August 7, 2023 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsAugust 7, 2023 | 10 Minute Read

Amy JupeCo-Head of XIG Private Equity Primaries and Head of XIG Private Credit Amy Jupe |

James GelferPortfolio Solutions for Alternatives Capital Markets and Strategy James Gelfer |

For more than a decade, both the number of funds and amount of capital raised by private market General Partners (GPs) had been on an upward trajectory. For GPs, attracting and retaining talent was relatively easy over this period, with industry tailwinds attracting high-caliber professionals who could be incentivized with rising compensation packages and the promise of expanding opportunities. These trends accelerated during the post-pandemic boom, which saw unprecedented levels of fundraising and deal activity. As in many other industries, some firms altered their trajectory for a new world in which those levels of activity and growth would be the norm going forward, ramping up hiring, capital deployment, and fundraising ambitions. Just a few quarters removed from those halcyon times, private market activity has slowed significantly, and structurally higher rates and macroeconomic uncertainty are expected to create a more challenging operating environment in the years ahead.

With Limited Partners (LPs) facing the combined impact of the numerator and denominator effects, fundraising timelines have been extended and the challenges are expected to persist in the coming quarters. Many funds are struggling to meet their goals and are facing the prospect of a fund size that is smaller or unchanged from the prior vintage. Smaller fund sizes could translate to less potential carry to distribute amongst the investment teams, as well as present structural issues for GPs who have grown accustomed to a certain level of management fees and/or require higher levels of management fees to support organizations that were expanded in the anticipation of growth. The need for GPs to dedicate more time and effort to raising new funds could potentially become a distraction for investment team members. This not only introduces risk for strategy execution, but also could lead to morale and motivation issues for team members who may be asked to spend a disproportionate amount of time raising capital rather than deploying it.

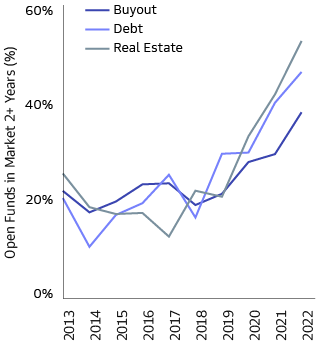

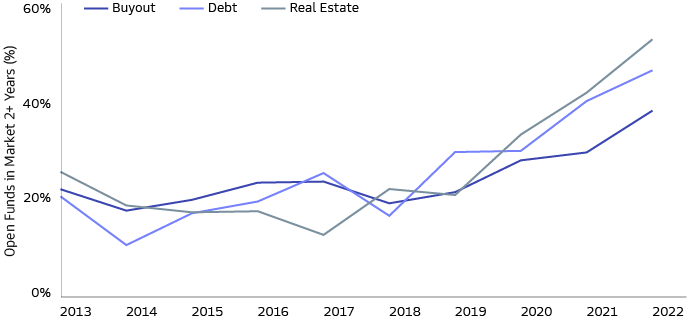

Source: PitchBook. As of December 31, 2022.

In addition to the broad fundraising slowdown, following a rapid proliferation of sub-strategies by some GPs, many appear to have changed tack and are redoubling efforts on existing strategies rather than branching into new areas. As there are potentially fewer opportunities for talent to rise through the ranks and assume new responsibilities, the risk of organizational instability and team turnover at GPs may also rise—particularly amongst mid-career professionals who may no longer anticipate the same trajectory with their current firm. Headlines suggest that some GPs have started reducing head count, and there are also expectations for consolidation within the industry as even well-performing firms may find it difficult to find a viable path forward (see sidebar). We believe these challenges for GPs are important considerations for LPs in both assessing current fund positions and evaluating new opportunities.

The private equity industry has seen relatively steady growth for several decades, across both the number of firms and total assets under management. A handful of GPs have achieved scale and more direct access to capital markets via public listings. With this access to financing, some have turned to acquisitions to expand both their fund offerings and talent pools. The 50 largest GPs completed 116 strategic deals in the decade through 2022, but the pace is accelerating with nearly 40% of those transactions coming in the last two years. Many of these merger and acquisition deals between GPs involve established firms, where the track record and longevity of the strategy being acquired are major assets; other deals for less-established GPs can be more akin to so-called acqui-hires of startup engineering teams, where the main asset being acquired is the people. As a result, the largest GPs now tend to have diversified strategy offerings that allow them to lean into and capture different opportunities as the market and environment evolves. Other GPs looking to follow suit and build multi-strategy platforms will likely need to raise capital, either from a public listing or GP stake sale.

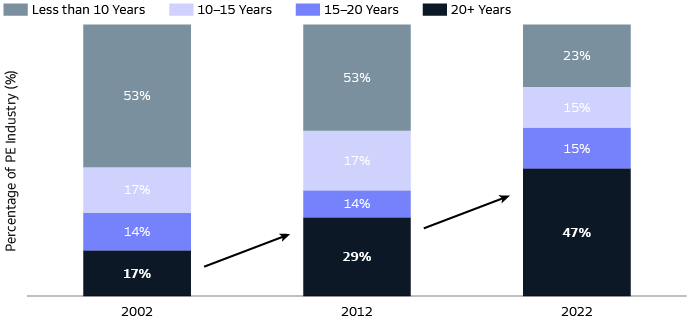

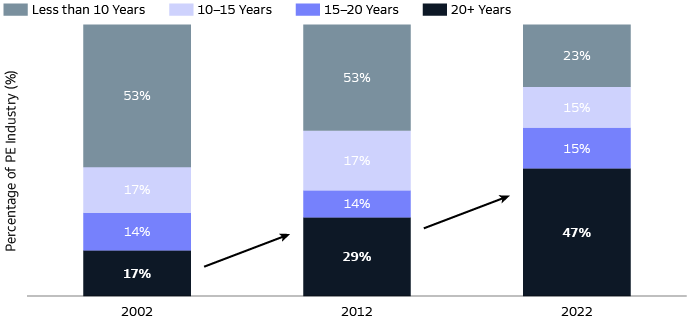

At the same time that large GPs are becoming more acquisitive, the proliferation of GPs and funds in recent years also means that the number of potential targets has never been higher. In addition to cyclical factors that may lead to organizational instability, many established GPs are at a critical juncture; nearly half of GP firms that are 20-35 years old have yet to initiate a succession plan. At the other end of the spectrum, the proliferation of new firms over the last 15 years means that many of the firms operating today have yet to experience a full market cycle. Many of these firms aggressively expanded amidst the broad tailwinds of the last decade, and now that the market has turned and fundraising has grown more difficult, the need to recalibrate could lead some to pursue strategic alternatives.

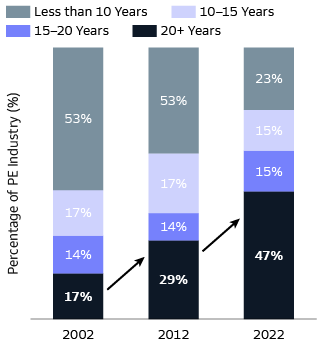

Source: Preqin. As of December 2022. Includes all private equity buyout firms with AUM greater than $1 billion.

Capital is the lifeblood of business, and this is particularly true for investment management firms. A strong, stable capital base is essential for private market managers not only to deploy capital effectively and efficiently through market cycles, but also to properly compensate talent and provide a compelling trajectory for upward mobility. As with many businesses, an investment firm tends to be best positioned when the client base (i.e., LPs) is diverse and unconcentrated. Some simple ways to quantify a GP’s LP base include assessing the total number of LPs at both the firm and fund level, as well as the relative commitments of the largest LPs and the percentage of re-ups. The type of LP is pertinent too; similar types of LPs may behave similarly in terms of their commitment decisions.

We believe strategy diversification should also be considered, with pros and cons for different models. Large, diversified asset managers with multiple fund strategies may be able to allocate resources, especially non-investment resources, across a platform depending on where they are most needed, which would be expected to change over the course of a cycle. In addition, manager-level revenue streams for diversified GPs are often more consistent, as the lumpiness of performance and fundraising associated with a particular strategy is reduced when aggregating multiple strategies. As a result, the firm can provide a smoother and more predictable compensation experience for many investment professionals. At the other end of the spectrum, single-strategy GPs should theoretically be able to run leaner teams and tie compensation more directly to performance, with the tradeoff being less opportunity to mitigate strategy-specific headwinds. Additionally, single-strategy firms inherently have fewer avenues for junior talent to be promoted or assume more responsibility.

In today’s environment, the most challenged GPs may be those that are in the midst of an expansionary phase, potentially with fund strategies in their first few vintages; these GPs may have to contemplate whether certain strategies are viable going forward, and how their recent growth plans may need to be recalibrated for new realities. To understand the GP’s priorities and the potential for distraction caused by ancillary strategies, investors can analyze the number of strategies that the firm has managed over time, including the average age and asset under management (AUM) change across strategies, as well as develop an understanding of which investment team members are dedicated to a particular strategy or will be required to work across multiple strategies. This analysis should be supplemented with conversations with senior leadership and considerations for how economics are shared between the flagship team and those running other strategies.

Team turnover is a straightforward and common way to address stability, but some research has shown a positive correlation between turnover and performance. This potentially counterintuitive finding can be attributed to a combination of short-term performance improvements when “bad performers” are asked to leave along with long-term performance benefits from turnover that enables a firm to “adapt and replenish skills.”1 Indeed, the strategies and skillsets required to succeed are likely to differ based on the prevailing macro environment and particular segment of the business cycle. To that end, rather than simply equating a lack of turnover with stability, we believe investors should be looking to assess how a GP is adapting—whether through team structuring, upskilling, additions, or (in some cases) reductions—to maintain an edge and deliver alpha in an ever-evolving market. Furthermore, LPs should consider if there is enough accountability and whether everyone is being held to a high enough standard, including more tenured professionals who over time may play a less active role in the organization.

Investment firms necessarily increase in complexity as they grow, but organizations need to strive to maintain clear lines of communication and simplicity in their structure. Stability starts at the top with strong leadership. Investment acumen is essential, and while leaders need to have confidence and trust their skills and process, they also run the risk of hubris and consolidating decision-making. Successful GPs tend to limit the number of direct reports for both senior leaders and mid-level managers; these flatter hierarchies may lead to enhanced collaboration and facilitate opportunities for professional development and upward mobility by increasing exposure for junior team members. The career progression for specific roles should be clear, and a firm-level succession plan should be in place to ensure continuity (see sidebar).

With turnover alone proving insufficient to evaluate the team and structure, due diligence should include an evaluation of the investment committee composition and process. Incorporating diverse viewpoints can create a more resilient organization and lead to greater buy-in from team members. The ownership structure of the firm is important in assessing not only how current economics are shared, but also to understand how the structure may impact collaboration and long-term planning.

The view that “people are our greatest asset” has become cliché in many fields, but in private equity, we believe people truly are the foundation. Retaining and hiring talent are cited as primary objectives for GPs of all sizes.2 As private markets become a more integral part of capital markets and investment portfolios, the competition for experienced talent is intensifying. The ability to properly motivate talent may become more challenging in the current environment, as a decrease in exits is likely to impact carry payouts in the near term while the potential for weaker fund-level performance could reduce compensation pools over the long term.

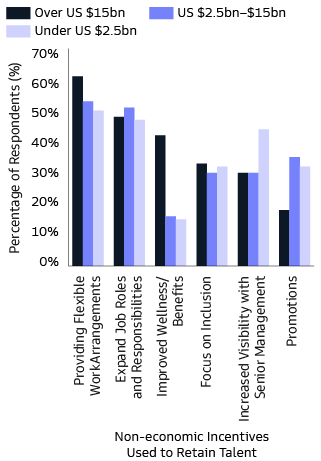

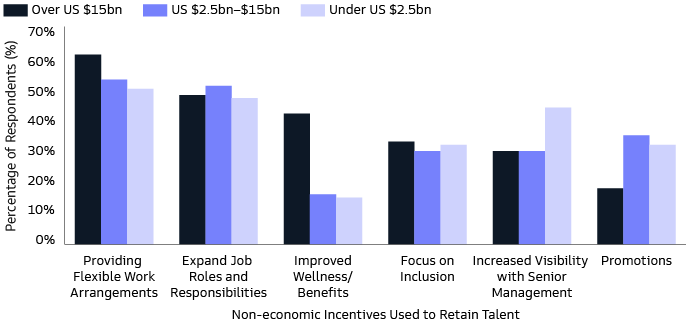

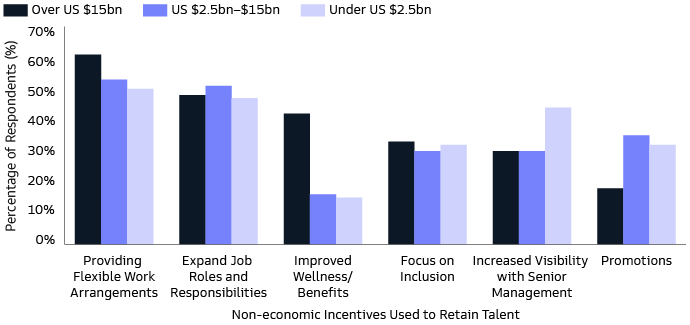

Compensation is unquestionably a primary motivator for many workers across a broad range of fields—and private equity is no exception. Investors can assess the overall GP commitment to the fund, including how it is financed and contributed to, as well as the allocation of carry, to understand the complex economic incentives. But employees are increasingly valuing other factors in the workplace. Research has shown that the level of talent at an investment firm is best explained when evaluating both economic incentives and non-economic incentives,3 including opportunity to operate autonomously, achieve mastery, and work towards a purpose. Increasingly, flexible working arrangements (i.e., remote work) are a factor too. In addition to assessing formal policies, diligence should include time with professionals from all levels of the GP to get a qualitative view of morale.

Source: EY. The 2023 EY Global Private Equity Survey. As of January 18, 2023.

Talented professionals will seek out challenging, rewarding opportunities—as such, GPs need to have a plan in place to ensure they have ways of motivating and rewarding top talent. In addition to the risk of losing talent to competitors, GPs must also consider the potential for employees to launch their own fund if not presented with opportunities. While raising a first-time fund is notoriously difficult, especially in today’s more challenging fundraising environment, those with the most success often come from established GPs where they have been able to demonstrate an initial track record of success.4

As the market environment has turned, many GPs are grappling with new realities in fundraising and managing their own firm. These challenges also represent an important variable for LPs to consider in both evaluating current holdings and considering new fund commitments. Organizational stability is always an important factor for private market investing—where a single fund commitment typically lasts for more than a decade—but it is perhaps even more paramount today as market tremors create the potential for cracks in firms’ foundations.

Committed to providing you with the insights you need to build your practice.

1Cornelli, Simintzi, and Vig, “Team Stability and Performance: Evidence from Private Equity,” May 2019.

2EY, “Three ways CFOs are adapting to emerging private equity trends,” Jan 18, 2023

3Goldman Sachs Asset Management as of 2015 and Ouimet, Paige and Tate, Geoffrey A., Firms with Benefits? Nonwage Compensation and Implications for Firms and Labor Markets (July 5, 2023). Available at SSRN: https://ssrn.com/abstract=4112463 or http://dx.doi.org/10.2139/ssrn.4112463

4Private Equity International. “LPs pull back from first-time funds” As of December 1, 2022.

Glossary

Acqui-hires refers to buying a company primarily for the skills of the employees rather than the products or services offered.

Risk Considerations

All investing involves risk, including loss of principal.

Alternative investments are suitable only for sophisticated investors for whom such investments do not constitute a complete investment program and who fully understand and are willing to assume the risks involved in Alternative Investments. Alternative Investments by their nature, involve a substantial degree of risk, including the risk of total loss of an investor’s capital.

Private equity investments are speculative, highly illiquid, involve a high degree of risk, have high fees and expenses that could reduce returns, and subject to the possibility of partial or total loss of fund capital; they are, therefore, intended for experienced and sophisticated long-term investors who can accept such risks.

Alternative Investments often engage in leverage and other investment practices that are extremely speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested. There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers.

Investors should also consider some of the potential risks of alternative investments:

Alternative Investments - Hedge funds and other private investment funds (collectively, “Alternative Investments”) are subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains and an individual’s net returns may differ significantly from actual returns. Such fees may offset all or a significant portion of such Alternative Investment’s trading profits. Alternative Investments are not required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of such Alternative Investments.

The above are not an exhaustive list of potential risks. There may be additional risks that are not currently foreseen or considered.

Conflicts of Interest

There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. These activities and interests include potential multiple advisory, transactional and other interests in securities and instruments that may be purchased or sold by the Alternative Investment. These are considerations of which investors should be aware and additional information relating to these conflicts is set forth in the offering materials for the Alternative Investment.

General Disclosures

Diversification does not protect an investor from market risk and does not ensure a profit.

There is no guarantee that objectives will be met.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

THESE MATERIALS ARE PROVIDED SOLELY ON THE BASIS THAT THEY WILL NOT CONSTITUTE INVESTMENT ADVICE AND WILL NOT FORM A PRIMARY BASIS FOR ANY PERSON’S OR PLAN’S INVESTMENT DECISIONS, AND GOLDMAN SACHS IS NOT A FIDUCIARY WITH RESPECT TO ANY PERSON OR PLAN BY REASON OF PROVIDING THE MATERIAL OR CONTENT HEREIN. PLAN FIDUCIARIES SHOULD CONSIDER THEIR OWN CIRCUMSTANCES IN ASSESSING ANY POTENTIAL INVESTMENT COURSE OF ACTION.

The views expressed herein are as of the date of the publication and subject to change in the future. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. Nothing in this document should be construed to constitute allocation advice or recommendations.

The website links provided are for your convenience only and are not an endorsement or recommendation by Goldman Sachs As-set Management of any of these websites or the products or services offered. Goldman Sachs Asset Management is not responsible for the accuracy and validity of the content of these websites.

The opinions expressed in this white paper are those of the authors, and not necessarily of Goldman Sachs. Any investments or returns discussed in this paper do not represent any Goldman Sachs product. This white paper makes no implied or express recommendations concerning how a client’s account should be managed. This white paper is not intended to be used as a general guide to investing or as a source of any specific investment recommendations.

Examples are for illustrative purposes only and are not actual results. If any assumptions used do not prove to be true, results may vary substantially.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, a licensed entity regulated by the Securities and Futures Commission of Hong Kong (SFC). This material has not been reviewed by the SFC. © 2023 Goldman Sachs. All rights reserved.

Singapore: Investment involves risk. Prospective investors should seek independent advice. This advertisement or publication material has not been reviewed by the Monetary Authority of Singapore. This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

New Zealand: This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser. The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

East Timor: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds), or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed under any laws or regulations of Timor-Leste. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person or institution without the prior consent of Goldman Sachs Asset Management.

Vietnam: Please Note: The attached information has been provided at your request for informational purposes only. The attached materials are not, and any authors who contribute to these materials are not, providing advice to any person. The attached materials are not and should not be construed as an offering of any securities or any services to any person. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer under the laws of Vietnam. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Cambodia: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds) or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer or investment advisor under The Securities and Exchange Commission of Cambodia. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Date of First Use: August 7, 2023 326745-OTU-1837975