August 4, 2022 |

Defined Contribution

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsSeptember 29, 2022 | 7 Minute Read

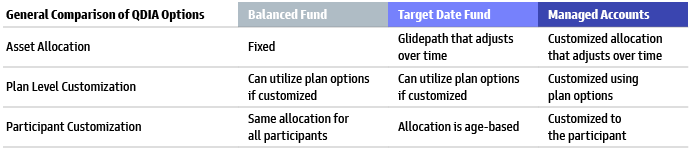

There has been tremendous focus on and increased utilization of default investing since the Pension Protection Act of 2006 (PPA). While several types of investments are eligible under the qualified default investment alternative (QDIA) rules, TDFs have captured the bulk of the assets. We believe the market share among the QDIA types may be poised for greater change, as outlined in the following pages.

The PPA provides a safe harbor for plan fiduciaries investing participant assets in certain types of investments in the absence of participant investment direction. The DOL’s final regulation provides conditions that must be satisfied in order to obtain fiduciary relief, and indicates that fiduciaries are not relieved of the liability for the prudent selection and monitoring of qualified default investment alternatives (QDIAs).

Source: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/fact-sheets/final-rule-qdia-in-participant-directed-account-plans.pdf

Source: PSCA’s 64th Annual Survey, published 2022.

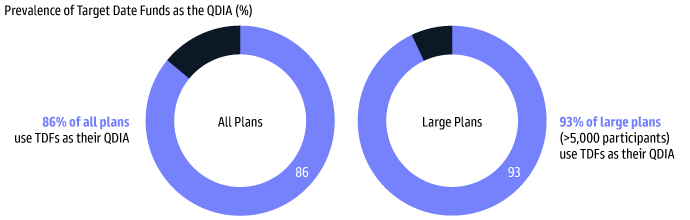

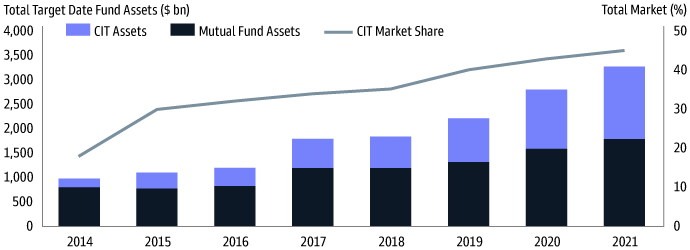

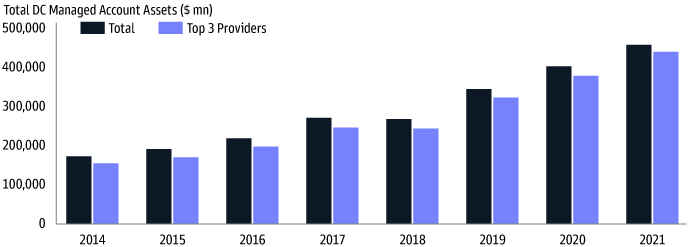

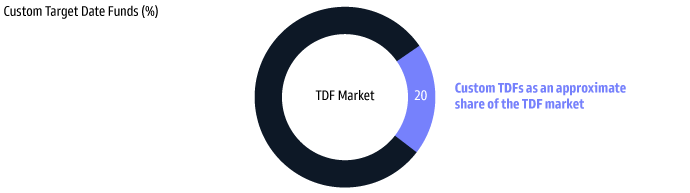

While there are multiple acceptable QDIA options, target date funds have been the prevalent choice to date. The target date market has grown rapidly over the last decade to an estimated $3.27 trillion; industry assets have increased by nearly 10x. Assets continued to grow in 2020 despite a drop in participant contributions. By comparison, the DC managed account landscape is roughly 15% of the size of the total target date market.

Source: Morningstar, 2022 Target-Date Strategy Landscape. Data as of 12/31/2021.

Source: Cerulli, U.S. Retirement Edition, 1Q 2022, 1Q 2021, 1Q 2019 and 1Q 2017.

Source: DCIIA Custom TDF Survey, published May 2020.

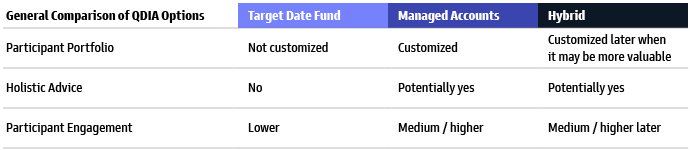

Certain Considerations

What comes next? (R)evolution of QDIA Options?

Will target date funds continue their dominance as QDIA options in DC plans? Will industry trends emerging around the desire for (1) retirement income and (2) increased personalization/customization lead to an evolution of target date offerings or even a revolution of QDIAs altogether?

A number of target date managers are evolving their offerings to focus on the decumulation aspect through the use of annuities and managed payout structures. Managed account services are focused on the desire for increased personalization and, in some cases, are also addressing retirement income. The concept of a hybrid QDIA (sometimes referred to as a dynamic QDIA) has emerged.

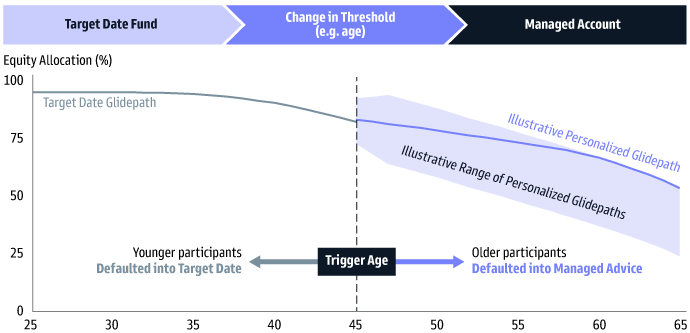

What is a Hybrid QDIA?

A hybrid QDIA is an approach in which a participant’s default investment starts as one type of investment (such as a target date fund) and, upon reaching a certain threshold (e.g., age), automatically transitions to a different type of investment (such as a more retirement-focused solution like a managed account).

Source: Goldman Sachs Asset Management. For illustrative purposes only.

According to a recent DCIIA research paper that interviewed plan sponsors who adopted a hybrid (dynamic) QDIA, a primary reason they did so was to provide participants the age-appropriate service and advice they needed to optimize their retirement outcomes. The paper noted that participants’ investment sophistication, or lack thereof, helped drive the plan sponsors’ decision to adopt the dynamic QDIA.

Additional Considerations

Committed to providing you with the insights you need to build your practice.

Disclosures

ERISA Client Disclosure

THESE MATERIALS ARE PROVIDED SOLELY ON THE BASIS THAT THEY WILL NOT CONSTITUTE INVESTMENT ADVICE AND WILL NOT FORM A PRIMARY BASIS FOR ANY PERSON’S OR PLAN’S INVESTMENT DECISIONS, AND GOLDMAN SACHS IS NOT A FIDUCIARY WITH RESPECT TO ANY PERSON OR PLAN BY REASON OF PROVIDING THE MATERIAL OR CONTENT HEREIN. PLAN FIDUCIARIES SHOULD CONSIDER THEIR OWN CIRCUMSTANCES IN ASSESSING ANY POTENTIAL INVESTMENT COURSE OF ACTION.

This material is provided at your request for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant. This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Views and Opinions

This information is not a formal recommendation. Views and opinions are current as of the date of this presentation and may be subject to change.

Third Party Sources

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Confidentiality

No part of this material may, without Goldman Sachs’ prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

Date of first use: September 29, 2022. 285345-OTU-1647206