation prior to retirement, such as salary, bonus, etc.)

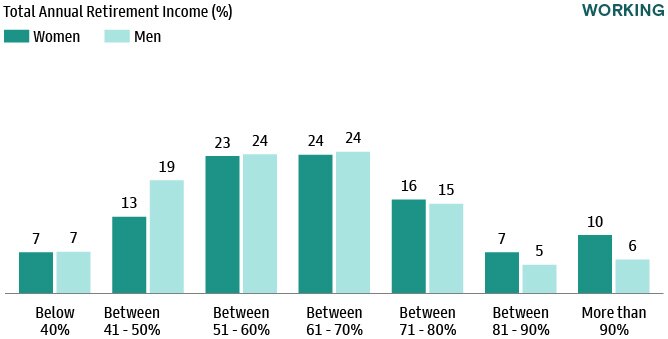

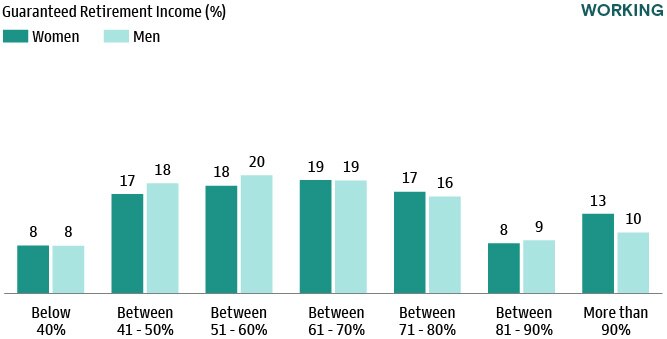

Many Women (and Men) Underestimate Their Retirement Income Needs

As mentioned, many experts suggest that retirement savers should expect they will need at least 70% of pre-retirement income. However, we see that only 33% of working women (vs. 26% of men) reported anticipating needing at least that amount. Women may also need to treat this needed income level conservatively given the general expectation that they will live longer in retirement.

The desired levels of guaranteed income are roughly consistent between the genders. Notably, there is a wide range of desired guaranteed income levels for both men and women, with the bulk of interest in having between 40% and 80% of their income coming from guaranteed sources.

How much total annual income do you anticipate needing entering retirement (including Social Security) relative to your pre-retirement income? (e.g., your final annual compensation prior to retirement, such as salary, bonus, etc.)

What percentage of retirement income do you want to receive from guaranteed sources (pension, Social Security or annuities)?

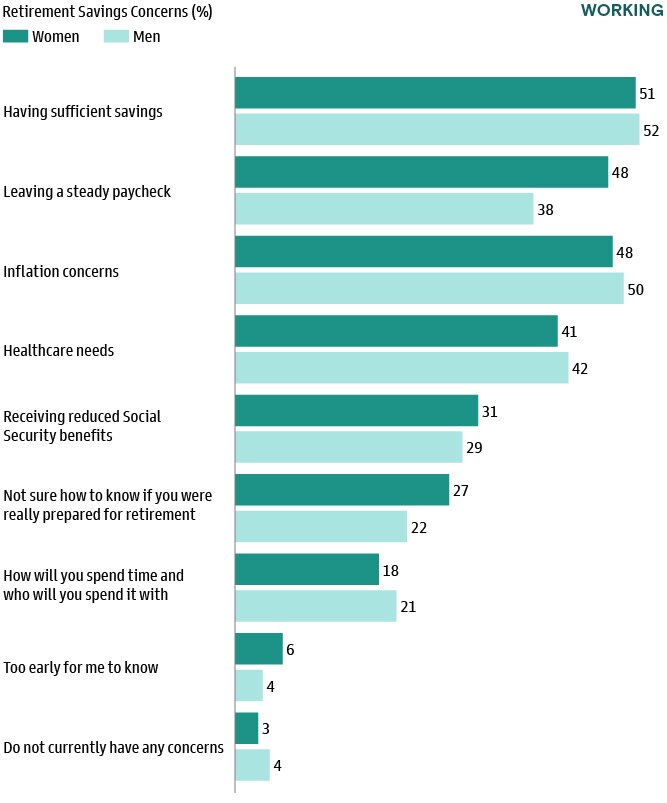

Leaving a Steady Paycheck is a Greater Concern for Women

While having sufficient savings, healthcare needs, and inflation concerns were similar for both women and men, there was a meaningful difference in concern with leaving a steady paycheck. Many working and retired respondents expressed concern over not being able to generate income from a job when they transition to retirement, but women reported this concern more so than men.

What concerns, if any, do you have about preparing for retirement?

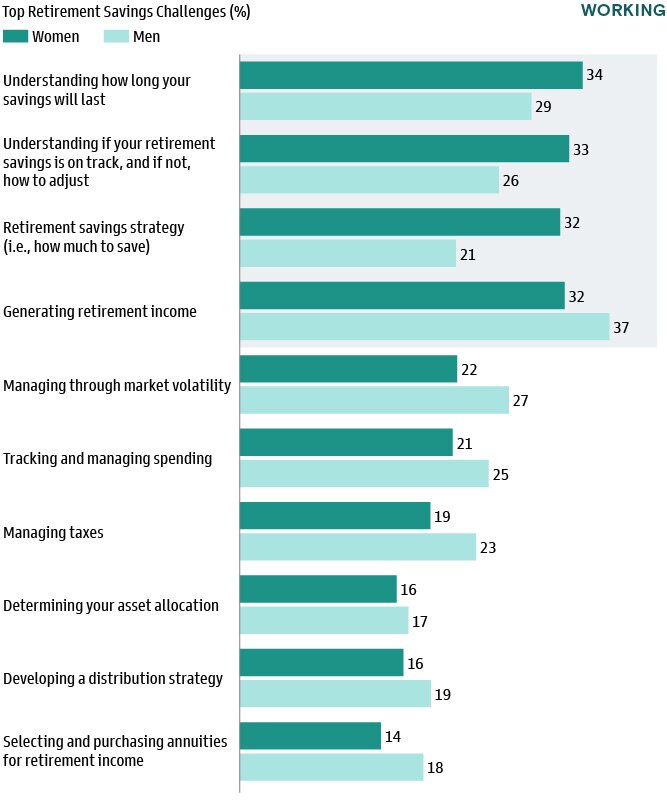

Top Challenges Women Face are Fundamental Retirement Planning Needs

The top challenges women reported preparing for retirement were concentrated on four primary retirement saving needs as shown in the chart. While men reported their top challenges ranged across a diverse number of topics, (e.g., managing taxes, managing through market volatility), women respondents focused on key issues needed to successfully retire.

This chart demonstrates the different challenges faced by different plan demographics and the benefit of providing advice and guidance across a range of topics to help plan participants successfully prepare for retirement.

What are the top challenges you face managing your retirement savings and investments where you would like advice / guidance? (Select up to three choices).

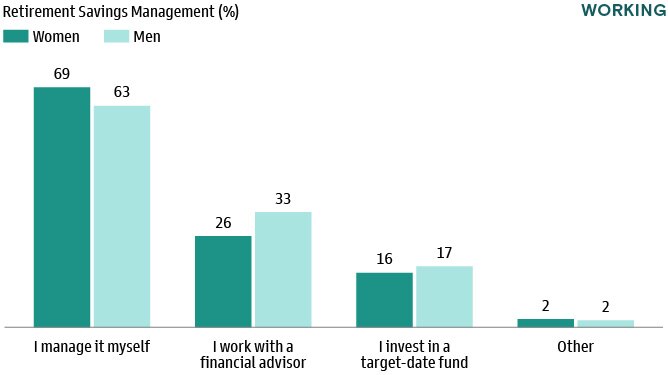

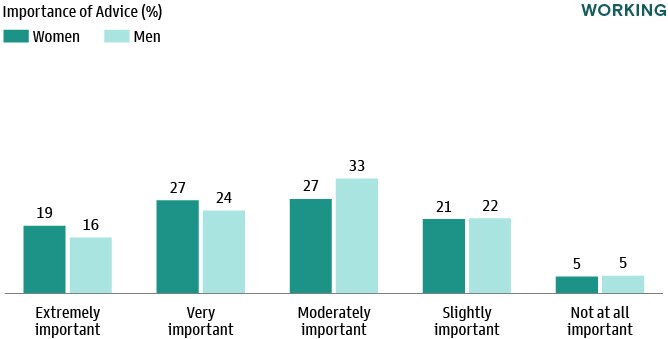

Despite Concerns and Confidence in Their Ability, Women are More Likely to Manage Savings Themselves

Given women reported facing many challenges managing their retirement savings, it may seem that women leverage financial help to navigate these challenges to a greater degree.

However, 69% of women respondents reported managing their savings themselves, while men were more likely to work with a financial advisor. Nearly all (95%) of survey respondents indicated they view financial help as important, but women were more likely to report that financial help is extremely or very important to successfully manage their retirement savings (46% for women, vs. 40% for men).

Do you manage your retirement savings yourself?

How important is it to receive financial help (education, advice, counseling) to successfully manage your retirement savings/income and investments?

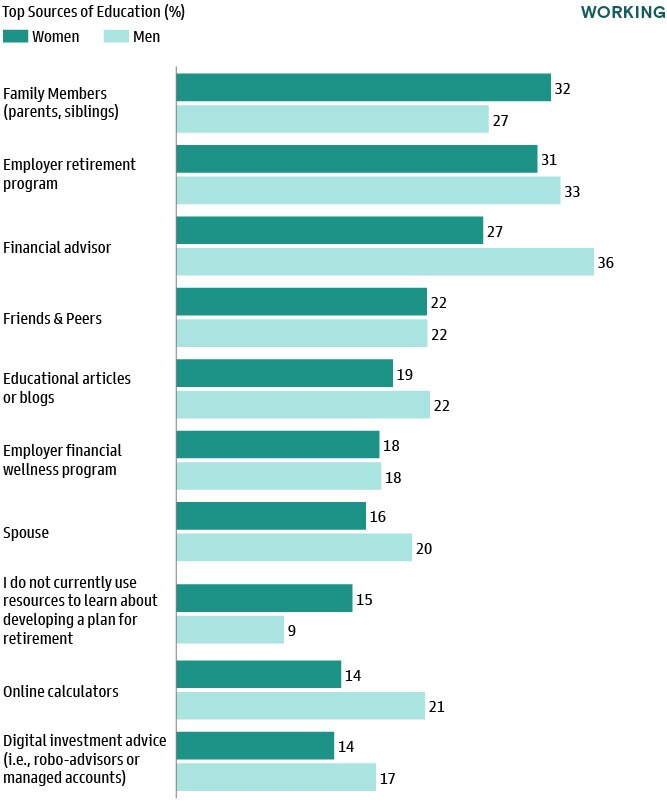

Top Sources of Help & Advice for Workers

When it comes to the notion of financial help, women and men respondents have varying opinions on what channels of education and advice are preferred. Men reported preferring to work with a financial advisor as their top choice of education and advice, while women respondents more often relied on their family members. Additionally, more women reported not using any resources to plan for retirement (15% of women, vs. 9% of men). Despite the added complexity in managing their retirement savings, women were less likely to leverage financial resources to do so.

Which of the following sources of education and advice do you currently leverage to learn about developing a plan for retirement? (Select up to three choices).

Save a copy as a PDF

Navigating the Financial Vortex: Women & Retirement Security

Related Insights

-

-

At a Glance: Retirement Planning for Women

December 7, 2022 This infographic highlights the different retirement trends American men and women experience in a visual format. Read More

×

Start the Conversation

Committed to providing you with the insights you need to build your practice.