August 18, 2022 |

Pension Solutions

Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsDEFINED BENEFIT EROA ASSUMPTIONS 2022: FINDING A BOTTOM?

October 03, 2022 | 12 Minute Read

Executive Summary

Expected return on asset (EROA) assumptions continue to move lower in both the corporate and public defined benefit (DB) plan universes. In 2021, the average corporate DB EROA assumption fell below 6% for the first time, driven by a combination of higher allocations to long duration fixed income and lower return forecasts for many asset classes. Many public DB plans also continued to lower return expectations, with adjustments predominately linked to reduced capital markets assumptions. Some public plans have also put in place programs to systematically lower this assumption if actual results in any given year exceed actuarial expectations.

Nonetheless, these assumptions may be finding a bottom. The rise in US Treasury yields and risk-free rates have led to a re-rating of the expected returns for various asset classes. Indeed, our Goldman Sachs Asset Management strategic long-term assumptions have been upwardly revised this year across parts of the equity, fixed income, and alternatives spheres. Of course, continued shifts by corporate plans to fixed income as part of de-risking actions and the efforts described above by some public plans to bring down these assumptions may counteract higher return expectations for individual asset classes.

Each year, corporate and public DB pension plans in the US, as well as various other institutional investors, are required to develop an EROA assumption. Plan sponsors typically make a number of decisions to determine an appropriate methodology for calculating an EROA assumption.

As we have done in prior years, this paper aims to:

- Provide some historical context around how these assumptions have changed over time;

- Illustrate recent actions by plan sponsors in making adjustments;

- Describe certain practices for setting an EROA assumption;

- Answer common questions facing plan sponsors; and

- Outline our EROA forecasts for a series of illustrative portfolios that may be helpful as plan sponsors consider their approach to these issues.

Introduction - Running the Numbers Once Again

Each year hundreds, if not thousands, of DB plan sponsors go through an exercise of developing an EROA assumption for their plans. While this exercise is familiar to many plan sponsors and is required in many circumstances to comply with accounting and financial reporting requirements, there are still many questions as to how plan sponsors develop an EROA assumption.

The balance of this paper seeks to provide context on what we have observed plan sponsors doing over the last 12 months, describe certain practices on setting an EROA assumption, and outline a set of expectations that takes into account today’s environment. While our work highlights that many institutional investors have lowered these assumptions in recent years, increases in interest rates may mean the multi-year decline in these assumptions be coming to an end.

Update on Corporate and Public DB Plan EROA Assumptions

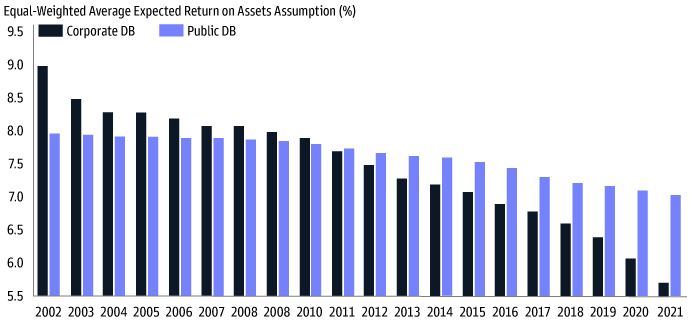

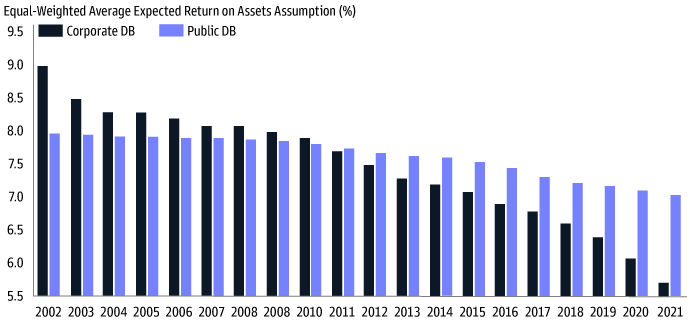

EROA assumptions for DB pension plans have been on a downward trend for many years (see Exhibit 1). Last year was no exception, as the average EROA assumption for corporate and public DB plans declined yet again. The average corporate DB EROA assumption has declined almost 250 basis points since 2008. The downward trend is similar for the public plan universe, though the average decline during that same period was only around 90 basis points.

Although year-over-year changes tend to be quite small, the cumulative impact on plan sponsor financials can be material. Across the entire DB universe, an EROA change measured in just a few basis points can impact billions of dollars in municipal pension liabilities and corporate earnings.

Exhibit 1: Average EROA Assumptions for Corporate and Public DB Plans Continue to Decline

Source: Goldman Sachs Asset Management, company reports, and Center for Retirement Research at Boston College. Data through fiscal year-end 2021.

We continue to find that the dispersion of assumptions in corporate DB plans is quite wide, which is partially attributable to the varied approaches many sponsors are taking to asset allocation and investment strategy. Sponsors that are total return focused (and, therefore, have higher allocations to public equities and alternatives) continue to maintain assumptions of 7% or higher, while plan sponsors utilizing a liability driven investment (LDI) approach (and, therefore, have higher fixed income allocations) tend to use notably lower assumptions. For example, the average allocation to fixed income for corporate DB plans that reported an EROA below 6% is 63%, while the average allocation to fixed income for plans that reported an EROA of 7% or higher is only 33%.1

While EROA assumptions have trended lower and at a slower pace in the public DB community, we find that there tends to be more similarity in the return assumption that public plans are using. Over 90% of public DB plans used a return assumption in 2021 of between 6.5% and 7.5% (inclusive).2 Compared to corporate plans, these sponsors have generally not adopted de-risking strategies and tend to employ investment strategies that are more similar in nature.

These averages will likely fall again in 2022. In the appendix of this report, we have detailed examples of corporate and public DB plans that announced the EROA assumption they were using in the current fiscal year. In many cases, the 2022 assumption is lower than what was used in 2021. Nonetheless, as we explore later in this report, the rise in interest rates and downward adjustment to the valuation of many assets in 2022 has contributed to an increase in the long-term return assumptions associated with many asset classes. This may help to stem the tide of EROA reductions and may lead some plans to increase this metric in future years.

A Reminder on the Process of Setting an EROA Assumption

There is limited guidance for setting an EROA assumption, and as a result, plan sponsors must make a number of decisions, often with input from their actuary and/or consultant. Ultimately, a sponsor’s auditor must review the fairness of the assumptions used for pension disclosures in the financial statements. As there is no “one-size-fits-all” approach to the development of an EROA assumption, multiple factors might be considered based on the plan’s individual circumstances and methodology. The remainder of this section attempts to highlight some of the more common questions that plan sponsors face when developing an EROA assumption.

• How should a plan sponsor define “long-term?” We believe that forward looking asset class assumptions should generally cover the next 10 years and include some reflection of current market conditions. For example, return assumptions should properly reflect today’s yield environment.

• How much reliance should be placed on historical performance versus forward looking assumptions? The name alone (Expected Return on Assets) suggests that this exercise is intended to primarily be based on forward looking assumptions. We understand that some sponsors may take into account actual historical returns on their portfolios when developing their EROA assumption and believe that history can serve as a useful guide. However, if a plan sponsor recently shifted a large portion of the portfolio from risk assets to fixed income, we would expect the EROA assumption to be adjusted appropriately, with less reliance on historical plan returns.

• What should plan sponsors focus on first – the EROA assumption or long-term strategic asset allocation? For corporates, a higher EROA assumption may have a positive impact on its income statement in the current fiscal year but could require a higher allocation to risk assets. This could result in a greater chance of future shortfalls relative to the EROA, as well as increased funded status volatility and uncertainty about meeting obligations. Conversely, a higher allocation to long duration fixed income leads to a lower EROA assumption (and higher pension expense) but may also result in fewer negative surprises relative to EROA and lower funded status volatility. For public plans, a lower EROA assumption more directly translates into a lower funded status position and higher contribution requirements for employers. Hence, it is important that plan sponsors reviewing the various trade-offs manage them appropriately, taking into account their obligations as plan fiduciaries.

• Should the forward-looking return assumption be based on an arithmetic (average annual) or geometric (compound) return forecast? With the lack of specific guidance, some have suggested that arithmetic returns are consistent with financial statement reporting for actual fiscal year returns. That said, geometric return forecasts more closely resemble the return pattern that plans are likely to experience.

• How should investment manager excess returns/alpha be factored into the calculation? If a plan is invested with active managers, it is likely that plan sponsors include alpha assumptions into the overall EROA calculation. We believe these alpha forecasts could be developed at the asset class level (rather than at the portfolio level). A weighted average using the plan’s strategic asset allocation targets might then be used to generate a total portfolio alpha expectation.

• Should return expectations be gross or net of investment management fees and/or other pension-related expenses, such as PBGC premiums? We have observed investment management fees factored into EROA assumptions. That is, forward looking assumptions can be built with return assumptions net of investment manager fees. In many cases, other pension-related expenses, including PBGC premiums, are reflected in another pension expense line item—service cost. Since most plans take this

approach, we generally have not seen PBGC costs factored into EROA assumptions.

Adjusting EROAs Based on Actual Portfolio Performance

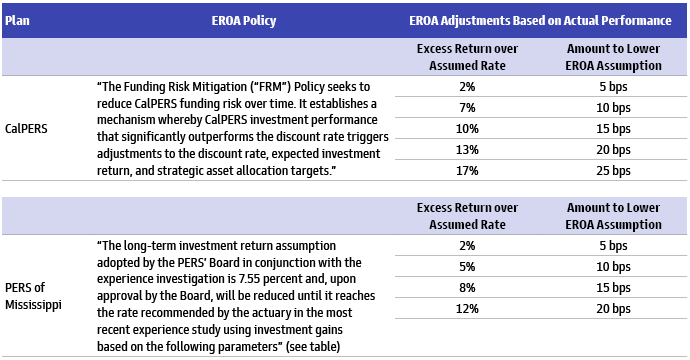

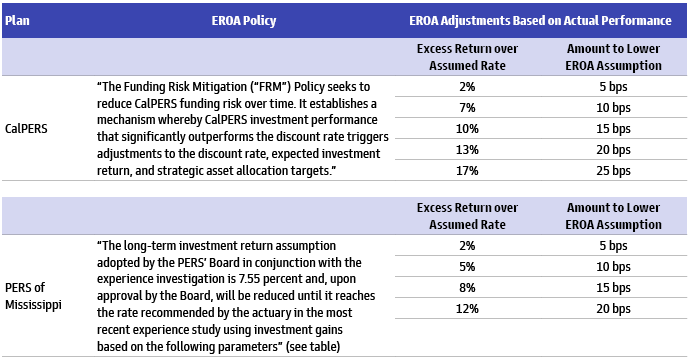

For some public DB pension plans, the EROA assumption can be a sensitive subject. This assumption is generally used by public pension plans to discount their liabilities. Therefore, lowering the assumption, holding all else constant, would increase the value of a plan’s liabilities and lower its funded status. This, in turn, could have implications for contribution requirements, among other things.

In recent years, some plans have put policies in place to mechanically lower their EROA assumption if actual returns in any given year exceed their long-term estimate. We have detailed two examples below. Elsewhere in this paper we have argued that return assumptions may be finding a bottom after over 10 years of steady reductions. In some cases, plans may even be able to argue for an increase to the assumption. Nonetheless, some plans may continue to see this percentage lowered if they have a system in place to adjust it downward following periods of outperformance.

Exhibit 2: Illustrative Public DB EROA Policies

Source: Public filings and Goldman Sachs Asset Management. As of August 31, 2022. For discussion purposes only.

How Have Return Expectations Changed?

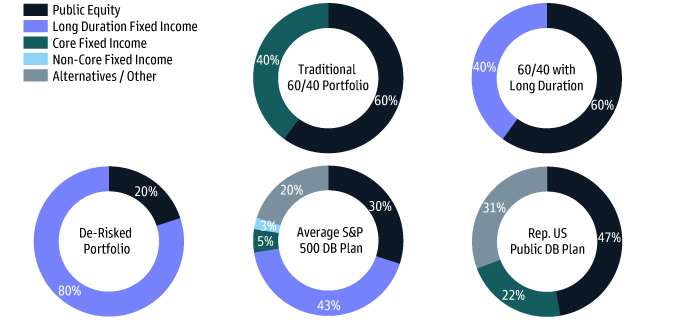

With the understanding that there are a number of variables that go into setting an EROA, plan sponsors might be wondering what range of reasonable expectations exist today and how those expectations may have changed in the last 12 months. We have outlined our view on some illustrative portfolios in Exhibit 3 below. In addition to three common illustrative portfolios, we have also included two illustrative portfolios intended to be representative of typical corporate and public DB plan allocations.

Exhibit 3: Representative Corporate and Public DB Pension Portfolios

Source: Goldman Sachs Asset Management, company reports, and Center for Retirement Research at Boston College. As of August 8, 2022. For illustrative purposes only. 60/40 portfolios and De-Risked portfolio are hypothetical portfolios based on common industry standards. The average S&P 500 pension plan is based on company reports. US public DB plan is for illustrative purposes only and based on data from the Center for Retirement Research at Boston College.

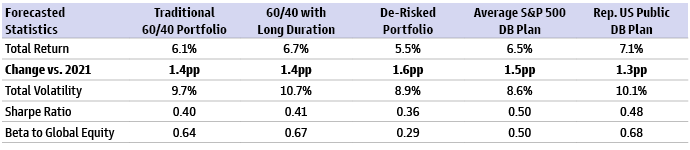

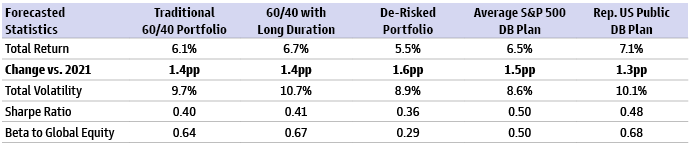

Using our most recent set of capital market forecasts, we have generated a series of sample outputs to help illustrate potential impacts on EROA assumptions and have also included the year-over-year change. As seen in Exhibit 4, return forecasts have moved higher over the past year for each of the five representative portfolios.

Exhibit 4: Illustrative Forecasted Returns for Representative Portfolios

Source: Goldman Sachs Asset Management. As of August 1, 2022. All numbers reflect Multi-Asset Solutions’ strategic assumptions as of June 30, 2022. Assumptions reflect generic active management for each asset class. “Change vs. 2021” reflects the difference between June 30, 2022 and June 30, 2021 assumptions. Strategic long-term assumptions are subject to high levels of uncertainty regarding future economic and market factors that may affect future performance. They are hypothetical indications of a broad range of possible returns. Please see additional disclosures.

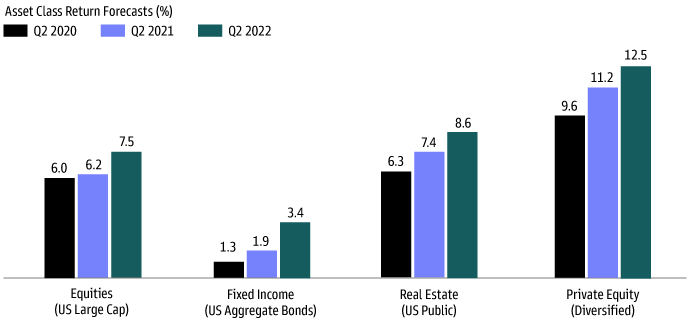

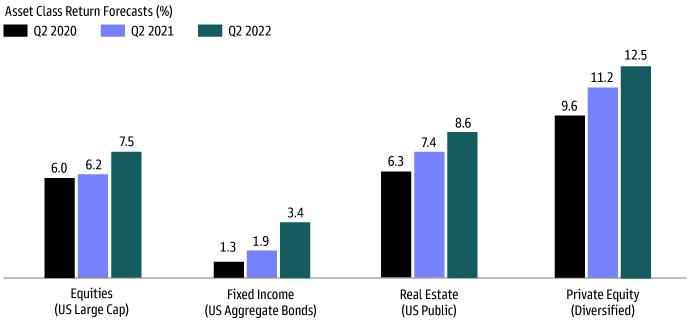

This has been driven by the upward revision to many individual asset class return forecasts. In Exhibit 5, we detail how Goldman Sachs Asset Management forecasts, as derived by our Multi-Asset Solutions team, have progressed over the past two years for a sample of asset classes. The increase in US Treasury yields and risk-free rates has been a catalyst for the upward revisions to return expectations for certain asset classes.

Exhibit 5: Illustrative Forecasted Returns for Representative Portfolios

Source: Goldman Sachs Asset Management. As of August 1, 2022. All numbers reflect Multi-Asset Solutions’ strategic assumptions as of June 30, 2022. Assumptions reflect generic active management for each asset class. “Change vs. 2021” reflects the difference between June 30, 2022 and June 30, 2021 assumptions. Strategic long-term assumptions are subject to high levels of uncertainty regarding future economic and market factors that may affect future performance. They are hypothetical indications of a broad range of possible returns. Please see additional disclosures.

Conclusion

Setting an EROA is a necessary task for plan sponsors each year; however, there is no universally agreed upon approach. In our experience, plan sponsors typically want to choose a methodology and maintain that approach annually. Naturally, a large shift in the plan’s strategic asset allocation or a meaningful change in return expectations by asset class would likely require a change in EROA. While each plan sponsor may have its own set of unique circumstances, we have seen a downward trend in EROA assumptions consistent with shifting asset allocations and expectations for market returns. Nonetheless, the tide may be turning as individual asset class long-term return expectations have been rising. As we outlined above, there are a series of practices that plan sponsors may want to keep in mind when setting these projections.

Related Insights

-

-

July 20, 2022 | Pension Solutions

Corporate Pension Quarterly 2Q2022: Braving the Bear

July 20, 2022 The S&P 500 officially entered bear market territory in June 2022, posting the worst first-half performance since 1970. Amid heightened uncertainty but still-elevated funded levels, plan sponsors are taking a closer look at liability-hedging, hibernation, and de-risking strategies. Corporate Pension Quarterly 2Q 2022: Braving the Bear highlights potential investment approaches and strategies to consider in the face of market volatility as plans approach their “end state” portfolios. Read More

×

Start the Conversation

Committed to providing you with the insights you need to build your practice.