April 24, 2023 |

GSAM Featured Insights

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsJuly 31, 2023 | 12 Minute Read

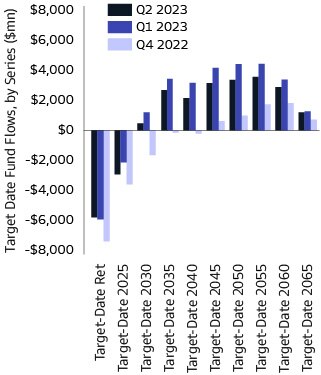

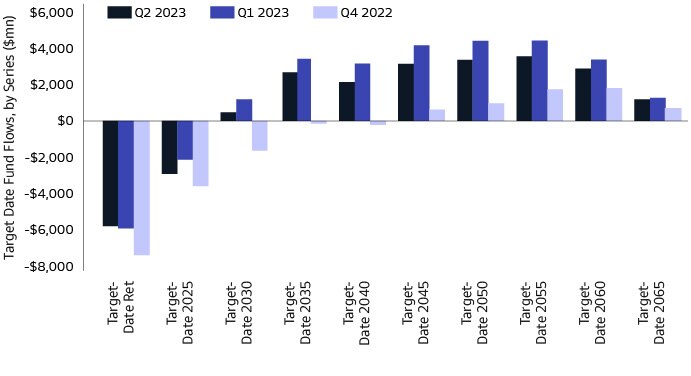

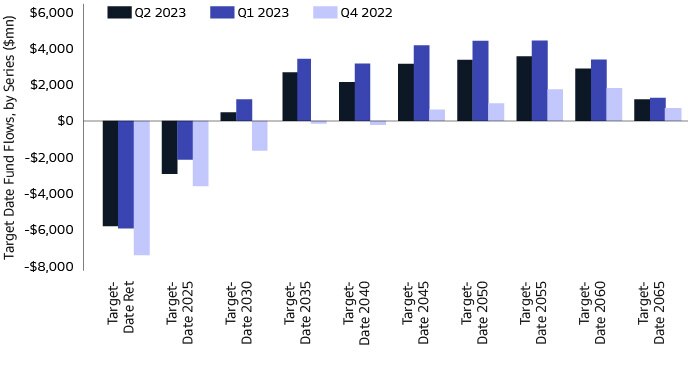

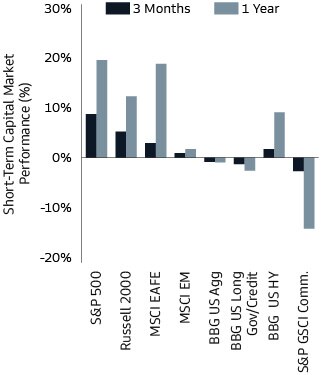

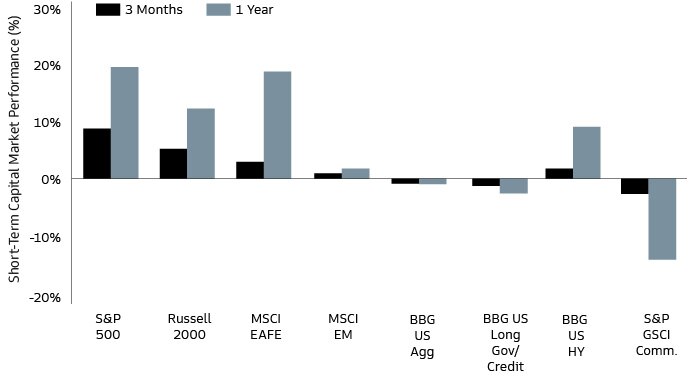

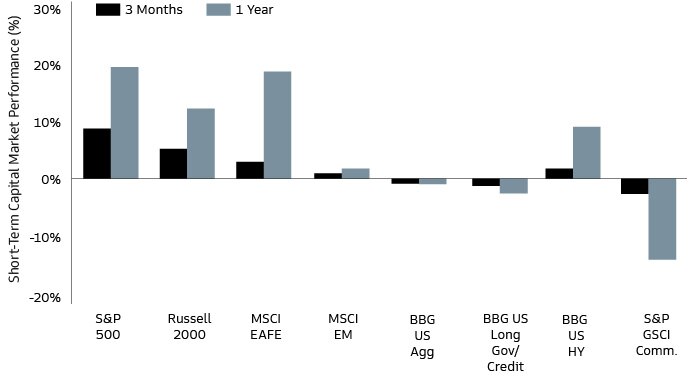

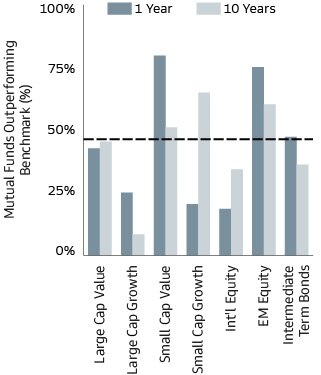

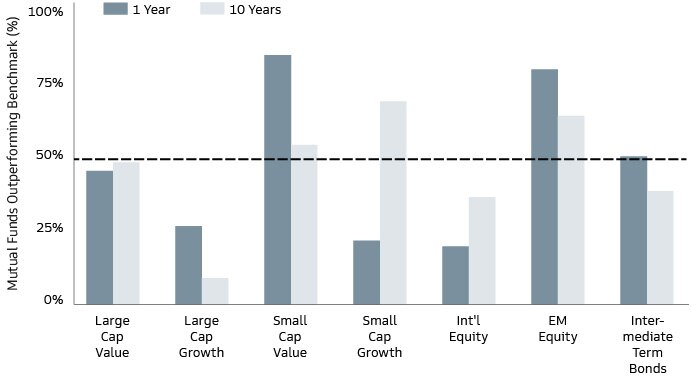

Fund flows for near-retirement target date vintages in Q2 continued to be negative, similar to prior quarters. On the other hand, net flows were positive in longer-dated categories but down quarter-over- quarter. Broadly we see some stabilization following a more challenged last year. At an asset class level, equity markets continued moving higher, especially in the US. Meanwhile, bonds gave back some of their earlier YTD gains and commodity losses continued. Active managers have performed best on a relative basis in small cap value and emerging market equities categories.

Source: Strategic Insight, Simfund. As of June 30, 2023. For open-end mutual funds

only. For illustrative purposes only.

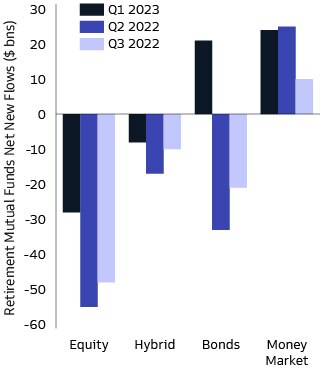

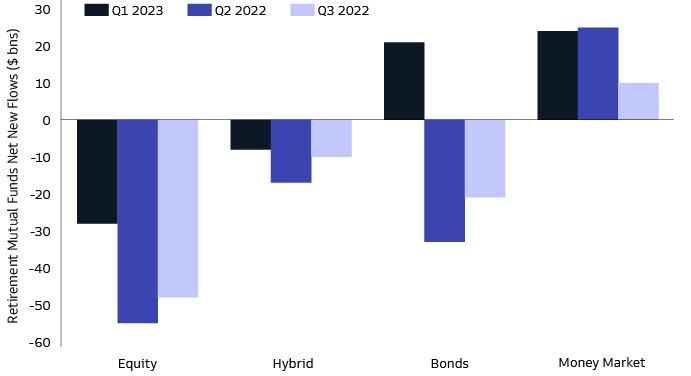

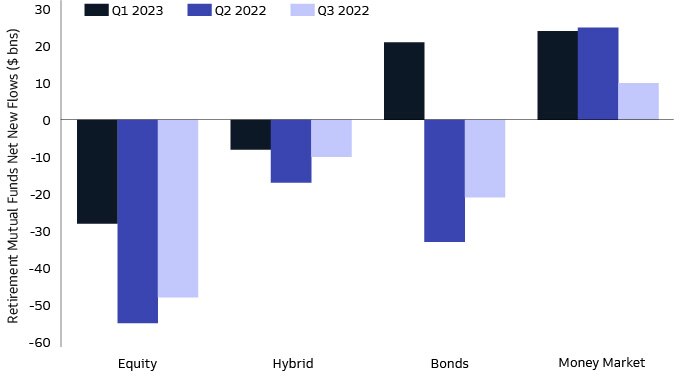

Source: ICI "The U.S. Retirement Market, First Quarter 2023." As of Q1 2023 (latest

available). For illustrative purposes only.

Source: Morningstar. As of June 30, 2023. Past performance does not guarantee future results, which may vary. For illustrative purposes only.

Source: Morningstar. As of June 30, 2023. Net of fees. Please refer to the disclosures

for benchmarks. Past performance does not guarantee future results, which may vary. For illustrative purposes only.

Please see end notes for additional disclosures and definitions

Industry Associations Request DOL Delay Implementation of Roth Catch-Up Contributions

In May 2023, Congressional leaders wrote to Treasury Secretary Yellen and IRS Commissioner Werfel seeking to ensure that Congressional intent is carried out with respect to several provisions of SECURE 2.0, including:

Lifetime Income for Employees Act, reintroduced in the House, seeks to make it easier for plan sponsors to include annuities in the plan’s qualified default investment alternative (QDIA) and default up to 50% of a participant’s balance into an annuity.

Retirement Fairness for Charities and Educational Institutions Act of 2023 was introduced by the House Committee on Financial Services to amend the securities law to allow 403(b) retirement plans to invest in collective investment trusts (CITs).

The Department of Labor (DOL) released its semi-annual non-binding regulatory agenda, which addressed several retirement-related items, including the definition of investment advice fiduciary.

The proposal would amend the definition of an investment advice fiduciary within the meaning of ERISA and Section 4975 of the Internal Revenue Code as well as evaluate class exemptions and propose amendments or new exemptions to ensure consistent protection of plan and IRA investors. The timeline for a proposed rule is noted as August 2023.

Other retirement related items addressed in the DOL Spring 2023 regulatory agenda include:

New litigation continues to pertain mostly to excessive fee cases, including alleged imprudent investment and recordkeeping fees and underperformance.

Key dismissals include three cases at the district court level alleging fiduciary breach for retaining Blackrock’s target date funds.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities.

Over the past few years, the drum beat of “personalization in Defined Contribution plans” has grown louder. The industry’s focus on improving retirement savings outcomes and the development of new technologies has enabled many new institutionalized advice services to bring personalized retirement planning advice to the forefront. In this In Focus, It’s Getting Personal section, we explore what is meant by personalization, what we believe is driving the need from a plan design perspective and certain considerations for plan sponsors.

Personalization in DC plans can have different meanings but at its core involves a fundamental principle.

Here are three ways plan sponsors might consider personalizing the retirement planning process.

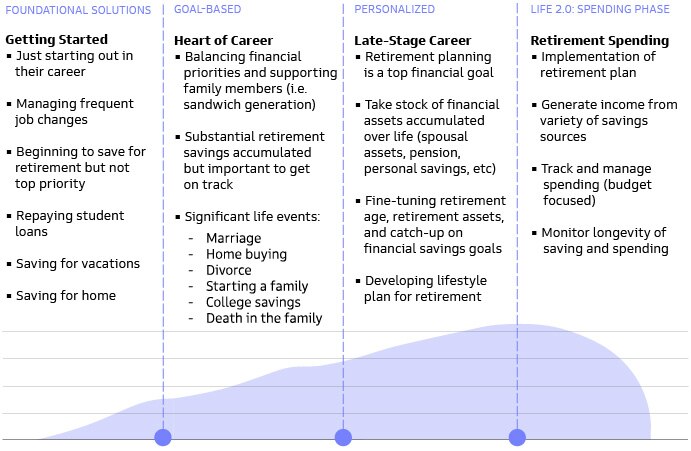

The trend toward personalization is a natural progression that has taken the industry from plan-level support to group-based or targeted support to now participant-level services. This progression of financial help (below) illustrates how the major developments across the industry have increasingly provided more personalized support to assist participants with their unique financial challenges.

Diagram shown for illustrative purposes only.

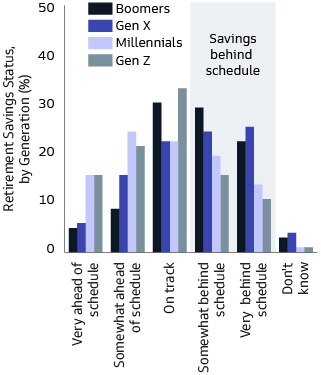

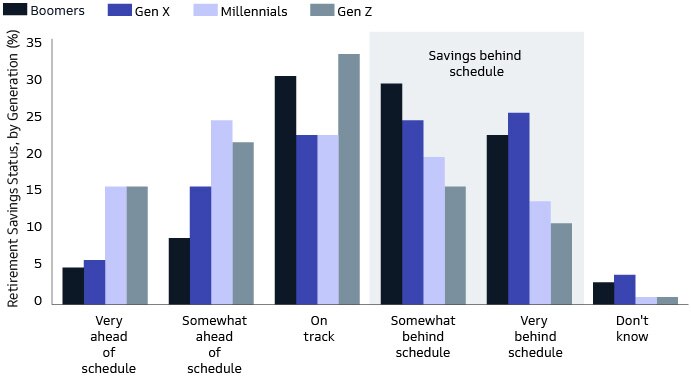

One challenge plan sponsors face is that participants have varying levels of retirement savings, a range of financial needs, and desire different levels of advice and support. As participants age and approach retirement, their financial lives often become more complex, while their retirement goals become more clear and specific. To navigate individual circumstances and target their specific goals, many seek a greater degree of personalization for their retirement strategy.

Participants have varying levels of retirement savings. Some are well ahead of schedule and others are well behind. Without providing personalized advice to help each individual tailor their savings and investment strategy, some may not adjust their strategy in time to reach retirement with sufficient savings.

Source: Goldman Sachs Asset Management Annual Retirement Survey & Insights Report, 2022

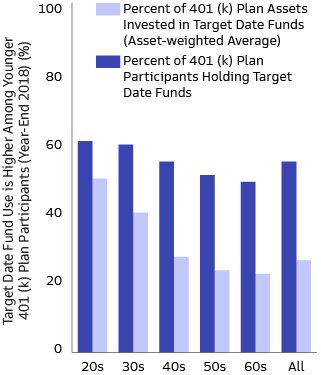

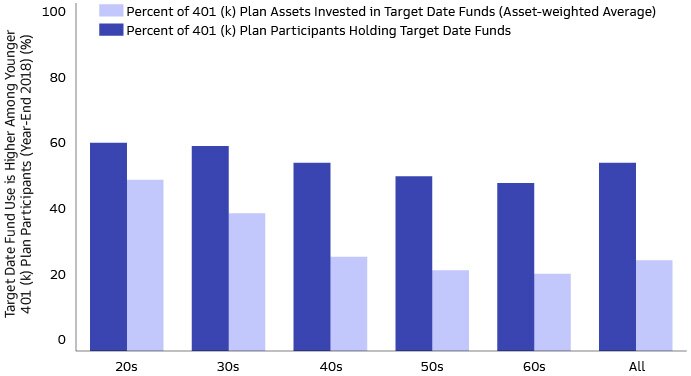

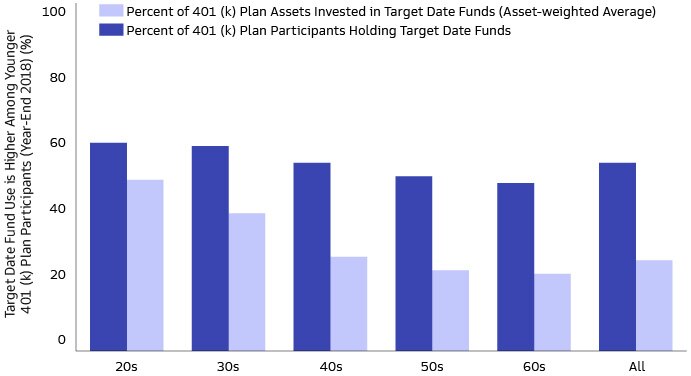

Target-date investors benefit from scale, asset allocation strategy and simplicity of design. However, as individuals age, the utilization of target date funds decreases, particularly for those with larger account balances, highlighting that they may be opting for a more personalized investment strategy.

Note: Funds include mutual funds, bank collective trusts, and life insurance separate accounts.

Source: Tabulations from EBR/ECI Participant-Directed Retirement Plan Data Collection Project. See Holden, VanDerhel and Bass 2021

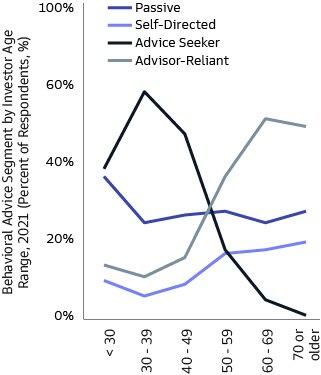

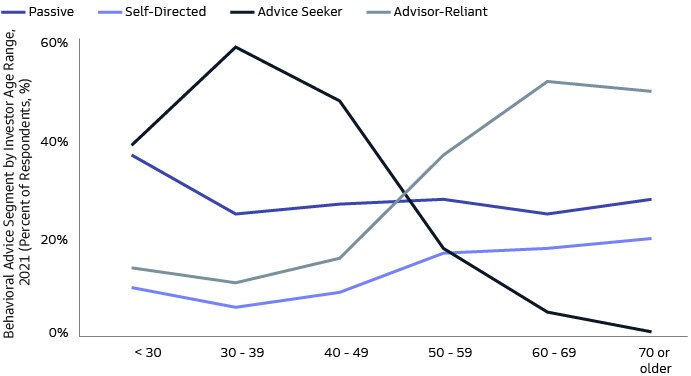

As we consider investment advice behaviors, while passive and self-directed investors are fairly consistent across age cohorts, we see a significant shift base on age from those seeking advice to those reliant on advice. This shift from advice seeking to advice reliant may align with the decline in target-date investors further illustrating the shifting desire for personalized advice as individuals age.

Source: Pheonix Marketing International, Cerulli Associates, U.S. Retail Investor Edition, 2Q 2022

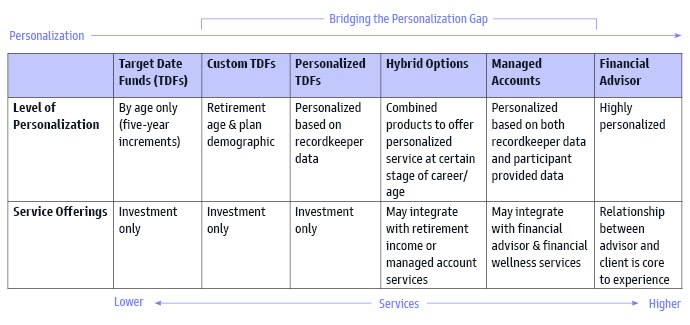

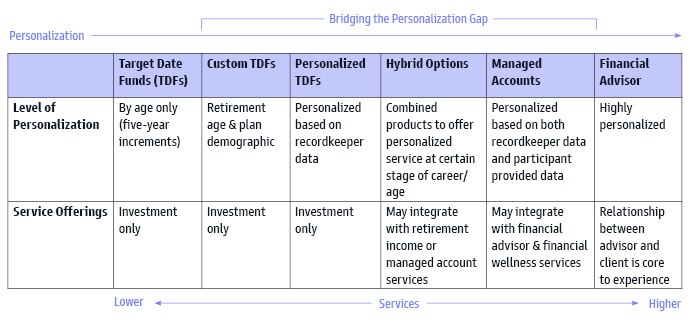

The market of institutionalized personalized solutions is developing to bridge the gap between two important services: target-date funds (TDFs) and financial advisors. TDFs are scalable, relatively low cost, easy to administer and solve a basic problem for plan participants… how do I allocate my investments? Financial advisors may be on the opposite side of the spectrum as they provide a highly customized and personalized experience, with tailored advice to each individual. The challenge is that it can be hard to scale these services for large populations.

The evolution in personalized services is bridging this gap to support a broader population of plan participants.

Source: Goldman Sachs Asset Management. As of July 2023.

A new category of emerging retirement solutions are hybrid options, which combine different products or services at different points in time to provide participants with solutions more aligned to their changing retirement needs. For instance:

These blended solutions highlight that developing integrated products may create a better participant experience and help participants with relevant options at key moments in their career.

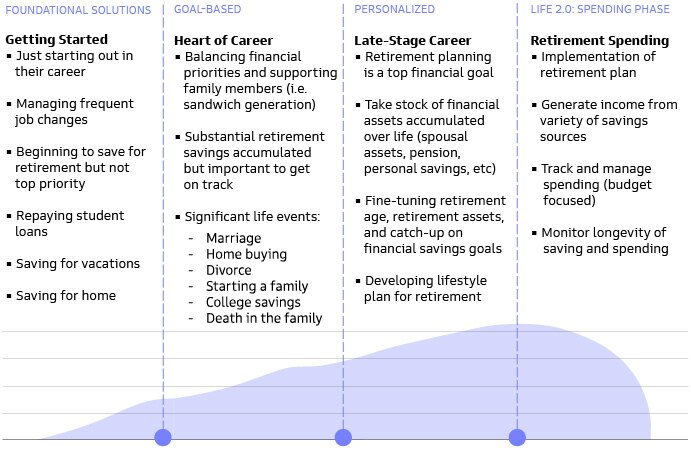

For plan sponsors focused on the overall financial wellbeing of their workforce, we believe the need to meet participants where they are and address their unique circumstances will become increasingly important. As discussed in our annual retirement research, Navigating the Financial Vortex, financial lives are becoming more complex and competing priorities make it difficult to save and invest for retirement (see illustrative financial journey below). Tailoring the approach in the following situations may help an individual better prepare for retirement.

For informational and illustrative purposes only.

Source: Goldman Sachs Asset Management. As of July 2023.

As a range of new options come to market, plan sponsors will have new choices to consider. As with other fiduciary decisions, plan sponsors will want to understand the service being offered, potential alternatives, and costs and fees, to name a few considerations. With the new generation of personalized solutions, there can be unique considerations for benchmarking given the service being offered may not match historical services.

Below are factors plan sponsors many want to consider when assessing personalized solutions.

The evolving nature of personalized services add a new dimension for plan sponsors.

Benchmarking and evaluating personalized solutions can be challenging because by design, each individual will have a tailored solution to meet their unique financial circumstances, including different investment objectives and risk approaches. Understanding a product’s underlying glidepath, investment methodology, personalization philosophy and investment controls can provide insight into its baseline investment process and how personalization will tailor the experience. Comparing the baseline investment approach allows for a more apples to apples comparison. And then the personalization philosophy can be evaluated to understand how individual portfolios are constructed. Without separating these two components it may be difficult to understand what is the driving factor of the performance.

Furthermore, we believe understanding the range of services offered in addition to the portfolio construction are key aspects of the analysis. In some cases, the planning component is an important part of the personalized services offered.

Developing greater personalized solutions is a natural progression in the DC industry as plan sponsors focus on providing broader financial wellbeing support for their employees. These solutions can help employees with decision support and evaluation of their financial challenges, and offer more relevant insight to drive actionable engagement. Plan sponsors may want to evaluate how these new developments fit into their overall plan design and can complement their existing education and advice services for employees.

Defined Contribution Quarterly - 3Q 2023

Committed to providing you with the insights you need to build your practice.

1Source: Georgetown University Center for Retirement Initiatives, June 30, 2023, https://cri.georgetown.edu/states/

Glossary

Small Cap: A stock from a public company whose total market value, or market capitalization, is about $250 million to $2 billion

Large Cap: A stock from a public company whose total market value, or market capitalization, is more than $10 billion

Passive Investors: Buys and hold investors

Self-Directed: Prefer to retain discretion

Advice-Seeking: Willing to cede discretion

Advice-Reliant: Prefer advisor discretion

A 401(k) plan is an employer-sponsored, tax advantaged defined contribution retirement plan. 401(k)s are often self-directed: plan participants decide how much they would like to contribute from their salary, and which investments from among those offered by the plan they would like to invest in.

Active Management refers to an investment approach where managers select investments for a portfolio in an attempt to outperform the benchmark index.

ERISA: Employee Retirement Income Security Act of 1974, as amended.

IRA: Individual Retirement Accounts

Volatility is a measure of variation of a financial instrument's price.

Risk Considerations

All investing is subject to risk, including the possible loss of the money you invest. Target Date Funds are subject to the risks associated with the underlying funds in which they invest. These risks change over time as the fund’s asset allocation strategy adjusts as it approaches its target date. There is no assurance any target date fund will achieve its investment objective. The principal value of an investment in a target date fund is not guaranteed at any time including at its target date.

You could lose money by investing in money market funds. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. The fund's sponsor has no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the fund at any time.

Equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Different investment styles (e.g., “growth” and “value”) tend to shift in and out of favor, and, at times, the strategy may underperform other strategies that invest in similar asset classes. The market capitalization of a company may also involve greater risks (e.g. "small" or "mid" cap companies) than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements, in addition to lower liquidity.

International securities may be more volatile and less liquid and are subject to the risks of adverse economic or political developments. International securities are subject to greater risk of loss as a result of, but not limited to, the following: inadequate regulations, volatile securities markets, adverse exchange rates, and social, political, military, regulatory, economic or environmental developments, or natural disasters.

Emerging markets investments may be less liquid and are subject to greater risk than developed market investments as a result of, but not limited to, the following: inadequate regulations, volatile securities markets, adverse exchange rates, and social, political, military, regulatory, economic or environmental developments, or natural disasters.

Investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity, interest rate, prepayment and extension risk. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. The value of securities with variable and floating interest rates are generally less sensitive to interest rate changes than securities with fixed interest rates. Variable and floating rate securities may decline in value if interest rates do not move as expected. Conversely, variable and floating rate securities will not generally rise in value if market interest rates decline. Credit risk is the risk that an issuer will default on payments of interest and principal. Credit risk is higher when investing in high yield bonds, also known as junk bonds. Prepayment risk is the risk that the issuer of a security may pay off principal more quickly than originally anticipated. Extension risk is the risk that the issuer of a security may pay off principal more slowly than originally anticipated. All fixed income investments may be worth less than their original cost upon redemption or maturity.

Investments in commodities may be affected by changes in overall market movements, changes in interest rates, or factors affecting a particular industry or commodity. Commodities are also subject to social, political, military, regulatory, economic, environmental or natural disaster risks.

Mutual funds are subject to various risks, as described fully in each Fund’s prospectus. There can be no assurance that the Funds will achieve their investment objectives. The Funds may be subject to style risk, which is the risk that the particular investing style of the Fund (i.e., growth or value) may be out of favor in the marketplace for various periods of time.

The above are not an exhaustive list of potential risks. There may be additional risks that should be considered before any investment decision.

General Disclosures

THESE MATERIALS ARE PROVIDED SOLELY ON THE BASIS THAT THEY WILL NOT CONSTITUTE INVESTMENT ADVICE AND WILL NOT FORM A PRIMARY BASIS FOR ANY PERSON’S OR PLAN’S INVESTMENT DECISIONS, AND GOLDMAN SACHS IS NOT A FIDUCIARY WITH RESPECT TO ANY PERSON OR PLAN BY REASON OF PROVIDING THE MATERIAL OR CONTENT HEREIN. PLAN FIDUCIARIES SHOULD CONSIDER THEIR OWN CIRCUMSTANCES IN ASSESSING ANY POTENTIAL INVESTMENT COURSE OF ACTION.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security, they should not be construed as investment advice.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY

JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

The website links provided are for your convenience only and are not an endorsement or recommendation by Goldman Sachs Asset Management of any of these websites or the products or services offered. Goldman Sachs Asset Management is not responsible for the accuracy and validity of the content of these websites.

Goldman Sachs does not provide legal, tax or accounting advice, unless explicitly agreed between you and Goldman Sachs (generally through certain services offered only to clients of Private Wealth Management). Any statement contained in this document concerning U.S. tax matters is not intended or written to be used and cannot be used for the purpose of avoiding penalties imposed on the relevant taxpayer. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you may disclose to any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be aware that a determination of the tax consequences to them should take into account their specific circumstances and that the tax law is subject to change in the future or retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. It should not be assumed that investment decisions made in the future will be profitable or will equal the performance of the securities discussed in this document.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices. The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein. The exclusion of “failed” or closed hedge funds may mean that each index overstates the performance of hedge funds generally.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the portfolio will achieve similar results. The index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark.

Bloomberg US Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including US Treasuries, investment grade corporate bonds, and mortgage backed and asset-backed securities.

Bloomberg US High Yield Index covers the universe of fixed rate, non-investment grade debt.

Bloomberg US Long Government/Credit Index is a broad-based flagship benchmark that measures the non-securitized component of long maturity (10+ years) bonds in the US Aggregate Bond Index. It includes investment grade, US dollar-denominated, fixed-rate Treasuries, government-related and corporate securities.

MSCI EAFE Index is a market capitalization weighted composite of securities in 21 developed markets.

MSCI Emerging Markets Equity Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

Russell 1000 Growth Index is an unmanaged index that measures the performance of the large cap growth segment of the US equity universe.

Russell 1000 Value Index is an unmanaged index of common stock prices that measures the performance of the large cap value segment of the US equity universe.

Russell 2000 Growth Index is an unmanaged index of common stock prices that measures the performance of the small cap growth segment of the US equity universe.

Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

Russell 2000 Value Index is an unmanaged index of common stock prices that measures the performance of the small cap value segment of the US equity universe.

S&P 500 Index is the Standard & Poor’s 500 Composite Stock Prices Index of 500 stocks, an unmanaged index of common stock prices.

S&P GSCI Commodity Index is a composite index of commodity sector returns, representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities.

Confidentiality

No part of this material may, without Goldman Sachs Asset Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

Date of First Use: July 28, 2023. 327134-OTU-1837866