April 20, 2023 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsApril 20, 2023 | 9 Minute Read

Valentijn van NieuwenhuijzenGlobal Head of Sustainability for Public Investing Valentijn van Nieuwenhuijzen |

The climate transition and the drive to create a more inclusive society are transforming the global economy. If the past year has taught investors anything, it’s that the process is going to be unpredictable.

The decade prior to 2022 saw a rapid expansion of the sustainable investing theme, propelled by swelling investor demand and the multiplying commitments of governments and companies to address the challenges of climate change and social inequality. Last year’s market volatility delivered a reality check, as the spiraling cost of living and energy supply concerns exacerbated by the war in Ukraine shifted attention to immediate economic issues.

Yet while 2022 may have brought the honeymoon for sustainable investing to an end, it did not derail the underlying economic restructuring. In fact, the sustainability transition could be accelerated by factors such as last year's energy shock, which underscored the need for securing natural gas from alternative suppliers, while increasing ambition for renewables. This also led to some countries setting net zero emissions targets for their energy systems. For investors, understanding this process will be essential to managing their assets effectively in the years ahead.

With climate change continuing to affect economies, businesses and communities around the world, the transition to a low-carbon economy is more important than ever. This decarbonization push will require transformative changes throughout the economy – especially in high-emitting sectors such as agriculture, construction, heavy industry and transport – driven by a united effort that includes supportive public policy and rapid advances in technology.

The transformation of the economy is not a distant goal; it’s happening now. We are in the midst of one of the biggest secular macroeconomic shifts in memory, propelled by a strengthening global consensus on the need to address climate change and social inequality that has been mapped out in landmark documents such as the United Nations’ Sustainable Development Goals.1

Reshaping the economy will require investment in companies and their value chains across all sectors, not just those with obvious links to sustainability themes such as renewable energy. After all, the complexity and scale of this systemic change require holistic, scalable solutions. Decarbonizing transport, buildings and industry, for example, will rely on a complex ecosystem of low-carbon technologies including energy storage and carbon capture along with access to clean power.

To make all this happen, mobilizing capital at scale will be critical – and vast amounts of investment are needed. Goldman Sachs Global Investment Research estimates that the price tag for decarbonizing 75% of the global economy now stands at $3.1 trillion per year.2 Key related goals will also come at a cost, and current investment meets only a fraction of annual needs. The shortfall in financing to protect biodiversity, for example, stands at $700 billion per year, according to a key UN agreement signed in December 2022.3

Sustainable investing has expanded rapidly over the past two decades, driven by the increasing commitments of governments, companies and asset managers to support the transition. This growth can be seen in the rising volume of assets managed by signatories to the Principles for Responsible Investment (PRI), a financial industry initiative that helps firms integrate environmental, social and governance (ESG) criteria into their investment and ownership decisions. The roughly 4,000 signatories to the PRI represented more than $120 trillion of assets at the end of 2021, up from just $10 trillion in 2007.4 Goldman Sachs Asset Management is a signatory to the PRI.

After years of favorable market conditions for sustainable investing, 2022 delivered a shock. Market volatility and the surging price of energy driven by supply and security concerns exacerbated by the conflict in Ukraine gave a lift to companies such as traditional energy producers that many sustainability-focused investors had typically omitted from their portfolios. This served as a drag on ESG strategies, as reflected in the underperformance of MSCI’s five main ESG stock indexes compared with the broader market.5 MSCI attributed the underperformance of its ESG indexes primarily to the strong performance of the energy sector and a rally in value stocks amid last year’s inflationary pressures and aggressive central bank tightening of monetary policy.6

While 2022 was challenging for sustainable investing strategies, the market turmoil did not undermine the long-term importance of ESG factors to the performance of listed companies. In a report published last December, Goldman Sachs Global Investment Research showed that stocks scoring higher for environmental and social criteria performed better than lower-scoring stocks in the first 11 months of 2022. This continued a trend stretching back more than a decade: in a study going back to the start of 2012, the lowest-ranking group of companies based on environmental and social criteria consistently underperformed the higher-ranking groups.7

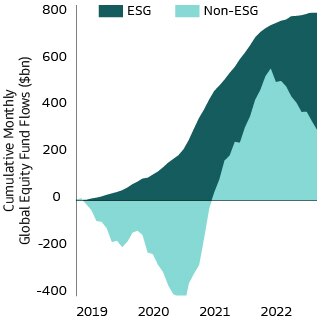

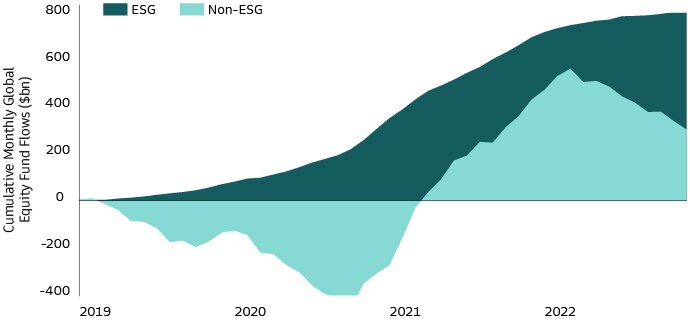

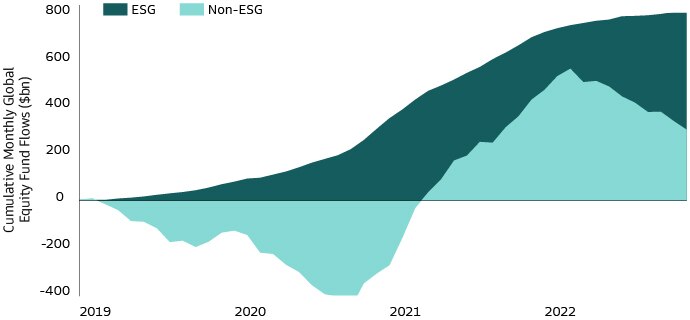

We believe that the strategic consequences of 2022 will potentially support the transformation of the global economy, opening up wider investment opportunities. The sustainability investment case remains strong, supported first of all by resilient investor demand. The flow of investor money into sustainable mutual funds shows this clearly: while these inflows last year were well below highs seen during the pandemic, they remained positive despite the market turmoil. Non-ESG funds, by contrast, suffered outflows throughout 2022.8

Source: Morningstar, Goldman Sachs Global Investment Research. As of December 2022.

Global resolve to achieve key sustainability goals also remains robust. Companies have continued to commit to reducing greenhouse gas (GHG) emissions in line with the overall goal of achieving net zero emissions by 2050. Governments around the world are also scaling up their commitments to the net zero agenda. On the critical issue of the financing needed for mitigation and adaptation efforts, leaders at the COP27 global climate conference in Egypt in November 2022 agreed to establish a loss and damage fund to support countries most vulnerable to the impact of climate change.9

The challenges of 2022, in particular the energy security issues in major European economies, will also add to the sense of urgency to accomplish global sustainability goals, and this could accelerate the energy transition by boosting efforts to develop and deploy sustainable alternatives to fossil fuels. Despite some short-term setbacks caused by the energy shock, such as increased reliance on coal in 2022,10 we believe last year’s turmoil has strengthened longer-term incentives to advance the shift to renewables and increased electrification.

A successful transition will require a swift ramping up of investment. For example, the nearly 190 countries that signed the UN’s landmark Kunming-Montreal Global Biodiversity Framework in December aim to mobilize at least $200 billion per year in biodiversity-related funding from public and private sources.11 To muster private capital on this scale, public policy must create the right incentives, especially in high-emission, hard-to-abate sectors such as industrial, transport, energy, chemicals and construction.

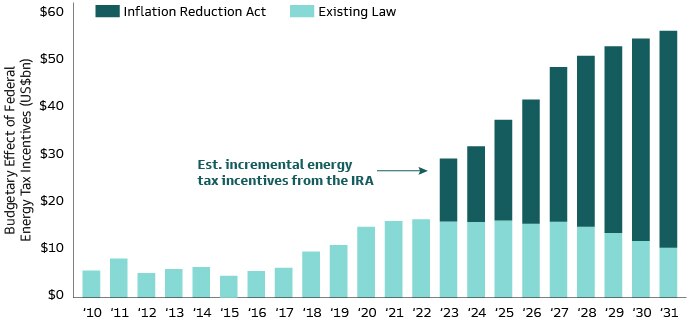

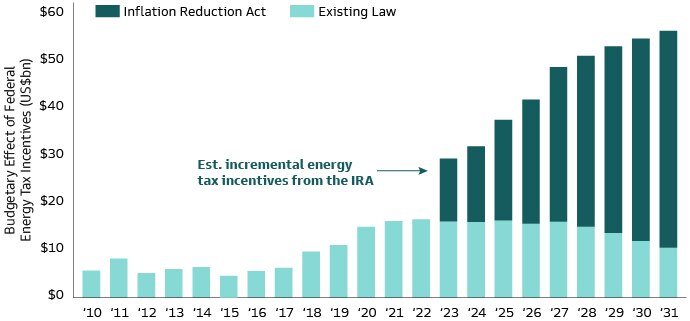

Recent evidence shows that policy makers are getting the message. In 2022, the US finalized the Inflation Reduction Act (IRA), which includes climate-related measures designed to accelerate the transition to a clean energy economy. The Act unleashes more than $390 billion in federal support for climate and energy initiatives over 10 years, with about $270 billion of that coming in the form of incremental tax incentives – a level of spending that could boost the competitiveness of the US in clean energy. It could be most transformative for battery storage, hydrogen, carbon capture and energy efficiency, according to Goldman Sachs Global Investment Research.12

Source: US Treasury, Congressional Budget Office, Goldman Sachs Global Investment Research. As of January 3, 2023. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved.

The impact of the Inflation Reduction Act will also be felt outside the US, including in the European Union, which has long been a leader in promoting the development of sustainable solutions through sweeping initiatives such as the European Green Deal, which sets out the bloc’s strategy for reaching net zero GHG emissions by 2050. In February 2023, a few months after the US Act was signed into law in Washington, EU policy makers unveiled a Green Deal Industrial Plan to increase the competitiveness of Europe’s net zero industry and speed the transition to climate neutrality. The plan foresees investment in strategic net zero sectors, including through tax benefits.13

Other countries are also deploying investment and incentives in the race to shape the future of clean energy. China has invested heavily in clean energy supply chains and currently dominates the manufacturing and trade of most clean energy technologies, according to the International Energy Agency (IEA).14 India’s government recently launched a range of initiatives to spur development of renewable energy technologies under its Production-Linked Incentive Scheme.15

We believe companies that transition successfully will be best positioned for success in the new sustainable economy. For investors, this is not an impact bet but an understanding of where the economy is going. Investments that help accelerate the transition therefore have the potential to provide attractive financial returns. The task for investors is to be the smartest at spotting opportunities amid the turbulence.

Green solution providers are essential to the development of solutions that will facilitate the transformation. The scale of innovation needed is highlighted by the IEA in a report on reaching net zero by 2050. While most of the global reductions in GHG emissions needed through 2030 can be achieved with technologies that are readily available today, in 2050 nearly half of reductions will come from technologies that are currently at the demonstration or prototype phase.16

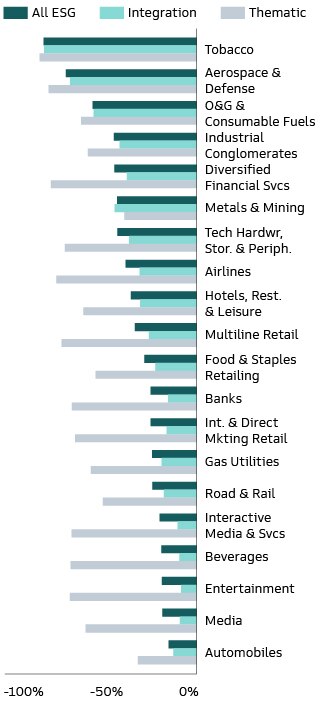

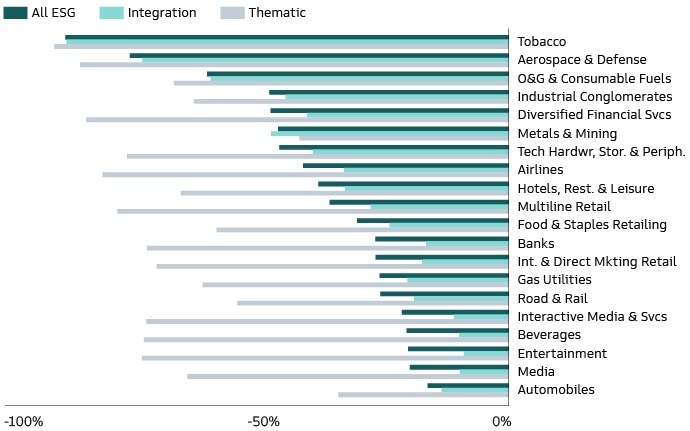

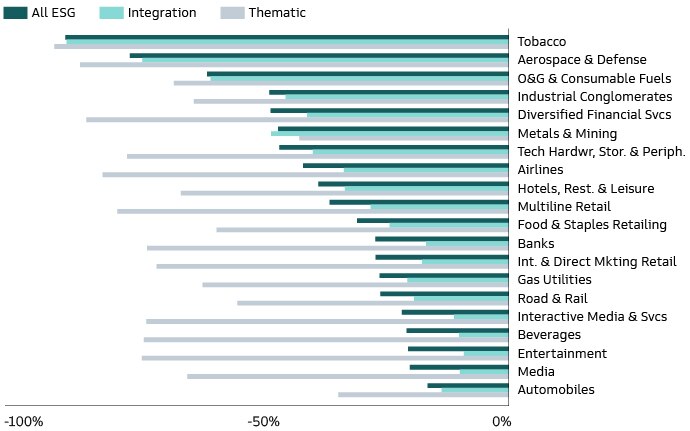

Green solutions firms cannot do it alone, however. Our real lives depend on an enormous range of products from traditional industries, and the biggest investment opportunities will likely be found in these sectors – where the challenges are the greatest. If companies such as producers of energy and building materials navigate the transition well, they can become leaders in the sustainable economy, gaining market share and enhancing their business models and cost structures. The leaders in these industries will create integrated products that take ESG considerations into account. To find them, sustainable investors will need to broaden their scope.

Many ESG investment strategies have a bias towards “pure play” sustainable business models. After all, it is a relatively straightforward task to create a carbon-light portfolio by investing in low-emission companies, even though some of these may have only a marginal relevance to the energy transition. This tendency to hold fewer stocks from high-emission sectors creates an opportunity for investment strategies focused on the transformation of heavy industry and high-GHG sectors where the potential for real-world impact is the greatest.

Source: Morningstar, Refinitiv Eikon, Goldman Sachs Asset Management. As of January 3, 2023

In fact, we are seeing a growing number of such transition and “improver” funds that provide capital and financial incentives for high-carbon industry leaders to step up their decarbonization efforts.17 Since our society and the global economy will still rely on these industries in a sustainable future, a system-wide sustainable transformation needs capital markets and global investors to provide support to both pure play green enablers as well as transition leaders in high-carbon industries.

The global economy is changing fast, propelled by a long-term regime shift around sustainability. This creates both new risks and new opportunities for investors, and embedding a forward-thinking, transformative approach in investment decisions and financial products will be crucial for future investment returns and prudent risk management. Such an approach has the potential to generate robust returns and make a positive contribution to the transformation of the economy. By guiding investors and the companies they invest in on their sustainability goals, this approach can also deliver greater impact for society.

Committed to providing you with the insights you need to build your practice.

1The SDGs are a 15-year global action plan for protecting the environment, ending poverty and reducing inequality.

2“Carbonomics: The Economics of Net Zero,” Goldman Sachs Global Investment Research. As of November 29, 2022.

3“COP15: Nations Adopt Four Goals, 23 Targets for 2030 in Landmark UN Biodiversity Agreement,” Convention on Biological Diversity. As of December 19, 2022.

4“About the PRI,” PRI Website. As of February 27, 2023.

5“The Performance of ESG Indexes: Year in Review,” MSCI. As of January 31, 2023. The broader market is represented in this comparison by MSCI’s flagship global index, the MSCI ACWI. MSCI explains in the report that its ESG indexes historically had lower relative allocations to the energy sector and higher allocations to information technology. These allocations contributed to the outperformance of ESG indexes in the decade before 2022, but this did not hold true last year.

6Growth investment strategies focus on companies’ future earnings and potential to outperform the market over time, while value strategies seek out companies currently trading below their fundamental value. Growth investing is often tightly linked with ESG and sustainability performance.

7“The PM’s Guide to the ESG Revolution IV: The Way Forward,” GS Sustain. As of December 15, 2022.

8“Global Sustainable Fund Flows: 4Q 2022 in Review,” Morningstar. As of January 26, 2023.

9”COP27 ends with announcement of historic loss and damage fund,” UN Environment Programme press release. As of November 22, 2022.

10“The world’s coal consumption is set to reach a new high in 2022 as the energy crisis shakes markets,” International Energy Agency. As of December 16, 2022.

11“Press Release: Nations Adopt Four Goals, 23 Targets for 2030 In Landmark UN Biodiversity Agreement,” United Nations. As of December 19, 2022.

12“10 Predictions for Sustainable Investing in 2023,” GS Sustain. As of Jan. 3, 2023.

13“The Green Deal Industrial Plan: Putting Europe’s Net-Zero Industry in the Lead,” European Commission press release. As of February 1, 2023.

14“Energy Technology Perspectives 2023,” IEA. As of January 12, 2023.

15“Government incentivizes local development and manufacturing of renewable energy technologies,” Ministry of New and Renewable Energy press release. As of March 22, 2022.

16“Net Zero by 2050, a Roadmap for the Global Energy Sector,” IEA. As of May 2021.

17“10 Predictions for Sustainable Investing in 2023,” GS Sustain. As of Jan. 3, 2023.

Disclosures

Glossary

Greenhouse gases absorb infrared radiation and trap heat in the atmosphere. This so-called greenhouse effect is associated with global warming. Examples include carbon dioxide, methane and nitrous oxide.

Green solutions are products, strategies and technologies that contribute to reducing greenhouse gas emissions and mitigating environmental impact. Examples include renewable energy technologies, energy-efficient buildings and sustainable agriculture practices.

Green enablers are companies that produce critical components of a more energy-efficient global economy, such as semiconductors and energy-transmission solutions.

MSCI ACWI is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. It comprises of stocks from 23 developed countries and 24 emerging markets.

Risk Considerations

Environmental, Social and Governance (“ESG”) strategies may take risks or eliminate exposures found in other strategies or broad market benchmarks that may cause performance to diverge from the performance of these other strategies or market benchmarks. ESG strategies will be subject to the risks associated with their underlying investments’ asset classes. Further, the demand within certain markets or sectors that an ESG strategy targets may not develop as forecasted or may develop more slowly than anticipated.

General Disclosures

The views expressed herein are as April 12, 2023 and subject to change in the future. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

This material represents the views of Goldman Sachs Asset Management. It is not financial research or a product of Goldman Sachs Global Investment Research (GIR). It was not a product nor financial research of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed herein may vary significantly from those expressed by GIR or any other groups at Goldman Sachs. Investors are urged to consult with their financial advisers before buying or selling any securities. The information contained herein should not be relied upon in making an investment decision or be construed as investment advice. Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security, they should not be construed as investment advice.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Examples are for illustrative purposes only and are not actual results. If any assumptions used do not prove to be true, results may vary substantially.

There is no guarantee that objectives will be met.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. Nothing in this document should be construed to constitute allocation advice or recommendations.

Investors cannot invest directly in indices.

In an effort to distinguish funds by what they own, as well as by their prospectus objectives and styles, Morningstar developed the Morningstar Categories. While the prospectus objective identifies a fund's investment goals based on the wording in the fund prospectus, the Morningstar Category identifies funds based on their actual investment styles as measured by their underlying portfolio holdings (portfolio and other statistics over the past three years).

©2023 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is not guarantee of future results.

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence (“S&P”) and is licensed for use by Goldman Sachs. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA):This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

New Zealand: This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Malaysia: This material is issued in or from Malaysia by Goldman Sachs (Malaysia) Sdn Bhd (880767W)

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited.

Singapore: This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser.

The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

Date of First Use: April 20, 2023. 309738-OTU-1762848