September 25, 2023 |

GSAM Featured Insights

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact Us

Suzanne GauronHead of Private Equity Strategies, Alternatives Capital Markets & Strategy Suzanne Gauron |

Harold HopeGlobal Head of Secondaries, External Investing Group Harold Hope |

Gabriel MollerbergSecondaries Investment Team, External Investing Group Gabriel Mollerberg |

Thom SpotoSecondaries Investment Team, External Investing Group Thom Spoto |

Investors often look to secondaries to gain private market exposure along with additional benefits, such as J-curve mitigation and diversification. Many of these attributes are most closely associated with traditional LP portfolio sales, but secondary firms have also provided other types of capital solutions to GPs and LPs over the last two decades, from team spinouts to structured notes, that provide differentiated access to private markets. Today, continuation vehicles and preferred equity structures have become more common. As activity evolves from LP portfolio sales to include more bespoke solutions, investors should be cognizant of both the skill sets needed to source, underwrite, and execute these more-complicated transactions, as well as the risk-return implications of potentially different transaction types.

The evolution of private markets has continually led to new challenges and opportunities that require unique capital solutions. As the private markets grew in the 1990s and early 2000s from a niche US market funded by wealthy individuals and a small number of institutions into a broader asset class with distinct strategies and a global presence, more investors became LPs in an increasing number of funds. Inevitably, some investors experienced disruptions to their liquidity profiles or shifts in strategy that required them to exit these holdings. The GPs managing the funds recognized that transferring one LP’s interest to another was preferable to default, leading to the beginnings of the secondary market. Funds dedicated to these LP secondary transactions were created, and over time grew to execute more complicated transactions—from multi-fund portfolios, to structured transactions, to “strip” sales designed to streamline portfolio management while retaining economic exposure.

Today, with private market holdings in excess of $10 trillion across private equity, real estate, infrastructure, and credit assets, the secondary market provides liquidity solutions to LPs looking to reshape their portfolios or adapt investment strategies to a dynamic environment.1 However, secondary managers—as sophisticated private markets investors with flexible capital, valuation expertise, and the ability to manage complexity—have also long been providing solutions to other market participants. In the mid-2000s, some secondary firms partnered with banks looking to streamline internal private equity investing teams, ultimately spinning out these teams into new private equity firms seeded by their existing portfolios in “synthetic secondaries.” In the last decade, secondary firms have been key to helping GPs find creative solutions for legacy portfolios and manage assets through periods of disruption. Indeed, many investors with mature private market portfolios now view the secondary market as a way to regularly manage portfolio allocations, in addition to solving liquidity needs.

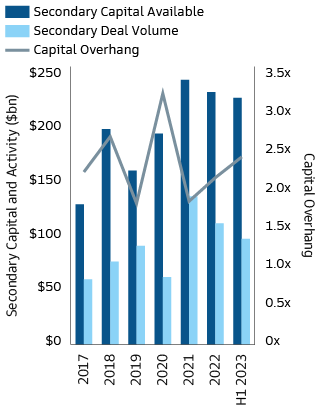

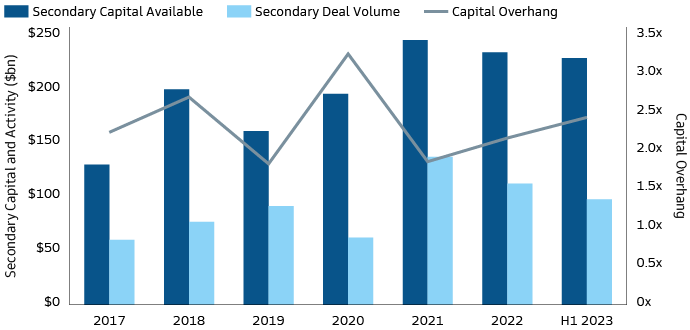

This creativity and capital flexibility, combined with attractive return generation for secondary LPs, has helped fuel strong activity in secondaries and driven AUM to more than $550 billion as of 1Q 2023. Even with this rapid growth, private market AUM (i.e., the potential supply of secondaries) has grown more than secondaries (20% CAGR vs. 17% since 2018). As a result, the secondary market remains under-capitalized relative to the broader private markets industry from which it derives its opportunity set. Furthermore, the secondaries space itself remains relatively concentrated, with the top 10 buyers accounting for at least 55% of deal activity since 2021.2 However, as the primary market has matured and the variety of secondary transactions continues to expand, secondary firms will need more than size and scale to compete; new skillsets will be required and adaptability will be necessary to structure capital solutions to meet the variety of needs of primary LPs and GPs, as well as their portfolio companies.

Source: Jefferies Global Secondary Market Review – July 2023. Capital overhang = capital available / deal volume.

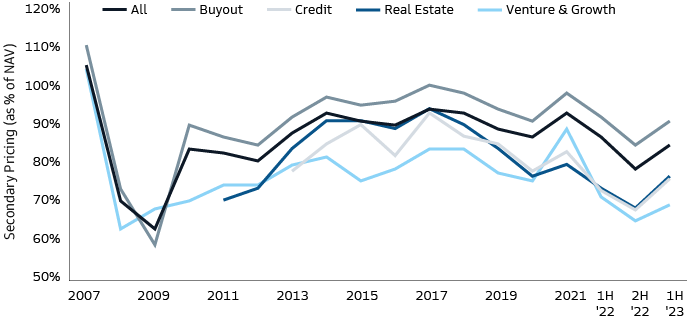

LP portfolio sales were the first secondary transactions to be executed and have historically represented the majority of the market. In the early days of the secondary market, transactions were often non-economic and the result of stress within the selling LP—liquidity constraints, strategic changes, regulatory changes, or life changes for individual investors. As a consequence, providers of liquidity were able to acquire interests at often-meaningful discounts to NAV.

Source: Greenhill Cogent, Jefferies. As of June 2023.

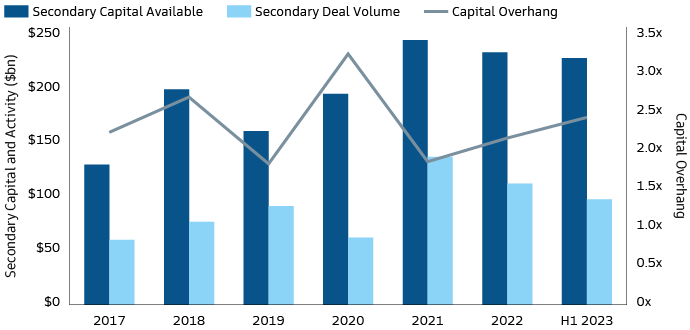

Over the last decade, however, more transactions have been executed during benign market conditions and the secondary market is no longer seen solely as an expression of distress. Today, LP portfolio sales are widely viewed as a useful portfolio management tool to adjust exposures, free up capital and team resources from older commitments that have largely run their course and crystalize gains. As more buyers and sellers have entered the market for traditional LP secondaries, pricing has generally become more stable at narrower discounts to NAV. Even in 2020, when secondary pricing and transaction volume dropped sharply in the first half of the year during the initial throes of the COVID-19 pandemic, the market rebounded to pre-pandemic levels by 1H 2021.

Bid-ask spreads widened again in 2022, as dislocations in public markets and a slowdown in transaction activity made it more difficult for buyers and sellers to agree on pricing. But while transaction volume slowed in 2022, it was still one of the strongest years on record for executed transactions, and pricing rebounded in 1H 2023—illustrating the increased depth and resiliency of the market. One factor contributing to the resilience of the market is sellers’ increasing willingness to allow buyers to choose certain assets for a broader portfolio sale, which can help to achieve actionable pricing.

While the traditional secondary market is becoming more liquid, most transactions still occur at a discount to NAV. Younger funds, where assets have more time to appreciate, typically price closer to NAV, while older vintages tend to command higher discounts; in the first half of 2023, buyout funds less than five years old priced at 91% of NAV on average, while funds with a 2012 vintage or earlier sold at an average of 73% of NAV.3 Investors have been gravitating towards younger funds, with an average age of 7.0 years in 1H 2023—the first time it has dipped below 8 years since 2014. Another factor that has supported pricing in 2023 is the use of deferrals, which allows the buyers to fund part of a transaction at a later date in return for a higher price.

Discounts in the secondary market will also reflect the complexity involved in the transaction, as well as the type, quality, and familiarity of the assets involved. As such, the most efficient pricing in the secondary market remains for traditional buyout fund stakes, which represented 72% of secondary transaction volume in 2022 and 1H 2023.4

As private markets have expanded to incorporate a broader array of assets, some secondary firms have expanded their expertise to evaluate adjacent strategies such as real estate, infrastructure, and private credit. Previously, these assets were often incorporated in portfolio sales as part of a larger transaction or excluded from sales. Today, larger LP portfolio sales and more specialized secondary funds support dedicated transactions in these spaces. Discounts for these assets tend to be wider than for traditional buyout strategies, partly due to the smaller set of buyers with the expertise to evaluate these assets, as well as their lower return profiles that require a larger discount to meet equity-focused secondary return targets. These strategies represent some of the fastest-developing areas of the secondary market, as specialist firms enter the space and established secondaries players launch dedicated vehicles.

Underpinning the opportunity in real estate, infrastructure, and private credit secondaries is the long-term growth in those asset classes, which now manage in excess of $3 trillion. Many LPs in these primary funds are also reconsidering how they define and classify different assets, leading to a widespread reassessment of asset exposure that has created an increased need for liquidity solutions. In real estate, for example, multi-tenant office buildings and shopping centers—once acquired for their core characteristics and perceived safety—are no longer viewed as “set it and forget it” investments. Conversely, industrial and rental housing assets—generally viewed as less stable historically due to shorter lease terms, fragmented ownership, and ease of over-building in expanding markets—are now exhibiting characteristics of “core” real estate, benefitting from healthy demand, outsized growth, and very liquid capital markets. As LPs seek to rebalance their risk profiles, the secondary markets can help facilitate the redeployment of capital.

While traditional LP secondary transactions remain at the core of the secondary market, other types of capital solutions have become more prominent in the past few years. Rather than solely seeking liquidity, many investors are pursuing structures that allow for extended holding periods that enable additional compounding of returns—evidenced by the rise of long-hold PE funds with durations of 20 years or more. Much of the initial activity in the space was used to support GPs’ use of buy-and-build strategies and technological transformation to create value in portfolio companies—approaches that may require more time to implement and mature than is allowed by the typical Limited Partnership structure.

The traditional Limited Partnership has a term of 10 years, generally with two one-year extensions, putting a limit on how long a GP has to execute their value creation plans. Within that 10-year period, there is typically a four- or five-year investment period, and LPs will generally expect to start seeing some liquidity by the time the fund is fully invested and the GP is fundraising again. Given these dynamics, GPs may feel a degree of pressure to sell assets four or five years after they make the investment, regardless of whether they have maximized the value. While some LPs have questioned the ability of private equity sponsors to drive excess returns over longer time periods, recent research suggests that the performance of sponsor-to-sponsor transactions, where one GP sells an investment to a second GP, is comparable to that of traditional buyout deals. This supports the argument that GPs are able to implement operational plans and acquisition strategies targeted at specific stages of development and profitability.

The secondary market can provide capital solutions that allow GPs to continue owning well-known assets in which they have high conviction and a clear plan for additional value creation, while also providing existing LPs a liquidity option and allowing for the entry of new LPs. Distinct from LP portfolio sales, these capital solutions evolved from “fund restructuring” transactions, which often involved complex situations with challenges at the underlying asset, GP, or both. Much like LP portfolio sales evolved from a market focused on distressed sellers facing liquidity challenges to a more robust (and less-stigmatized) market for reshaping portfolios, these “fund restructuring” transactions have shifted from deals designed to rework troubled situations to a market focused on high-quality assets managed by top GPs looking to extend value creation plans and realign incentives. With these new tools, GPs can look to optimize their own fund management and provide a more dynamic set of exit options for their LPs, while deepening relationships with strong companies and opening the aperture for new investors. This trend has only intensified in 2022 and 2023, as a slowdown in exits and more challenging financing conditions have compelled GPs to look for creative options.

Continuation vehicles aim to achieve a variety of objectives: liquidity for LPs looking to exit their position; the ability for current LPs to maintain exposure to the asset; and the opportunity for new investors to gain exposure to a high-quality asset managed by a GP already deeply immersed in the business, providing an extended holding period and new capital to fund further growth for the GP. These transactions typically involve the transfer of the target asset(s) from the original fund into a new vehicle, where existing LPs can elect whether they prefer to receive cash proceeds and exit the investment, or a pro-rata interest in the new vehicle. The secondary manager typically provides: an independent fair market value for the transaction; negotiates the structure and terms of the continuation vehicle to ensure continued alignment; and provides the capital that cashes out of any exiting LPs.

Continuation vehicles are bespoke and vary greatly in size and structure, with some centered on single assets while others have more diversified holdings. Continuation vehicle investors have the benefit of investing in known assets with a GP who already intimately understands its operations and has a compelling case for further value creation. The GP is able to continue executing from their existing playbook, enabling the secondary investors and LPs to bypass the early low-growth period common in new deals where a GP gains greater familiarity with the asset and refines their initial value creation plans. The GP’s familiarity with the business can also provide a degree of downside protection for the new LPs relative to a primary investment, as the value creation is largely focused on a continuation of the investment.

With the number of stakeholders involved in continuation vehicle transactions, including the liquidating LPs, the continuing LPs (in some cases), the GP, and the secondary fund/new LPs, ensuring the proper alignment of incentives is key. The GP and the secondary buyer typically negotiate new fee structures and economic protections, which may include the reinvestment of any economics a GP realizes from liquidating LPs into the continuation vehicle and a new investment from the GP. Since the specifics of each transaction tend to be unique, the economics of continuation vehicles are tailored to each deal but generally include mechanisms, such as reduced fees and revised hurdle rates.

Another important consideration for continuation vehicles is the higher level of concentration compared to traditional secondary transactions. Continuation vehicle transactions can include a portfolio of holdings, or a single asset. Single-asset transactions carry a higher degree of company-specific idiosyncratic risk, requiring the need for careful portfolio construction by the secondary manager to ensure suitable diversification. Consequentially, continuation vehicle diligence requires a deep understanding and expertise more akin to traditional buyout investing.

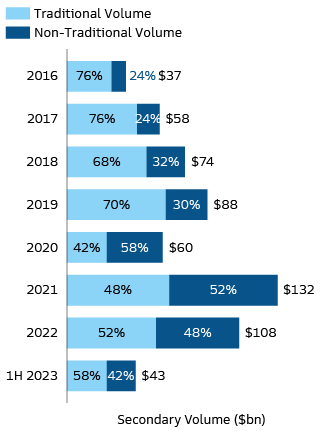

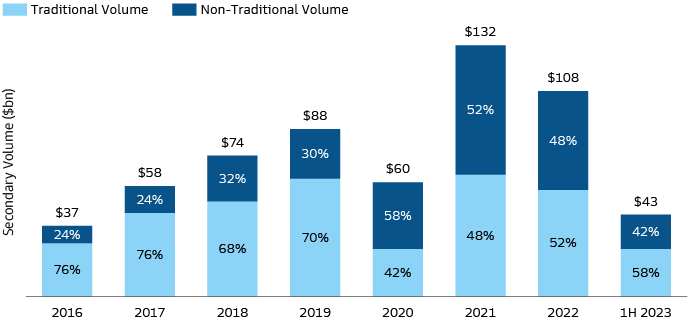

Continuation vehicles had been steadily gaining prominence prior to 2020, growing from less than 20% of the secondary market in 2015 to 30% of all transactions in 2019, even as the overall volume more than doubled. In the pandemic downturn in early 2020, many LPs pulled back on traditional portfolio sales as equity markets fell and discounts widened, but continuation vehicle transactions proved more resilient, representing more than half the total deal volume for the year. GP led deal activity slowed in 2022 along with the broader secondary market. As exits and distributions have slowed in 2022 and 2023, the relative need for LP portfolio sales has risen, pushing nontraditional volume to 42% of secondary activity in 1H 2023.5 Going forward, we expect secondary market volume to be split roughly evenly between LP portfolio sales and non-traditional activity, with cyclical factors impacting year-to-year changes.

Source: Jefferies Global Secondary Market Review – July 2023.

Another transaction type that has increased in frequency is preferred equity or structured secondaries. In these transactions, a secondary capital provider offers financing that is securitized by a portfolio of assets or collateral pool. Following the investment, the preferred equity holders receive a disproportionate share of the portfolio’s value until the initial investment is repaid with a contractual return, as well as potential for additional upside in the growth of the portfolio thereafter.

GPs utilize preferred equity to pursue buy-and-build strategies with portfolio companies in funds that have more limited remaining capital, but where extending the holding period through a continuation vehicle may not be necessary. Similar to other solutions in the secondary market, GPs can use the proceeds of preferred equity deals to satisfy LPs who have the desire to accelerate liquidity without giving up 100% of their upside. In more complex and multifaceted secondary transactions, preferred equity can also be a useful tool to help satisfy the requirements of the various parties involved.

Particularly in times of stress, preferred equity solutions can provide managers, funds, or assets with needed liquidity in exchange for a preference on future cash flows. GPs also turn to preferred equity rather than debt due to the bilateral nature of the financing arrangement and lack of covenants. Preferred equity drew particular attention during the COVID-19 pandemic when GPs turned to the strategy to fund portfolio companies as revenues were interrupted and credit markets were not available. Buyers in these deals were able to rely on the potential downside protection characteristics to deploy earlier into the pandemic than other transaction types, while borrowers took advantage of the speed and flexibility of these financing solutions. In the recent environment, preferred equity is increasingly viewed as a means of providing intermittent liquidity to existing LPs, while also potentially bolstering an asset’s balance sheet.

The secondaries market is likely to continue its growth trajectory, with transaction volumes increasing alongside private markets more broadly. Secondaries firms are also likely to continue innovating around the structural limitations of private assets and the diverse needs of GPs and LPs, building new solutions around inefficiencies and complexity to pursue attractive returns for investors. While scale is necessary to execute larger portfolio transactions and remain competitive in the market, executing secondary transactions in the growing areas outside of traditional buyout LP interests requires the ability to value different types of assets, and understand future cash flow streams.

As the variety and complexity of transactions increase, a combination of experience and creativity will be required to design solutions benefitting all parties while maintaining an appropriate alignment of incentives. Moving forward, success across the full spectrum of capital solutions will require the breadth and flexibility to operate seamlessly throughout various asset classes, coupled with the depth and focus to structure and execute complex transactions to liquidity, and beyond.

Committed to providing you with the insights you need to build your practice.

1 Preqin. As of September 2023.

2 Evercore H1 2023 Secondary Market Survey. As of July 2023.

3 Jefferies H1 2023 Global Secondary Market Review. As of July 2023.

4 Jefferies H1 2023 Global Secondary Market Review. As of July 2023.

5 Jefferies H1 2023 Global Secondary Market Review. As of July 2023.

Glossary

Buyout is an investment transaction by which the ownership equity of a company or a majority share of the stock of the company is acquired.

Continuation vehicles typically involve the transfer of the target asset(s) from the original private markets fund into a new vehicle.

Dislocation describes market activity in securities where the price is disconnected from the fundamentals.

Drawdown is an investment’s peak to trough decline.

Dry powder refers to marketable securities that are highly liquid and considered cash-like.

J-curve refers to the cumulative net cash flow seen by an investor, which for private equity investments is typically negative in the first several years after the initial commitment due to capital being drawn down for investments and generally becomes positive after capital is returned and the fund becomes net cash flow positive.

Limited Partner (LP) refers to the investors into private equity funds which are managed by a General Partner (GP) .

Private Credit refers to non-bank lending that is not issued or traded in public markets.

Real Assets describes investments into physical structures s, including real estate and infrastructure

Risk Considerations

All investing involves risk, including loss of principal.

Alternative investments are suitable only for sophisticated investors for whom such investments do not constitute a complete investment program and who fully understand and are willing to assume the risks involved in Alternative Investments. Alternative Investments by their nature, involve a substantial degree of risk, including the risk of total loss of an investor’s capital.

Private equity investments are speculative, highly illiquid, involve a high degree of risk, have high fees and expenses that could reduce returns, and subject to the possibility of partial or total loss of fund capital; they are, therefore, intended for experienced and sophisticated long-term investors who can accept such risks.

Alternative Investments often engage in leverage and other investment practices that are extremely speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested. There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers.

Investors should also consider some of the potential risks of alternative investments:

· Alternative Strategies. Alternative strategies often engage in leverage and other investment practices that are speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the entire amount that is invested.

· Manager experience. Manager risk includes those that exist within a manager’s organization, investment process or supporting systems and infrastructure. There is also a potential for fund-level risks that arise from the way in which a manager constructs and manages the fund.

· Leverage. Leverage increases a fund’s sensitivity to market movements. Funds that use leverage can be expected to be more “volatile” than other funds that do not use leverage. This means if the investments a fund buys decrease in market value, the value of the fund’s shares will decrease by even more.

· Counter-party risk. Alternative strategies often make significant use of over- the- counter (OTC) derivatives and therefore are subject to the risk that counter-parties will not perform their obligations under such contracts.

· Liquidity risk. Alternatives strategies may make investments that are illiquid or that may become less liquid in response to market developments. At times, a fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all.

· Valuation risk. There is risk that the values used by alternative strategies to price investments may be different from those used by other investors to price the same investments.

Alternative Investments - Hedge funds and other private investment funds (collectively, “Alternative Investments”) are subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains and an individual’s net returns may differ significantly from actual returns. Such fees may offset all or a significant portion of such Alternative Investment’s trading profits. Alternative Investments are not required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of such Alternative Investments.

Conflicts of Interest

There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. These activities and interests include potential multiple advisory, transactional and other interests in securities and instruments that may be purchased or sold by the Alternative Investment. These are considerations of which investors should be aware and additional information relating to these conflicts is set forth in the offering materials for the Alternative Investment.

The above are not an exhaustive list of potential risks. There may be additional risks that are not currently foreseen or considered.

General Disclosures

The website links provided are for your convenience only and are not an endorsement or recommendation by Goldman Sachs Asset Management of any of these websites or the products or services offered. Goldman Sachs Asset Management is not responsible for the accuracy and validity of the content of these websites.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

The J-curve refers to the cumulative net cash flow seen by an investor, which for private equity investments is typically negative in the first several years after the initial commitment due to capital being drawn down for investments and generally becomes positive after capital is returned and the fund becomes net cash flow positive.

Diversification does not protect an investor from market risk and does not ensure a profit.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

The views expressed herein are as of the date of the publication and subject to change in the future. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, a licensed entity regulated by the Securities and Futures Commission of Hong Kong (SFC). This material has not been reviewed by the SFC. © 2023 Goldman Sachs. All rights reserved.

Singapore: Investment involves risk. Prospective investors should seek independent advice. This advertisement or publication material has not been reviewed by the Monetary Authority of Singapore. This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

· Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

· Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

· Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

· Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws.

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

New Zealand: This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar: This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser. The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

East Timor: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds), or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed under any laws or regulations of Timor-Leste. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person or institution without the prior consent of Goldman Sachs Asset Management.

Vietnam: Please Note: The attached information has been provided at your request for informational purposes only. The attached materials are not, and any authors who contribute to these materials are not, providing advice to any person. The attached materials are not and should not be construed as an offering of any securities or any services to any person. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer under the laws of Vietnam. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Cambodia: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds) or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer or investment advisor under The Securities and Exchange Commission of Cambodia. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

336800-OTU-1884899 Date of First Use: October 31, 2023