August 7, 2023 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsAugust 7, 2023 | 15 Minute Read

James AshleyInternational Head of Strategic Advisory Solutions James Ashley |

Simona GambariniSenior Market Strategist, Strategic Advisory Solutions Simona Gambarini |

The French philosopher Auguste Comte is often quoted by the economic community as saying, “Demography is destiny.” We believe he was wrong. Demographics are just one factor influencing economic and social outcomes across countries, but it can play a critical role in shaping public policy, inflation and investment decisions over long-run time horizons. This article addresses the many effects of the most important demographic trends, looking at the macro implications, how countries adapt policies to changing populations, and critically, what that means for investors.

Any significant change in the population—for example, average age, dependency ratios, life expectancy or birth rates—can have material implications for an economy. Demographic change can influence the underlying growth rate of an economy, structural productivity growth, living standards, savings rates, consumption and investment. It can influence the long‐run unemployment rate and equilibrium interest rate, housing market trends and the demand for financial assets. Economies with rapidly expanding prime-age population cohorts (ages 25-54) enjoy the benefits of improved potential gross domestic product (GDP) growth, but also face the challenge of creating sufficient employment to satisfy the needs and desires of that population. By contrast, aging societies typically must wrestle with the reduction of their labor force and rebalance their economies to devote a much higher share of national income to social and health care (irrespective of whether that is publicly or privately financed). The challenges vary according to the dynamics and parameters of the population pyramid. In many cases, the questions are both absolute and distributional; both types of questions matter for investors seeking to allocate capital efficiently.

These questions have immediate practical importance. A number of the world’s major economies are in the midst of the most rapid demographic change since World War II, with the potential to reshape the macro and investment landscape for decades to come. In the US, declining fertility rates and an aging population are not as much of a challenge as in other countries, yet the labor force participation rate is at multi-decade lows—a secular trend that has been catalyzed by the exogenous shock to the labor market created by COVID-19 lockdowns.

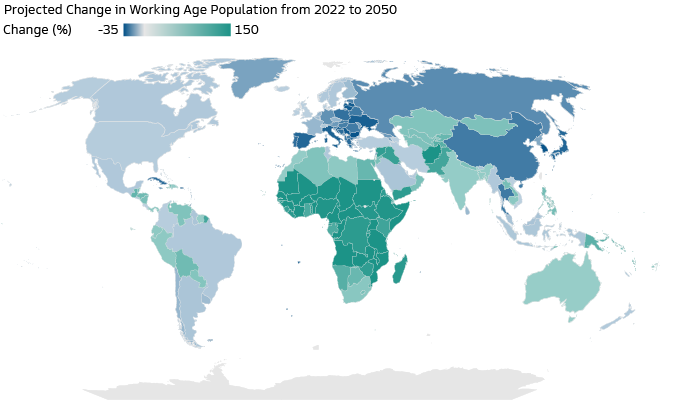

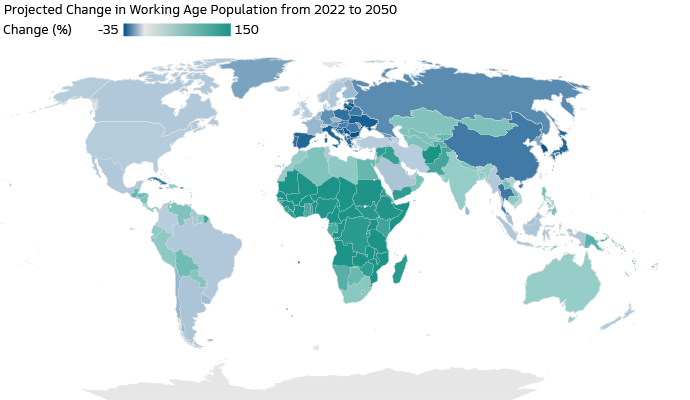

By contrast, China faces a Lewis Turning Point1 as its surplus labor disappears while the aging population grows—a combination that could fundamentally redefine the contours of the world’s second-largest economy with potential global consequences. Put simply, demographics strongly suggest weaker trend growth in China over the years ahead. Nor is China alone in facing that kind of demographic pressure; Germany, Italy and large parts of Eastern Europe may need to confront the implications of shrinking labor forces as the baby boom generation retires.

Conversely, many emerging-market economies have much more positive demographic profiles. For example, India recently overtook China as the most populous country in the world, and its youthful profile will yield a demographic dividend for decades to come.2

Source: United Nations, Haver Analytics and Goldman Sachs Asset Management. As of June 17, 2023. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. For illustrative purposes only.

Measuring the impact of population aging on economic growth can be complex and multi-faceted. Any meaningful economic analysis may benefit from considering demographics in conjunction with other long-term trends like the increased development and adoption of artificial intelligence (AI), efforts by governments to decarbonize, and the fracturing of the global economy.

Other factors being equal, less favorable demographic impulses suggest potential growth will be weaker. This is primarily a function of a shrinking labor contribution. For example, the US Congressional Budget Office estimates increased female participation rates and the emergence of the baby boom generation combined to have added approximately 1.7 percentage points per year to average growth in US potential real GDP growth from 1948 to 2001.3 As the population ages, the size of the working-age population tends to decrease. This can lead to a decline in the labor force and potentially lower economic output.

But demographics can also impact other components of potential growth beyond labor market volumes (headcount). The aging of the workforce could also depress investment, thus having a negative impact on capital formation. For instance, older workers may draw down investment assets to pay for expenses as they near retirement, or they may pivot to fixed income or cash as their risk profile becomes more conservative with age. Older individuals tend to have greater healthcare needs that can increase healthcare expenditures. A shift in expenditures to healthcare from sectors with higher productivity might potentially reduce overall productivity and affect growth as a result.

For a variety of reasons, the statistical relationship between the aging of the workforce and productivity is believed to be hump-shaped, albeit with factors such as health and education levels contributing to variations in peak productivity.

The aging of many economies coincides with the increasingly widespread adoption of generative AI, which may go some way to supporting productivity at the aggregate level. Goldman Sachs Global Investment Research (GIR) estimates that generative AI could—depending on its capability and adoption timeline—raise annual US labor productivity growth by just under 1.5 percentage points over a 10-year period following widespread adoption.4 This could eventually increase annual global GDP by 7%.

While AI could be the next driver of GDP, it is unclear how workers of varying age, skills and economies will be affected by potential displacement, particularly in fields including customer and legal services, coding and content creation.

Thus while demographics could have a significant negative impact on economic growth rates in many major economies—taking into account how aging societies may spur innovation—the conclusions are more complex and nuanced.

The net impact of aging on inflation depends on the relative strength of a number of cross-currents. We believe aggregate nominal demand will probably decline (a disinflationary effect) as a rising share of the population retires (and income levels typically decline), but aggregate supply will also fall (an inflationary effect) as the labor force diminishes in size. Given that (full) retirement is a complete cessation of economic production, but retirees will only partially (if at all) reduce their demand, the net impact of these two high-level forces is likely to be inflationary.

The aggregate data may not tell the full story, however; shifts in spending patterns at the regional or sector level can be equally powerful. For example, if aging societies display differentiated spending patterns, this can mean expenditure is redirected toward sectors where there is existing supply-side capacity to absorb it, in which case the inflationary impact is dampened considerably. Micro (sector-level) may be as important as macro (broad-economy) trends.

Similarly, one of the economic lessons from the post-COVID reopening is that sector-level labor market dislocations (whether surfeits or shortfalls) from structural breaks can have major impacts on wage dynamics. Careful micro-econometric analysis may be required on a case-by-case basis, rather than overarching grand pronouncements. And just as when considering the impact of aging on growth, so too with inflation it is important to consider other contemporaneous structural changes. For example, technology and the wide adoption of AI may provide significant disinflationary forces across many economies, but with uncertain impacts on the capacity (and therefore inflationary consequences) for health and social care that are likely to see higher demand in aging societies.

Critically, the impact of an aging population on economic growth and inflation can vary across countries and depends on factors such as government policies, labor market dynamics and healthcare systems. Policymakers can adjust immigration policies, labor market regulations, and investments in healthcare and education to address the challenges posed by an aging population and promote sustainable long-term economic growth. That said, with China—one of the major sources of labor supply for the past 20 years—also suffering from deteriorating demographics, advanced economies may start to struggle to import labor from such places either via migration or outsourcing of production.

Overall, we think that population aging across most developed markets and China will largely be inflationary, especially when coupled with decarbonization and deglobalization. That will potentially create a profoundly different inflation dynamic for central banks to contend with relative to the past 15 years. Demographics point to structural stickiness to inflation, suggesting higher nominal policy rates in the decades ahead. This would be a reversal from the post-Global Financial Crisis era of low inflation and policy rates stuck at the effective lower bound, with possibly far-reaching consequences for fixed income investors.

An aging and longer-lived population also creates fiscal challenges around health and social care and the financing of state pensions. Those challenges are exacerbated when—as is the case for many developed markets—they come with a decline in fertility rates. On a neutral assumption of broadly unchanged net migration flows, one of the many consequences of those demographic dynamics is to raise questions about the sustainability of public pension provisions on existing parameters such as retirement age, contributions, payouts and payment protections. For example, in the UK, where demographics are not particularly adverse, the Office for Budget Responsibility estimates that the cost of state pension provision will rise from 4.8% of GDP currently to 8.1% by 2070.5

Policymakers and the broader community of stakeholders may need to debate whether those costs are socially acceptable, or if there could be a need for a reappraisal of the appropriate levels of provision. Such debates will not be purely technocratic or take place against a sterile backdrop, as the recent French demonstrations against an increase in the retirement age illustrate.6 These are vital questions that touch on fundamental elements of the social contract. What is the appropriate level of entitlement that citizens can expect to access? At what age? What level of taxation is required to finance that? And what sort of immigration policy is needed to meet those requirements?

Just as the economic impact of demographics has the potential to be significant, so too may be the investment consequences. For long-term investors who are looking to build robust portfolios beyond a single economic cycle, population dynamics play an important role. While no investor can accurately predict what the coming decades have in store for financial markets, understanding the implications of aging demographics for markets can help investors make more informed investment decisions and build better portfolios.

One asset class that may be more easily linked to demographics is real estate.7 Housing demand depends on the age structure of a society and on residential population trends. The demand for residential property is therefore more directly affected by demographic changes than in many other markets. As residents age, the average household size shrinks so more apartments are needed per capita. We think this may benefit certain sectors such as senior living facilities. On the other hand, a shrinking population can be negative for the housing market because empty buildings are typically not pulled down. While according to the United Nations the global population is expected to grow over the next 60 years, some countries like Japan—whose population is in decline—may face structural housing challenges. Infrastructure could also be transformed to support the needs of aging populations including roads, waste management and digital technology.

By contrast, the impact of demographics on other financial assets is sometimes less clear-cut. According to a 2016 study from the San Francisco Fed, the main channel through which demographics affect real interest rates is the increase in life expectancy.8 Rising life expectancy tends to be associated with lower interest rates because people save more in anticipation of a longer retirement period. In principle, as the global population becomes older, one can expect interest rates to be lower in the long run. That said, the age structure may also capture the persistent component of interest rates. Recent dynamics point to potentially higher yields over the next decade, which is consistent with an environment of higher inflation.

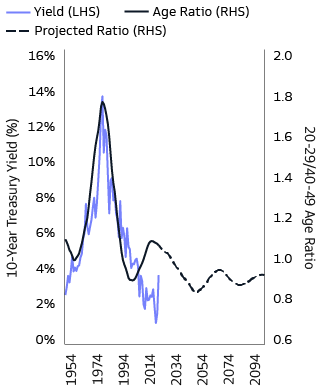

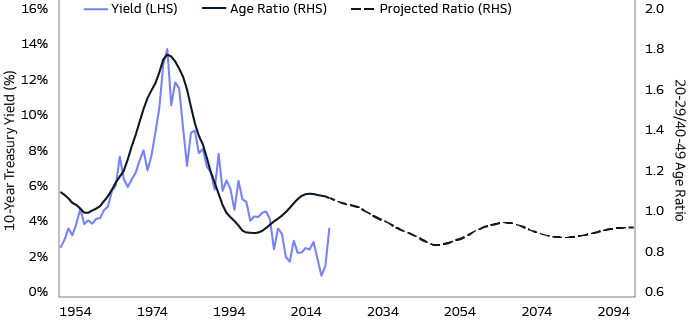

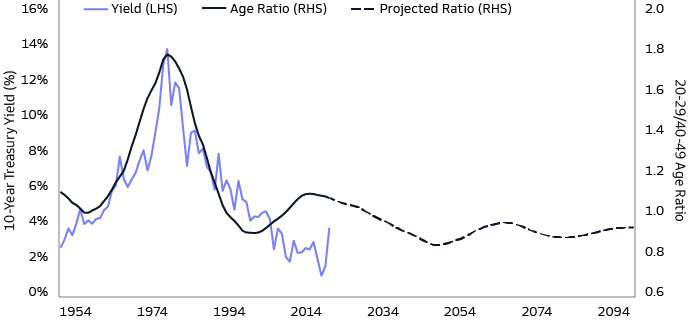

We believe the composition of the population matters too, especially that of the working age cohort, as suggested by a 2015 paper from the International Monetary Fund (IMF).9 The ratio of people aged 20-29 and 40-49 shows a statistically significant relationship with the 10-year nominal government bond yield in the US. While many other factors are at play, the regression analysis suggests a strong relationship between the two.10 And this mostly holds true when applied internationally.11 People tend to borrow when young, invest for retirement and their children’s college when middle-aged, and live off their investments once they are retired. All else equal, prevailing long-term nominal government bond yields in advanced economies will therefore bear some relation to the balance between the young, who are the spenders, and the middle-aged, who are the savers. When the ratio between those two cohorts is high, there will be excess demand for consumption by the younger population. This tends to reduce the demand for bonds, pushing yields higher and encouraging saving by the middle-aged cohort. By contrast, when the ratio is low, there will be excess demand for saving by the middle-aged population, which may push up the price for bonds, potentially prompting yields to fall.

Source: United Nations and Goldman Sachs Asset Management. As of June 12, 2023. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Past performance does not predict future returns and does not guarantee future results, which may vary. For illustrative purposes only.

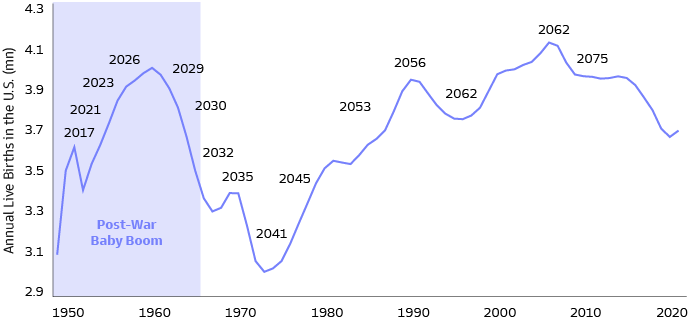

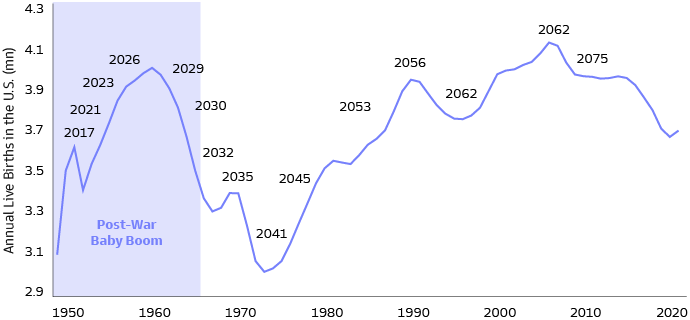

This ratio changes over time, as different age cohorts work their way through the population structure. In the US, the ratio has recently grown as baby boomers—people born between 1946 and 1964—are starting to retire, pointing to potentially higher long-term yields over the next 10-15 years. Beyond that, the ratio of people aged 20-29 and 40-49 in the US could put some downward pressure on the 10-year Treasury yield by 2050, but rates could rise again in the second half of the century as millennials—born between 1981 and 1996— retire.

Source: United Nations and Goldman Sachs Asset Management. As of June 14, 2023. The year they turn 65 marked on top of the line. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Past performance does not predict future returns and does not guarantee future results, which may vary. For illustrative purposes only.

For equities, there tends to be an inverse relationship between the equity risk premium (ERP) and the prevailing level of interest rates, because the ERP is defined as the difference between the expected return on stocks and the estimated expected return on risk-free bonds. Therefore, we expect the ERP to follow a similar, albeit opposite, pattern to bond yields. In other words, in the US at least, the ERP is likely to fall in the next 10-15 years as yields rise and fixed income challenges equities as an attractive investment alternative. Beyond that time horizon, the ERP may increase until 2050 as yields fall, and decline again in the second half of the century as yields trend upward. This will likely vary from country to country.

A dwindling workforce could also potentially weigh on equity valuations. Simply put, companies require economic growth to prosper, and an increase in the working-age population contributes directly to that growth. If the working-age cohort is shrinking, stagnation may set in, and firms will have a harder time growing their revenues and earnings.

But demographic change may also present potentially attractive investment opportunities. For example, companies that provide healthcare services to the elderly or those that can adapt to these new consumption trends are likely to benefit. Also, the expected reduction in labor supply may accelerate the adoption of new technologies such as AI. Firms that enable these technologies and help other companies adopt them effectively may profit from this. We see opportunities in venture capital or growth equity which can capture this trend early.

Overall, portfolios may have to be built differently in the future. Over the next 10-15 years, higher yields and lower equity risk premia across developed markets might prevail, but beyond that, much is likely to depend on the evolution of the relationship between the young and the middle-aged at the time, which in turn may potentially hinge on economic policies and migration trends. For example, raising the retirement age could change the balance between spenders and savers, while raising inflation targets to acknowledge the potential inflationary impact of deteriorating demographics may have profound implications for portfolio construction. (We explored a scenario of higher inflation regime in Is 3% the New 2%?).

Countries with relatively similar magnitudes of aging may also have different asset price dynamics. Furthermore, companies that offer products, services and technologies that are materially and beneficially exposed to the dynamics of consumer spending behavior could present attractive long-term investments. Finally, many emerging economies have more positive demographic profiles than advanced economies, and therefore may offer attractive diversification opportunities for investors exposed to aging population dynamics. Therefore, we believe portfolios should be constructed with these trends in mind.

Committed to providing you with the insights you need to build your practice.

1 A Lewis Turning Point is a situation in economic development where a surplus of low-cost labor is fully absorbed, leaving a shortage of workers. This may in turn push up wages, consumption and inflation rates.

2 United Nations. As of April 24, 2023.

3 Federal Reserve Bank of San Francisco, “Labor Force Participation and the Prospects for U.S. Growth.” As of November 2, 2007.

4 Goldman Sachs Global Investment Research, “The Potentially Large Effects of Artificial Intelligence on Economic Growth.” As of March 23, 2023.

5 UK Office for Budget Responsibility, “Fiscal risks and sustainability – CP 702.” As of July 2022.

6 Financial Times, “France hit by more protests against pension reform.” As of April 6 2023.

7 Gevorgyan, K. (2019). Do demographic changes affect house prices? Journal of Demographic Economics, 85(4), 305-320.

8 Federal Reserve Bank of San Francisco, “Demographics and Real Interest Rates: Inspecting the Mechanism.” As of March 2016

9 International Monetary Fund, “Demographics and The Behavior of Interest Rates*.” As of June 2015.

10 Goldman Sachs Asset Management. As of June 2023.

11 International Monetary Fund, “Demographics and The Behavior of Interest Rates*.” As of June 2015.

Glossary

Gross Domestic Product (GDP) is the value of finished goods and services produced within a country's borders over one year.

Positive demographic profiles refer to countries with a growing native population, high fertility rates, an expanding labor force and a low old-age dependency ratio.

Stagnation refers to a prolonged period of slow or no economic growth, often accompanied by bouts of high unemployment.

Risk Considerations

All investing involves risk, including loss of principal.

Equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Different investment styles (e.g., “growth” and “value”) tend to shift in and out of favor, and, at times, the strategy may underperform other strategies that invest in similar asset classes. The market capitalization of a company may also involve greater risks (e.g. "small" or "mid" cap companies) than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements, in addition to lower liquidity.

Investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity, interest rate, prepayment and extension risk. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. The value of securities with variable and floating interest rates are generally less sensitive to interest rate changes than securities with fixed interest rates. Variable and floating rate securities may decline in value if interest rates do not move as expected. Conversely, variable and floating rate securities will not generally rise in value if market interest rates decline. Credit risk is the risk that an issuer will default on payments of interest and principal. Credit risk is higher when investing in high yield bonds, also known as junk bonds. Prepayment risk is the risk that the issuer of a security may pay off principal more quickly than originally anticipated. Extension risk is the risk that the issuer of a security may pay off principal more slowly than originally anticipated. All fixed income investments may be worth less than their original cost upon redemption or maturity. High-yield, lower-rated securities involve greater price volatility and present greater credit risks than higher-rated fixed income securities

Emerging markets investments may be less liquid and are subject to greater risk than developed market investments as a result of, but not limited to, the following: inadequate regulations, volatile securities markets, adverse exchange rates, and social, political, military, regulatory, economic or environmental developments, or natural disasters.

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

An investment in Real Estate Investment Trusts ("REITs") involves certain unique risks in addition to those risks associated with investing in the real estate industry in general. REITs whose underlying properties are focused in a particular industry or geographic region are also subject to risks affecting such industries and regions. The securities of REITs involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements because of interest rate changes, economic conditions, tax code adjustments, and other factors.

The above are not an exhaustive list of potential risks. There may be additional risks that are not currently foreseen or considered.

General Disclosures

Diversification does not protect an investor from market risk and does not ensure a profit.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

The views expressed herein are as of the date of the publication and subject to change in the future. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. Nothing in this document should be construed to constitute allocation advice or recommendations.

The website links provided are for your convenience only and are not an endorsement or recommendation by Goldman Sachs Asset Management of any of these websites or the products or services offered. Goldman Sachs Asset Management is not responsible for the accuracy and validity of the content of these websites.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, a licensed entity regulated by the Securities and Futures Commission of Hong Kong (SFC). This material has not been reviewed by the SFC. © 2023 Goldman Sachs. All rights reserved.

Singapore: Investment involves risk. Prospective investors should seek independent advice. This advertisement or publication material has not been reviewed by the Monetary Authority of Singapore. This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

· Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

· Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

· Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

· Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws.

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

New Zealand: This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar: This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser. The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

East Timor: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds), or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed under any laws or regulations of Timor-Leste. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person or institution without the prior consent of Goldman Sachs Asset Management.

Vietnam: Please Note: The attached information has been provided at your request for informational purposes only. The attached materials are not, and any authors who contribute to these materials are not, providing advice to any person. The attached materials are not and should not be construed as an offering of any securities or any services to any person. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer under the laws of Vietnam. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Cambodia: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds) or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer or investment advisor under The Securities and Exchange Commission of Cambodia. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Date of First Use: August 7, 2023 326288-OTU-1838998