February 1, 2023 |

GSAM Featured Insights

Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsTHE KEY FEATURES OF SEMI-LIQUID FUNDS

July 7, 2023 | 5 Minute Read

The growth and innovation in private markets has allowed the introduction of new fund structures that help address different investor requirements. While semi-liquid funds are often valued for their ability to offer regular subscriptions and redemptions, their benefits extend well beyond the liquidity they can provide.

Compared to traditional drawdown funds, semi-liquid evergreen funds can offer immediate private markets exposure, provide investors with a regular source of income, and allow investors to remain invested for as long as they choose, with performance compounded over time.

Note: illustrative modelling, comparing a hypothetical traditional Private Credit fund to a hypothetical evergreen, semi-liquid Private Credit fund.

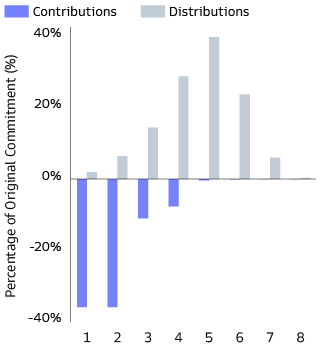

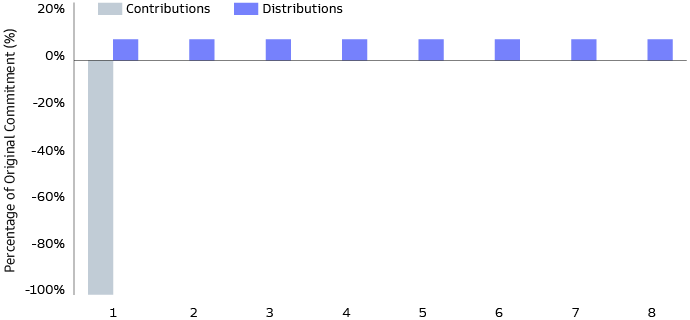

#1: Immediate Investment into Private Markets

Traditional Drawdown Fund

Source: Goldman Sachs Asset Management. For illustrative purposes only.

Capital pledged by investors is ‘called’ by the GP when investment opportunities present themselves.

A typical Private Credit fund would call and invest capital over the course of 3-4 years.

Investors maintain the use of pledged capital until it is called. They must carefully manage that capital to ensure that they can meet all their capital call obligations.

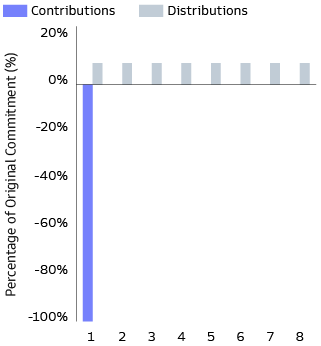

Semi-Liquid Fund

Source: Goldman Sachs Asset Management. For illustrative purposes only.

Investors contribute the full amount of commitment at the time of subscription; the capital is usually immediately invested in the fund (subject to subscription queues).

Semi-liquid funds typically have a ‘liquidity sleeve’, consisting of cash and / or public market investments, to hold investors’ capital if it cannot immediately be matched with a private investment opportunity.

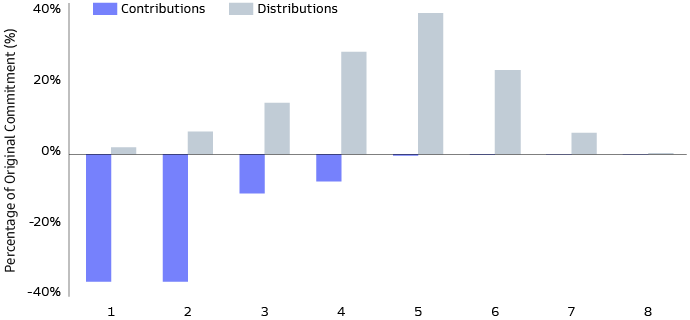

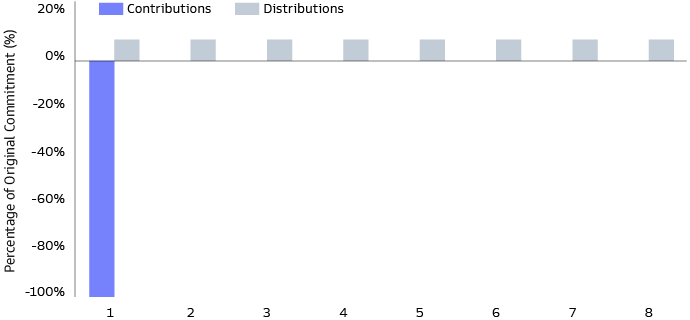

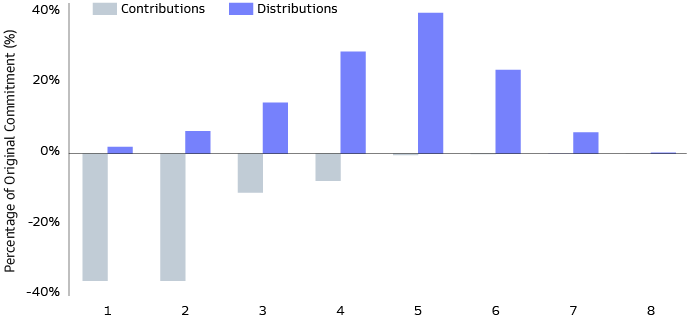

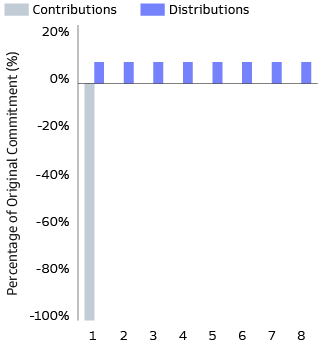

#2: Steadier Source of Income

Traditional Drawdown Fund

Source: Goldman Sachs Asset Management. For illustrative purposes only.

Senior credit funds offer regular source of income. Income received is a function of the invested amount – which in the early and late years may be smaller relative to the committed amount.

Distributions are at the discretion of the fund manager. As such, the investor should consider the capital in the fund as being locked up and unavailable for a period of several years.

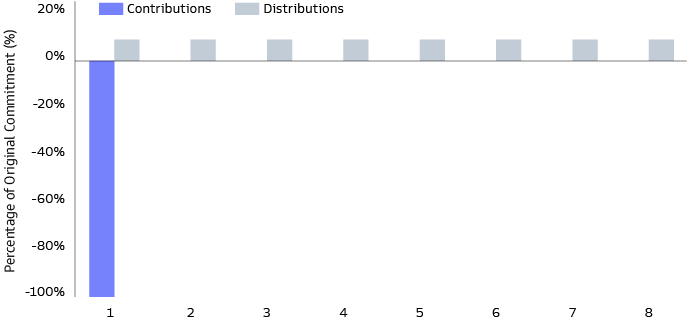

Semi-Liquid Fund

Semi-liquid funds typically target periodic distributions, e.g. on a monthly or quarterly basis, offering investors a regular source of income based on their full invested amount.

Investors have flexibility in timing their fund subscriptions and redemptions; monthly or quarterly windows are typical. However, semi-liquid funds typically feature redemption gates, which limit the amount investors are allowed to redeem in a given period.

Source: Goldman Sachs Asset Management. For illustrative purposes only.

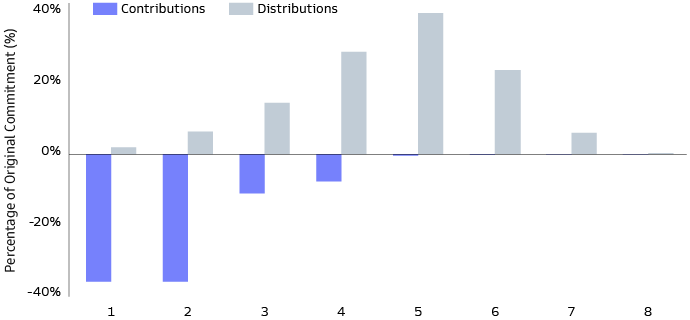

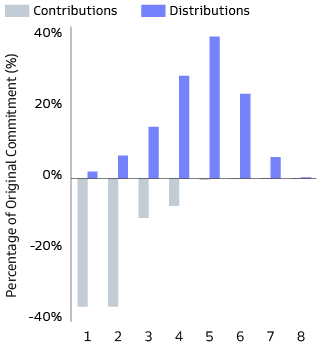

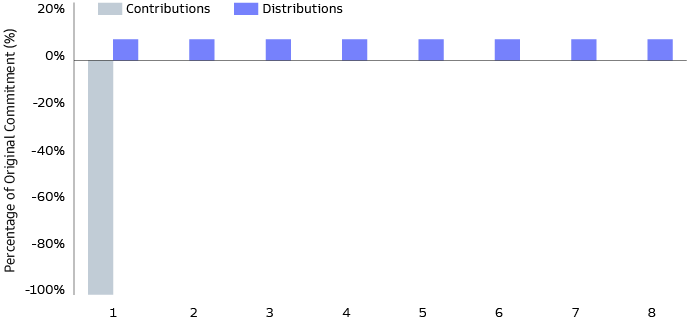

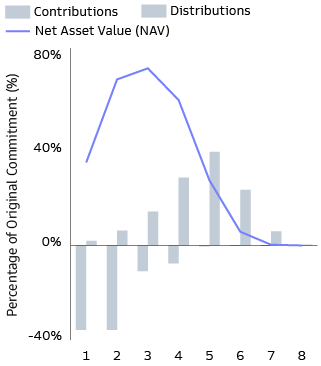

#3: Consistent Private Markets Exposure

Traditional Drawdown Fund

Source: Goldman Sachs Asset Management. For illustrative purposes only.

Managers of traditional drawdown funds can benefit from knowledge of the total capital available to deploy over the full investment period, making it easier to establish diversification (e.g., position sizing) parameters.

Investors’ exposure to private markets follows a ‘bell curve’, which ramps up during the early years of the fund as investments are made, and winds down in later years as investments are harvested.

On average, the fund’s net asset value peaks at 70-80% of the investor’s initial commitment.

Investors should optimize their private markets exposure via a steady commitment program to new funds each vintage year.

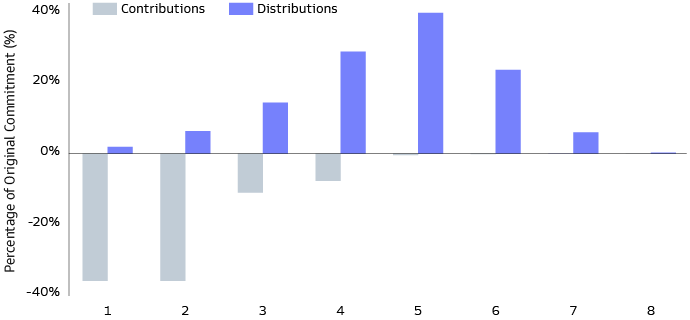

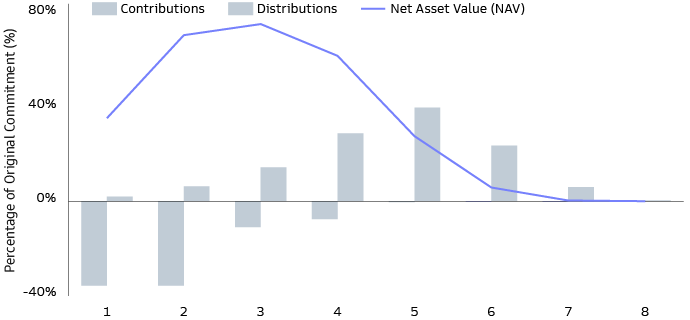

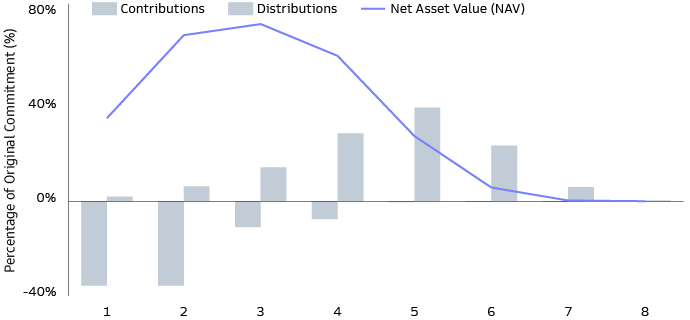

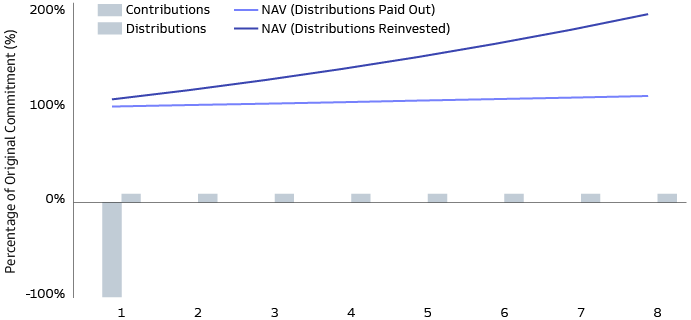

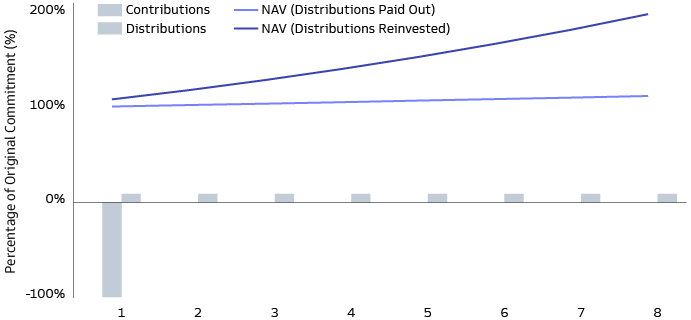

Semi-Liquid Fund

Source: Goldman Sachs Asset Management. For illustrative purposes only.

Investors benefit from consistent private markets exposure over the life of their investment.

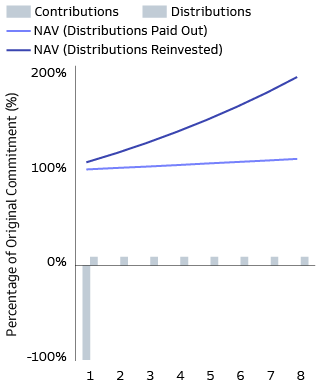

Investors can usually elect to receive their distributions in cash, or have them reinvested into the fund, allowing them to benefit from compound interest and accelerate the growth of their investment over time.

For investors, these funds also tend to be easier to manage than traditional drawdown funds, as they do not require regular re-investments given their perpetual nature.

Related Insights

×

Start the Conversation

Committed to providing you with the insights you need to build your practice.