Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsINVESTING IN FINANCIAL INCLUSION: DRIVING GROWTH AND BUILDING WEALTH

April 10, 2024 | 13 Minute Read

Jamison HillManaging Director, Horizon Inclusive Growth Jamison Hill |

Ivo LuitenPortfolio Manager, Impact Equity Ivo Luiten |

Roel van BroekhuizenPortfolio Manager, Green, Social and Impact Bonds, Goldman Sachs Asset Management Roel van Broekhuizen |

Key Takeaways

- Expanding Access to Affordable Finance

Financial inclusion is a critical component of inclusive growth. Growing awareness of its importance is spurring the development of tech-based solutions that broaden access to affordable financial services, creating opportunities for investors.

- Investing in Real-World Impact

Investors can discover innovative fintech companies promoting financial inclusion in developed and emerging markets by using an impact-focused approach across assets classes such as private equity, social bonds and listed equities.

- Fintech Focus in Private Equity

Private equity can provide exposure to the fintech sector through investment in new digital brands aimed at underserved consumers and software providers with embedded financial products that facilitate wealth-building.

- Social Bonds Drive Inclusive Lending

Banks are using social bonds to finance vital lending to low-income individuals and small businesses in regions facing economic challenges. For investors, social bonds offer a way to advance sustainability goals without sacrificing liquidity or returns.

- Impact Equity in Emerging Markets

Investment strategies focused on achieving impact in listed equities are helping address the connectivity gap and enhance financial inclusion around the world. The tasks in emerging markets often focus on mobile-based finance and telecoms infrastructure.

Overdraft fees in the US that can spiral into hundreds of dollars in a few hours. Small businesses in Europe’s poorest regions that struggle to find the financing they need to grow. Millions of people in emerging economies who have no access to financial services because they live in areas without banks or even a digital network.

These are just a few of the obstacles low-income people and those in less developed regions can face when they try to use the financial system. As the sustainable transformation of the global economy gathers pace, policy makers and investors increasingly recognize that removing these barriers is an essential step in building a more inclusive economy.1 The growing awareness of the importance of financial inclusion, combined with the slow adjustment of traditional lenders, has spurred companies around the world to come up with new solutions, and this surge of innovation is changing the game for sustainable investors.

The World Bank defines financial inclusion as individuals and businesses having access to useful, affordable financial products and services – transactions, payments, savings, credit and insurance – that meet their needs and are delivered in a responsible and sustainable way.2 This access can help people handle their everyday financial needs more safely and affordably, improve their resilience in emergencies and allow them to make investments that create wealth for the future. The central role of financial inclusion in poverty reduction and equitable growth is highlighted by the United Nations, which cites it as a key factor in achieving seven of the Sustainable Development Goals (SDGs), including those that address hunger, health and gender equality.3

Many of the solutions aiming to promote financial inclusion deploy new technology to improve the delivery and reduce the cost of financial services, such as a US digital bank offering overdraft protection to its clients. In some African countries with few banks and no fixed broadband networks, companies are developing mobile broadband and mobile phone-based financial services. European banks are using a new financial product – social bonds, which first appeared in 2015 – to raise funds earmarked for lending to small businesses in deprived areas and low-income individuals.

The market for investing in financial inclusion has now matured to the point where companies like these that are making a real difference for their customers also offer the prospect of attractive financial performance for investors. By using an impact-focused approach in asset classes such as private equity, social bonds and listed equities, investors can discover the wide array of opportunities available across developed and emerging markets.

Unaffordable Finance in Developed Markets

In developed markets, the challenge in promoting financial inclusion is to expand access to affordable products and services that allow people to build wealth. Without access to the mainstream financial system, many people who need to make transactions or borrow money are forced to use alternatives such as check-cashing operations, rent-to-own services and loans from pawn shops. These providers tend to have looser standards than traditional lenders – no FICO credit score required in the US, for example.4 They cluster in low-income neighborhoods, making them more accessible. Their products, however, are expensive and offer no opportunities to build wealth.

The scale of this problem – even in wealthy countries – can be seen in the US, where 5.9 million households were “unbanked” in 2021, meaning no one in the household had a checking or savings account at a bank or credit union. Another 18.7 million US households were “underbanked.” This means they had a bank account, but still resorted to products or services such as payday and pawn shops loans that are “disproportionately” used by those without access to banks.5

The concept of financial inclusion encompasses much more than bank accounts, however. The pain and stress of exclusion is felt in many ways. Those overdraft fees collected by the big US banks amount to more than $11 billion each year, and 84% of that is paid by people with average balances below $350.6 Overall, 64% of American consumers live paycheck to paycheck; even for those earning more than $100,000 a year, the number is 48%.7

Private Equity: Driving Fintech Solutions

Financial technology (fintech) companies in developed markets are leading the way in devising solutions to make financial services more affordable and tailor them to the needs of lower-income consumers. Smartphone penetration and modern software capabilities, in particular cloud computing, the proliferation of application programming interfaces, and artificial intelligence have coalesced to create a generational opportunity to transform and increase access to financial services.

We believe fintech will be one of the biggest investment opportunities in financial inclusion over the next decade. The private equity market can provide exposure to this rapidly evolving theme through investments in new digital brands aimed at underserved consumers and software providers with embedded financial products that facilitate wealth-building, for example by improving the user experience with government benefits providers. We think private markets are well suited to finance the development of these innovative companies that may require significant capital investment and time to realize their potential.

One example is a privately owned US fintech company that partners with regional banks to provide low-cost banking services through its platform. It brings down the cost of entry to basic banking by providing checking and savings accounts with no monthly fees or minimum balance requirements. Its commitment to expanding access to affordable finance also includes fee-free overdraft and a credit card with no annual, interest or late fees.8 This company and others like it have shown that there are real businesses to be built by serving the underserved.

Social Bonds: Supporting Small Business

Just as individuals and households suffer when they are cut off from the financial system, small businesses also feel the pain. One of the biggest issues they face is securing the financing they need to expand. In the euro area, for example, 24% of small and medium-sized enterprises (SMEs) reported severe difficulties in accessing finance in the first half of 2023 as borrowing costs rose and banks tightened SME lending standards.9

The struggles of small businesses to access finance can have knock-on effects for the communities they serve because of their central role in driving inclusive growth. In the European Union, 25 million SMEs, accounting for 99% of all businesses, create 85% of all new jobs.10 Micro-enterprises, which play a vital role in job creation in European regions with high unemployment, are even less likely to seek bank loans than larger companies because of higher rejection rates, stringent collateral requirements, high interest rates and bureaucratic hurdles.11

Some European banks are responding by using social bonds to raise funds for lending to promote the financial inclusion of SMEs.12 For example, a Spanish lender uses the proceeds from social bond sales to finance loans to self-employed workers, micro- and small businesses in parts of the country that are facing severe economic challenges. The bank also uses social bonds to provide loans to low-income individuals, helping recipients achieve goals such as access to decent and affordable housing, meeting basic family needs and gaining access to healthcare.13

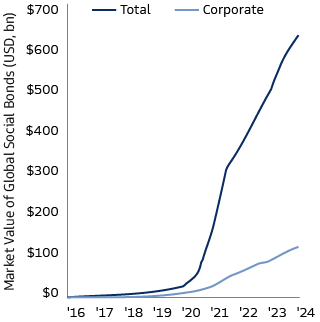

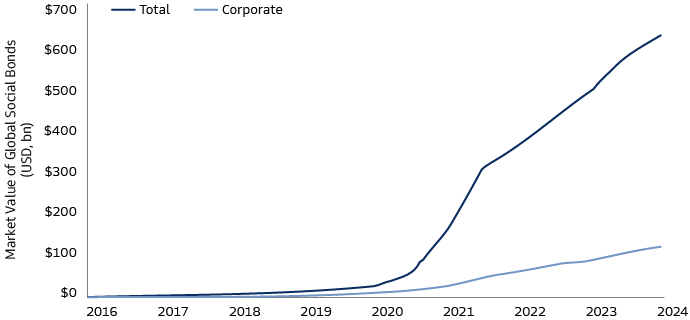

The social bond market has expanded to more than $630 billion in less than a decade, supported by strong investor demand.14 For issuers, tapping into this demand can provide a cost-effective way to raise funds to drive projects aimed at financial inclusion and other objectives.15 For investors, social bonds offer a way to advance their sustainability goals without sacrificing liquidity or returns. A key feature of social bonds is that their legal documentation spells out how their proceeds will be used, with the goal of financing only projects with clear social benefits. Issuers are also expected to report annually on the progress of projects financed with social bonds and the impact achieved.

The Global Social Bond Market Has Expanded to $639 Billion in Under a Decade

Source: Goldman Sachs Asset Management, Bloomberg. As of December 31, 2023.

Connecting People With Finance in Emerging Markets

In emerging markets, the obstacles to financial inclusion are more extensive than in developed countries. Of the 1.4 billion adults worldwide who remained unbanked in 2021, nearly all of them lived in developing economies. As a result, just 57% of adults in developing economies made or received digital payments, compared with 95% in in high-income economies.16

Improving financial inclusion in these regions will depend on expanding ownership of transaction accounts, which allow people to receive salaries and remittances safely and securely. This is more than a convenience: these accounts open the door to more efficient saving, cheaper borrowing, obtaining insurance and investing in life-enhancing services such as health and education.

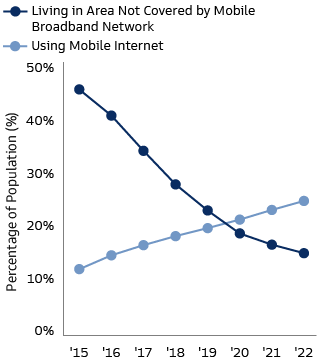

Where banks are scarce, the adoption of mobile financial services can be one of the most efficient solutions, allowing countries to leapfrog the traditional financial infrastructure of the developed world. In many cases, however, the first step is to increase digital connectivity. An estimated 2.9 billion people were still offline in 2021, with 1.7 billion in the Asia-Pacific region – mostly in China and India – and about 740 million in Africa.17 Huge disparities are also found between urban and rural areas.

Impact Equity: Building the Network

Investment strategies focused on achieving impact and returns in listed equities are helping address the connectivity gap and enhance financial inclusion around the world. To make a positive impact, companies need to offer unique, innovative products and services. Technology is at the core of this effort, as it is in developed economies, but the tasks in emerging markets often focus on building the infrastructure needed for mobile financial services to thrive.

One company, for example, is developing telecommunications infrastructure in sub-Saharan African countries from Madagascar to Senegal. It owns and operates more than 14,000 telecom towers and enables mobile network coverage for over 144 million people, especially in rural areas. This has made the company a key player in the roll-out of mobile service in Africa and an important enabler of digital inclusion.18

Another company is building on this infrastructure, providing affordable mobile services to 151 million customers in 14 African markets, including data customers and users of its mobile money business.19 Its target is to ensure that around 90% of the population in its markets have access to mobile network services by 2030. The company has also set financial inclusion targets, including boosting the number of women using its mobile money product.20

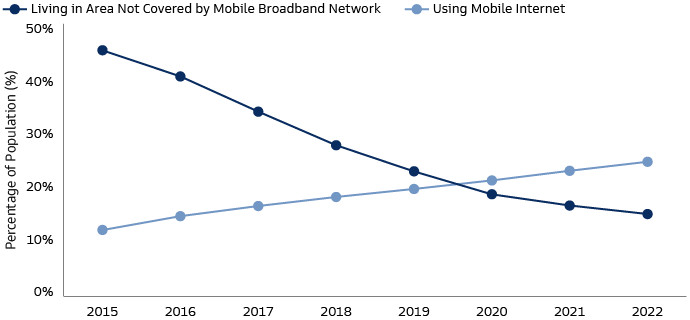

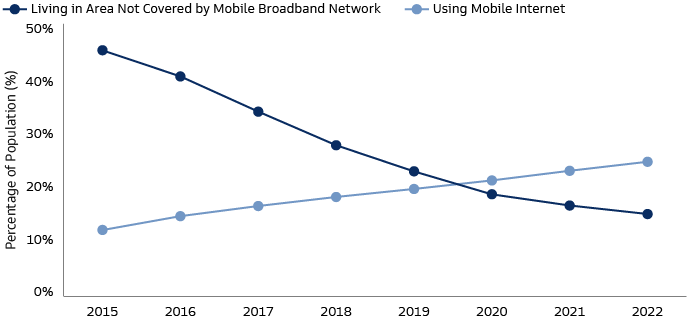

Narrowing the Mobile Coverage Gap in Sub-Saharan Africa

Source: GSMA, Goldman Sachs Asset Management. Data as of December 31, 2022.21

Impact and Returns

The tech-driven revolution in financial services has transformed the market for investors seeking to promote financial inclusion and sustainable growth. In developed markets, fintech companies that make vital services affordable are expanding fast, demonstrating the viability of a business model based on bringing underserved groups into the financial system. In emerging markets, companies are successfully deploying technology to bring millions into the internet age and connect them to the financial grid through mobile services. And traditional financial firms are using innovative products like social bonds to raise funds earmarked for lending to low-income borrowers and small businesses. For investors, these companies show how far financial inclusion investment has come in recent years. Once viewed as concessionary investing, the market has progressed to the point where the dual goals of sustainable investing – social impact and returns – are increasingly aligned.

Related Insights

×

Start the Conversation

Committed to providing you with the insights you need to build your practice.