Much like a dampener is used to remove energy from mechanical systems, tight financial conditions have been the tool utilized by central banks to slow global growth. Dampeners of growth have diverged as 1) monetary policy cycles have varied in response to regional inflation, and 2) credit tightening has emerged as a potentially powerful drag in some economies. Their uncertain impacts have left many investors sitting idly by as opportunities in risk assets feel few and far between.

With that said, markets seem to be pricing the best of all worlds—inflation moderating, policy rates falling, and recessions evaded. Still, seemingly more room to the downside than upside has made entry points difficult to identify, driving a flight to cash-equivalents. While attractive, the yield provided in ultra-short fixed income may be fickle, and kicking the can down the road on strategic allocations could prove costly for investors.

Objects at rest will remain as such unless acted on by an external force. Similarly, portfolios will remain unbalanced if strategic implementation is put off. Signals as to when to apply that force rarely align perfectly for investors. But in our view, they might not need to, as regional divergence has presented a diverse opportunity set to position across asset classes.

In this edition of the Market Know-How, we explore how investors may invest strategically in a post-monetary tightening regime, with emphasis on:

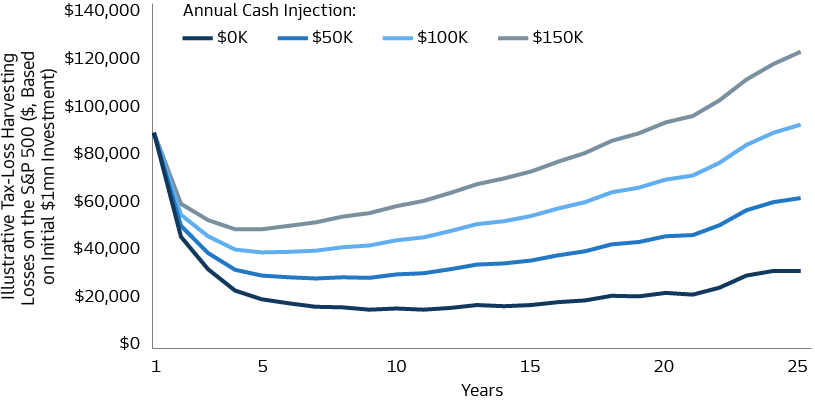

- Increasing the frequency of loss-harvesting via tax-advantaged SMAs to drive bottom-line tax savings.

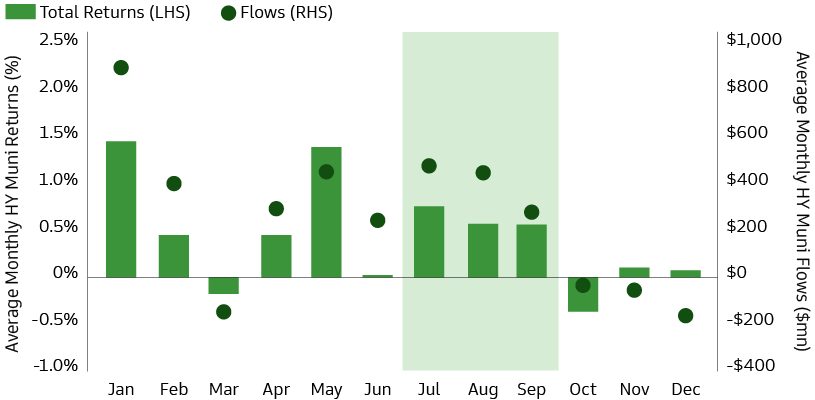

- Solving for various investor needs with high yield municipal bonds, particularly as technicals may turn more favorable.

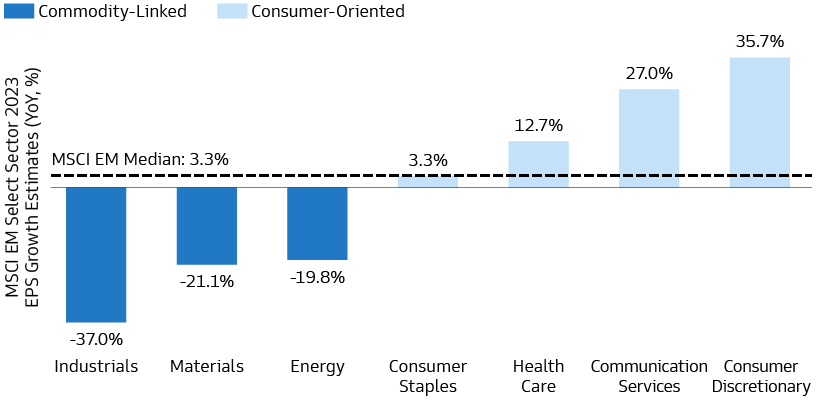

- Active selection within emerging market equities, which are set to potentially benefit from a consumer-led earnings recovery.