June 22, 2022 |

GSAM Connect

Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsTHE MICRO FOOTPRINTS OF MACRO RISKS

CIO Macro and Market Observations from Multi-Asset Solutions

June 29, 2022 | 8 Minute Read

Authors: Maria Vassalou, PhD and Amy Yifan Zhou, PhD

Household finance can provide differentiated micro-level perspectives into macro business cycles. For the moment, risks associated with household credit appear moderate compared to historical levels. But vulnerabilities on the asset side are notable. In today’s accelerated monetary tightening cycle, the risks of equity selloff and a housing slowdown are top of mind, though they will have different effects on different populations, depending on their income and the composition of their balance sheets. Ultimately, weaker consumers with diminished assets may need to tap into their credit lines, which spreads risk back to the liability side.

Household Debt Concerns

Recent evidence suggests that consumers are accumulating debt. As of Q1 2022, aggregate household debt in the US has surged to its historical record of nearly $16 trillion despite persistently higher interest rates. In other words, American households are borrowing more at higher costs. Over the past year and a half, the national average of 30-year fixed mortgage rate has increased rapidly from below 3% to almost 6%, which means monthly mortgage payments have nearly doubled.

On a relative basis, this level of household debt burden isn’t unprecedented. Currently, the US household debt-to-GDP ratio is about 75%, compared to nearly 100% during the Great Financial Crisis; household debt-to-income and debt service ratios are also below their historical highs. But will households hold up in an environment of high rates and volatile markets? To answer this question, we examine the size of household balance sheets and identify areas of vulnerabilities.

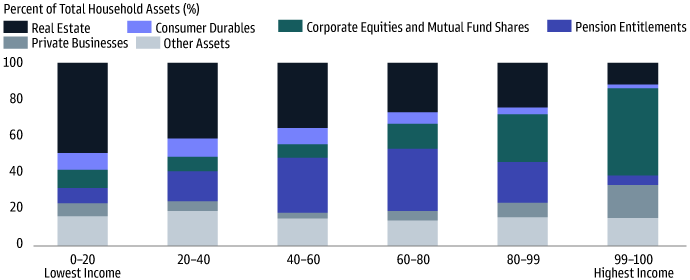

Exhibit 1. Household Assets by Income Quintiles (2021 Q4)

Source: Federal Reserve Board of Governors, Goldman Sachs Asset Management.

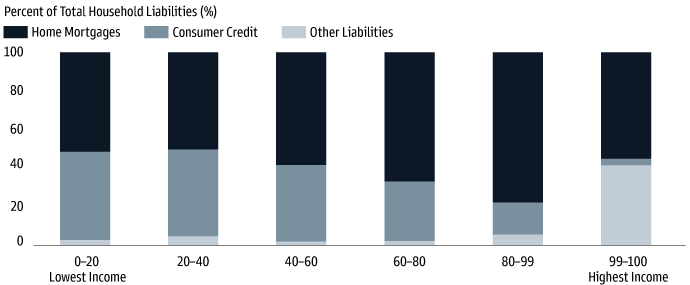

Exhibit 2. Household Liabilities by Income Quintiles (2021 Q4)

Source: Federal Reserve Board of Governors, Goldman Sachs Asset Management.

How Household Vulnerabilities May Translate Into Assets Vulnerabilities

The composition of household assets and liabilities is variable across demographics. For the lowest earners (bottom 20% by income), real estate accounts for about half of their assets. As we move up in income distribution, financial markets begin to play a bigger role. For the highest earners (top 1% by income), more than 60% of their assets are in corporate equities, mutual fund shares, and private businesses. Real estate for this group accounts for just 12% of assets. On the liability side, home mortgages take up the biggest share across the board, as expected; the lower earners also appear to be more dependent on consumer credit than higher earners.

As a result, the low- and high-income cohorts may exhibit different types of vulnerabilities with respect to macro shocks: low earners are more susceptible to home price fluctuations, whereas the high earners are more sensitive to equity market selloffs. The Fed is working hard to curb inflation with aggressive interest rate hikes. Aggregate demand is likely to cool down, and home prices are expected to appreciate less or even depreciate in the foreseeable future. For the lower earners, this implies that their asset levels can be at risk, but their mortgage liabilities are already tied to the higher prices that prevailed during the housing boom, leaving fewer resources available for consumption. On the other hand, following the year-to-date market selloffs, equity valuations have already re-priced significantly but earnings expectations have not. An earnings repricing would trigger downside risks in equities, shrinking the asset level for higher earners and reducing their willingness to consume.

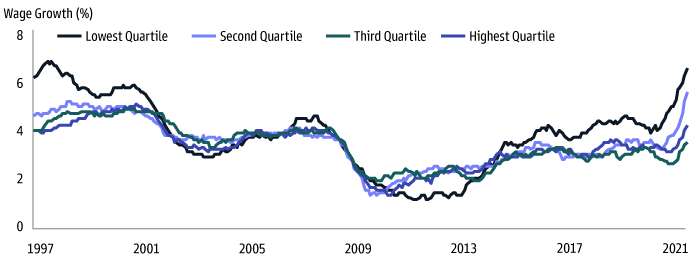

Furthermore, the lack of wage growth may pose additional challenges for accumulation of assets. Record-high inflation is already outpacing aggregate wage growth, which is growing at the slowest pace within the highest-paid quartile. This isn’t good news for the high earners, for whom wages and salaries account for more than 80% of pre-tax income. Faster wage growth at the lower end alone are unlikely to provide a sufficient boost to consumption either, since wages and salaries only account for 30% of pre-tax income for the lowest income quintile1.

Exhibit 3. Wage Growth by Quartile (12 Month Average of Median Wage Growth)

Source: Federal Reserve Bank of Atlanta, Bureau of Labor Statistics, Goldman Sachs Asset Management.

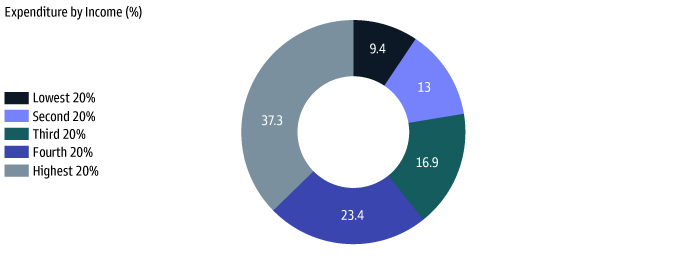

Exhibit 4. Annual Aggregate Expenditure by Income Quintiles

Source: Federal Reserve Bank of Atlanta, Bureau of Labor Statistics, Goldman Sachs Asset Management.

The Macro Implications of Consumer Weakness

Overall, asset-side vulnerability suggests that household consumption is likely to weaken in the foreseeable future, although the source of pressure may be different across the income spectrum. The top 30% earners today account for half of aggregate consumption, whereas the lowest 20% earners account for less than 10%. As top earners pull back, discretionary spending is likely to be one of the earliest casualties. In turn, weaker consumption in the aggregate economy may also lead to weaker equity earnings and pose further challenges to asset returns.

The vicious cycle of lower consumption spending by the top 30% of earners leading to lower corporate earnings and equity returns, prompting the top earners to further constrain their consumption can continue until we see a meaningful deceleration in inflation pressures. In the meantime, lower earners can easily become distressed as they increasingly tap their credit lines at ever higher interest rates. In other words, the debt burden can deteriorate faster for the lower income cohort who has higher dependency on consumer credit. The timing of policy actions will be important for limiting the transmission of asset price weakness into credit risk, and the choices consumers make will help determine the path of the household credit cycle and the depth of any economic downturn that may result.

All Eyes on the Consumers

The above suggest that monitoring closely consumer behavior across income brackets is key in determining asset behavior going forward. In the absence of any obvious pathologies in the economy, another implication is that this time around, a recession is likely to be broad-based, shallow but perhaps harder to rebound from, as the room for fiscal and monetary accommodation may be much more limited than in previous episodes. Active, nimble investing and careful risk management would be key in navigating the current environment.

About the Authors

Maria Vassalou, PhDCo-Chief Investment Officer, Multi-Asset Solutions Maria Vassalou, PhD |

Amy Yifan Zhou, PhDInvestment Center Director, Multi-Asset Solutions Amy Yifan Zhou, PhD |

Related Insights

×

Start the Conversation

Committed to providing you with the insights you need to build your practice.