July 12, 2023 |

Quarterly Investment Outlook

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsSeptember 5, 2023 | 6 Minute Read

Maral ShamlooEM Sovereign Economist Maral Shamloo |

Bregje RoosenboomLead Portfolio Manager, Fixed Income and Liquidity Solutions Bregje Roosenboom |

Angus BellEM Portfolio Manager Angus Bell |

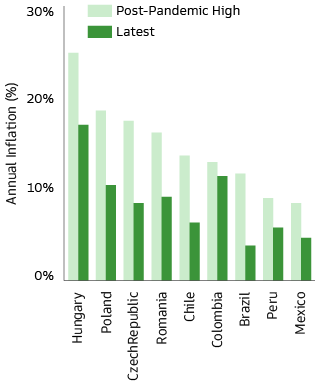

Inflation is falling rapidly across the emerging world in response to proactive monetary tightening by EM central banks, lower commodity prices compared to last year, supply chain improvements and stronger currencies (Exhibit 1).

Source: Macrobond, Goldman Sachs Asset Management. Based on data available as of August 16, 2023.

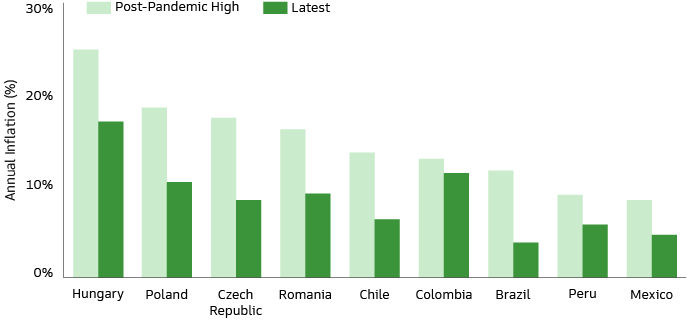

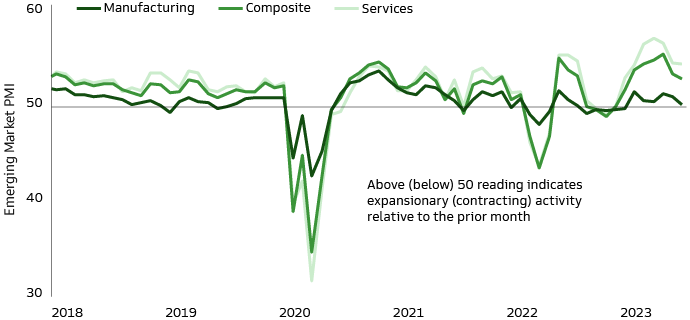

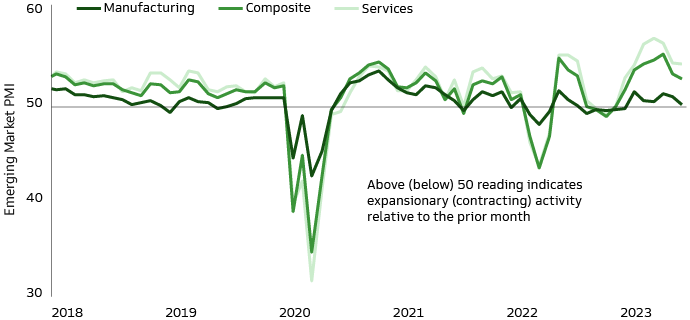

Inflation in emerging economies has fallen more quickly than in developed markets (DM), with central banks in the latter having to address larger domestically generated inflationary pressures. Although there has been some recent volatility in the commodity markets, we believe a significant degree of disinflation is still in the pipeline for the second half of 2023, particularly as growth momentum is slowing (Exhibit 2).

Source: Goldman Sachs Asset Management, Macrobond, S&P Global. As of July 2023.

The EM Local bond market experienced its most aggressive rate hiking cycle since its inception in 2021 and 2022. But many EM central banks are either easing monetary policy or are poised to do so. These banks delivered proactive and aggressive monetary tightening in response to sharply rising inflation in 2021 and 2022, resulting in the highest interest rates in a decade. Many concluded their hiking cycles late last year and have since been on hold. Faster-than-expected disinflation coupled with slowing growth and a high starting point for real rates have led several EM central banks to start cutting rates. Like the post-pandemic hiking cycle, central banks in Latin America (LatAm) have taken the lead, with the central banks of Chile and Brazil having already embarked on policy easing. We expect more EM central banks to follow suit over the next 18 months.

However, differences in how much inflation is falling suggest different central banks are likely to follow different monetary policy paths, underscoring the importance of active management. For instance, we anticipate further monetary tightening in Turkey and Russia, while many Asian central banks are likely to stay on hold. It is predominantly central banks in Central and Eastern Europe (CEE) and LatAm that are easing or set to ease. China’s central bank is also likely to continue to deliver targeted easing to counterbalance weaker-than-expected growth.

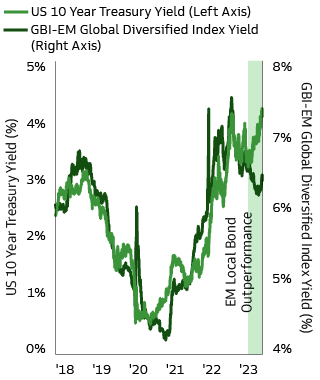

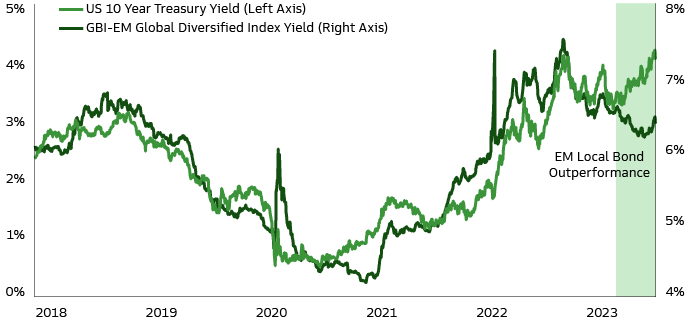

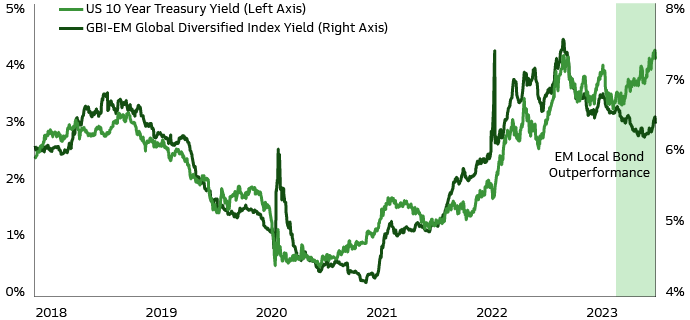

Assertive measures to counter inflation in recent years have resulted in high real rates and put EM central banks in a position to ease monetary policy ahead of DM central banks. EM local bonds, as measured by the J.P. Morgan Government Bond Index Emerging Markets (GBI-EM), have already rebounded sharply in anticipation of impending monetary easing, delivering a total return of 10% since their October lows and 7.5% year-to-date.2 Their performance has been in stark contrast with US rates, which have been volatile in 2023 (Exhibit 3).

Source: Macrobond, J.P.Morgan. As of August 24, 2023.

We believe EM local bonds’ strong performance has scope to continue. Historically there has been a strong correlation between peaks and troughs in annual inflation and subsequent peaks and troughs in EM local bond yields, particularly among high yield (HY) issuers. This suggests that the continued fall in EM inflation from recent peaks may coincide with additional declines in EM local bond yields, thereby extending the runway for potential GBI-EM returns.

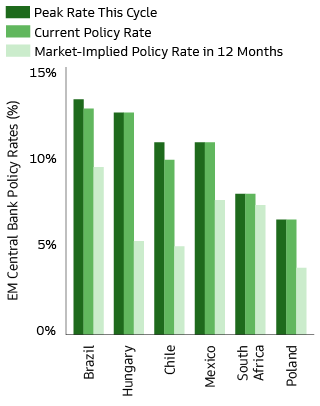

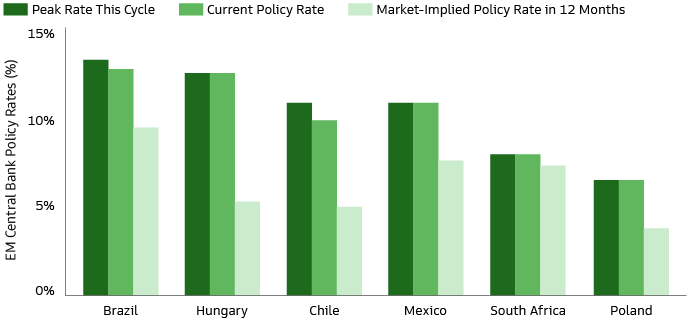

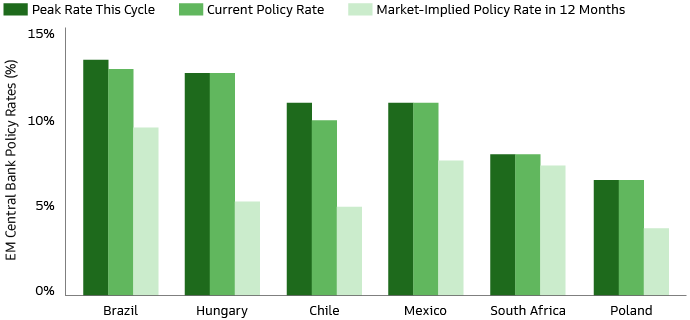

In addition, EM central bank actions tend to exceed market expectations both when they are tightening and loosening policy. For example, the Central Bank of Chile initiated its easing cycle with a larger-than-expected 100bps rate cut to 10.25%. The dovish tone conveyed in its July meeting minutes implies that forthcoming meetings may involve similarly large rate cuts.

EM local bonds are also being bolstered by favorable developments in EM currencies, which have historically detracted from total returns for investors in major developed markets. For context, a deterioration in current account positions amid supply constraints and the commodity price shock exerted significant downward pressure on EM currencies in 2022, reinforcing inflationary pressures for EM economies relative to major advanced economies. Fast forward to 2023, however, and EM currencies have strengthened, benefiting from attractive real rates and improved balance of payment positions (in response to aggressive monetary tightening and slower growth). Despite their appreciation and expectations of EM policy rate cuts, we think the appeal of EM currencies will persist as declining EM inflation should mean that EM real rates remain attractive.

A potential risk to EM currencies is a global or US downturn that would lead to the US dollar strengthening. Such an outcome could also impact EM local bond performance through heightened risk aversion. However, this is not our base-case scenario in the near term as recent signals suggest the US economy is still growing and inflation in the US is gradually falling.

In summary, we believe the combination of high starting real rates—following historic tightening in 2021 and 2022—and accelerating disinflation portends an expansion in market-implied pricing for policy easing within select EM local bond markets in the coming months. Additionally, despite EM central banks embarking on rate-cutting cycles, we believe EM local bonds are likely to continue providing attractive yields over core DM bonds.

Source: Macrobond, Goldman Sachs Asset Management, Bloomberg. As of August 28, 2023.

Committed to providing you with the insights you need to build your practice.

Assets under management as of May 31, 2023. Total Dedicated EMD assets includes all assets in funds and accounts, including cash and liquidity fund investments. AUM includes assets managed by GSAM and its investment advisory affiliates. Diversification does not protect an investor from market risk and does not ensure a profit. Past performance does not guarantee future results, which may vary.

1 As represented by the J.P. Morgan GBI-EM index.

2 Source: Bloomberg, J.P. Morgan, as of August 17, 2023.

Risk Consideration

Investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity, interest rate, prepayment and extension risk. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. The value of securities with variable and floating interest rates are generally less sensitive to interest rate changes than securities with fixed interest rates. Variable and floating rate securities may decline in value if interest rates do not move as expected. Conversely, variable and floating rate securities will not generally rise in value if market interest rates decline. Credit risk is the risk that an issuer will default on payments of interest and principal. Credit risk is higher when investing in high yield bonds, also known as junk bonds. Prepayment risk is the risk that the issuer of a security may pay off principal more quickly than originally anticipated. Extension risk is the risk that the issuer of a security may pay off principal more slowly than originally anticipated. All fixed income investments may be worth less than their original cost upon redemption or maturity.

When interest rates increase, fixed income securities will generally decline in value. Fluctuations in interest rates may also affect the yield and liquidity of fixed income securities.

Emerging markets investments may be less liquid and are subject to greater risk than developed market investments as a result of, but not limited to, the following: inadequate regulations, volatile securities markets, adverse exchange rates, and social, political, military, regulatory, economic or environmental developments, or natural disasters.

High-yield, lower-rated securities involve greater price volatility and present greater credit risks than higher-rated fixed income securities.

Investing in high-yield securities can be complex and involves a variety of risks and benefits. Non-investment grade fixed income securities and unrated securities of comparable credit quality (commonly known as “junk bonds”) are considered speculative and are subject to the increased risk of an issuer’s inability to meet principal and interest payment obligations. These securities may be subject to greater price volatility due to such factors as specific issuer developments, interest rate sensitivity, negative perceptions of the junk bond markets generally and less liquidity.

International securities may be more volatile and less liquid and are subject to the risks of adverse economic or political developments. International securities are subject to greater risk of loss as a result of, but not limited to, the following: inadequate regulations, volatile securities markets, adverse exchange rates, and social, political, military, regulatory, economic or environmental developments, or natural disasters.

The risk of foreign currency exchange rate fluctuations may cause the value of securities denominated in such foreign currency to decline in value. Currency exchange rates may fluctuate significantly over short periods of time. These risks may be more pronounced for investments in securities of issuers located in, or otherwise economically tied to, emerging countries. If applicable, investment techniques used to attempt to reduce the risk of currency movements (hedging), may not be effective. Hedging also involves additional risks associated with derivatives.

Investing in the N-11 countries is subject to risk of loss due to adverse social, political, regulatory or economic events in those countries. Investments into the N-11 countries may have to be implemented via equity swaps, equity index swaps, futures, participation notes, options and other derivatives which may involve additional financial counterparty risk. Changes in exchange rates may materially impact the value of investments in the N-11 countries. Financial advisers generally suggest a diversified portfolio of investments. Whilst the N-11 countries have some diversification in themselves, there may be times when these markets are all impacted in parallel by the same factors, which may make an investment in N-11 more volatile than a more diversified investment and an investor should only invest if he/she has the necessary financial resources to bear a complete loss of this investment.

Disclosures

This material is provided at your request for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

The website links provided are for your convenience only and are not an endorsement or recommendation by Goldman Sachs Asset Management of any of these websites or the products or services offered. Goldman Sachs Asset Management is not responsible for the accuracy and validity of the content of these websites.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this document and may be subject to change, they should not be construed as investment advice.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this document and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Investments in fixed-income securities are subject to credit and interest rate risks. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Goldman Sachs does not provide legal, tax or accounting advice, unless explicitly agreed between you and Goldman Sachs (generally through certain services offered only to clients of Private Wealth Management). Any statement contained in this document concerning U.S. tax matters is not intended or written to be used and cannot be used for the purpose of avoiding penalties imposed on the relevant taxpayer. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you may disclose to any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be aware that a determination of the tax consequences to them should take into account their specific circumstances and that the tax law is subject to change in the future or retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia Pacific: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

• Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

• Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

• Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

• Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

Canada: This document has been communicated in Canada by Goldman Sachs Asset Management LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. Goldman Sachs Asset Management LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

Brazil: These materials are provided at your request and solely for your information, and in no way constitutes an offer, solicitation, advertisement or advice of, or in relation to, any securities, funds, or products by any of Goldman Sachs affiliates in Brazil or in any jurisdiction in which such activity is unlawful or unauthorized, or to any person to whom it is unlawful or unauthorized. This document has not been delivered for registration to the relevant regulators or financial supervisory bodies in Brazil, such as the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários – CVM) nor has its content been reviewed or approved by any such regulators or financial supervisory bodies. The securities, funds, or products described in this document have not been registered with the relevant regulators or financial supervisory bodies in Brazil, such as the CVM, nor have been submitted for approval by any such regulators or financial supervisory bodies. The recipient undertakes to keep these materials as well as the information contained herein as confidential and not to circulate them to any third party.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Kuwait: The investments described in this document have not been and will not be registered, authorised, licensed or approved for offering, marketing or sale in the State of Kuwait pursuant to Law No. 31 of 1990 and Law No. 7 of 2010 nor by the Central Bank of Kuwait or any other relevant Kuwaiti government agency and shall not be offered or sold in the State of Kuwait, except in compliance with the above. No private or public offering is being made in the State of Kuwait, and no agreement relating to the sale of such investments will be concluded in the State of Kuwait. No marketing or solicitation or inducement activities are being used to offer or market such investments in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar: This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser.

These materials are presented to you by Goldman Sachs Saudi Arabia Company ("GSSA"). GSSA is authorised and regulated by the Capital Market Authority (“CMA”) in the Kingdom of Saudi Arabia. GSSA is subject to relevant CMA rules and guidance, details of which can be found on the CMA’s website at www.cma.org.sa.

The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Colombia: By receiving this document, and in case any contact is made with Goldman Sachs Asset Management, each recipient resident in Colombia acknowledges and agrees that it has contacted Goldman Sachs Asset Management at its own initiative and not as a result of any promotion or publicity by Goldman Sachs Asset Management or any of their respective agents or representatives. Colombian residents acknowledge that (1) the receipt of this document does not constitute a solicitation from Goldman Sachs Asset Management for its products and/or services, and (2) they are not receiving from Goldman Sachs Asset Management any direct or indirect promotion or marketing of financial and/or securities-related products and/or services.

This document is strictly private and confidential and may not be reproduced or used for any purpose other than evaluation of a potential investment in Goldman Sachs Asset Management’s products or the procurement of its services by the recipient of this this document or provided to any person or entity other than the recipient of this this document.

Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos.

Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o .Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

The opinions expressed in this research paper are those of the authors, and not necessarily of Goldman Sachs Asset Management. The investments and returns discussed in this paper do not represent any Goldman Sachs product.

This research paper makes no implied or express recommendations concerning how a client’s account should be managed. This research paper is not intended to be used as a general guide to investing or as a source of any specific investment recommendations.

Costa Rica: This is an individual and private offer which is made in Costa Rica upon reliance on an exemption from registration before the General Superintendency of Securities (“SUGEVAL”), pursuant to article 6 of the Regulations on the Public Offering of Securities (“Reglamento sobre Oferta Pública de Valores”). This information is confidential, and is not to be reproduced or distributed to third parties as this is NOT a public offering of securities in Costa Rica. The product being offered is not intended for the Costa Rican public or market and neither is it registered or will be registered before the SUGEVAL, nor can it be traded in the secondary market.

This report is produced and distributed by the Global Investment Research Division of Goldman Sachs, and is not a product of Goldman Sachs Asset Management. The views and opinions expressed may differ from those of Goldman Sachs Asset Management or other departments or divisions of Goldman Sachs and its affiliates. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. This information may not be current and Goldman Sachs Global Investment Research has no obligation to provide any updates or change.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein. The exclusion of “failed” or closed hedge funds may mean that each index overstates the performance of hedge funds generally.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Date of first use: September 5, 2023. 331660-OTU-1859495.