- No services available for your region.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsMAKING SENSE OF THE RETIREMENT INCOME QUAGMIRE

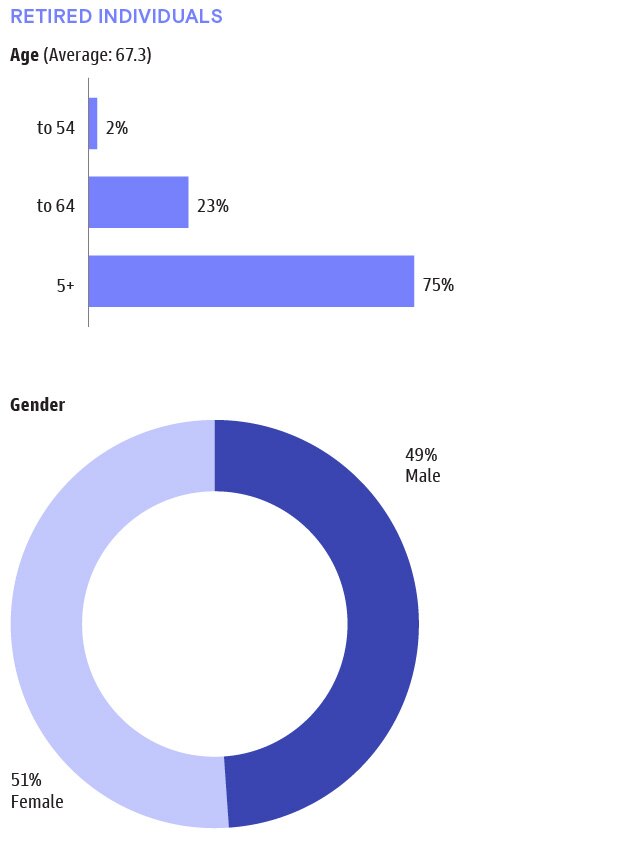

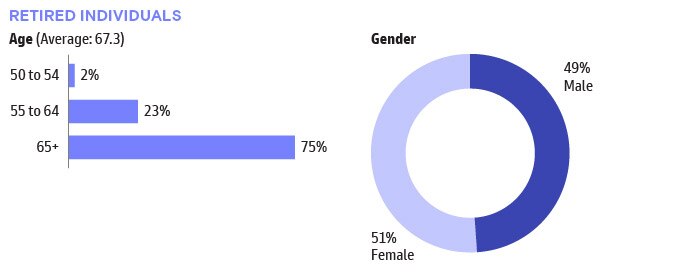

Though many individuals look forward to the days of retirement, it is not as easy as one may hope. Our survey found that individuals reach retirement with insufficient savings and then need to manage spending and income generation, all while estimating how long their savings will last. In the current environment, this is incredibly challenging and so it is no surprise that many spend conservatively, desire income that is stable, consistent and guaranteed, and seek retirement income advice to help them navigate.

As plan sponsors seek to tackle retirement income offerings in their plans, it is important to recognize that employer-sponsored retirement plans drop as a primary source of education and advice for retiree respondents. They dropped from the second most used source of education for workers preparing for retirement to sixth for those in retirement. For plan sponsors seeking to retain plan participants through retirement, this is an important consideration along with the mix of retirement income products and services to support their retiree needs.

This section explores the different aspects associated with retirement income, such as managing spending, deciding on the best way to generate income, and key features of retirement income.

Many Retirees May Not Have Enough Savings for Retirement

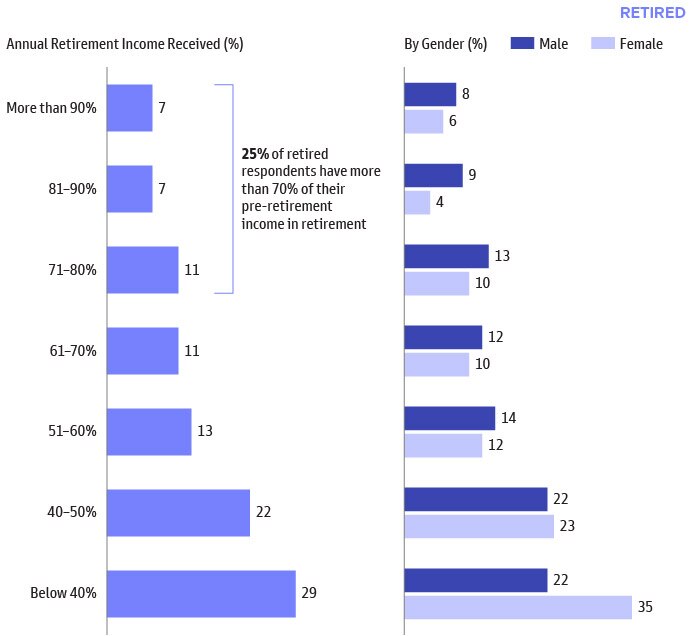

It is commonly suggested that 70% pre-retirement income is needed to maintain the standard of living in retirement. But based on survey findings, only 25% reach retirement and receive at least 70% pre-retirement income and more than half (51%) receive less than 50% of their pre-retirement income.

Women respondents report facing an even greater challenge accumulating sufficient saving, with 80% receiving less than 70% pre-retirement income and, notably, 35% receiving less than 40% of pre-retirement income.

How much total annual income do you receive in retirement (including Social Security) relative to your pre-retirement income (e.g., your final annual compensation prior to retirement, such as salary, bonus, etc.)?

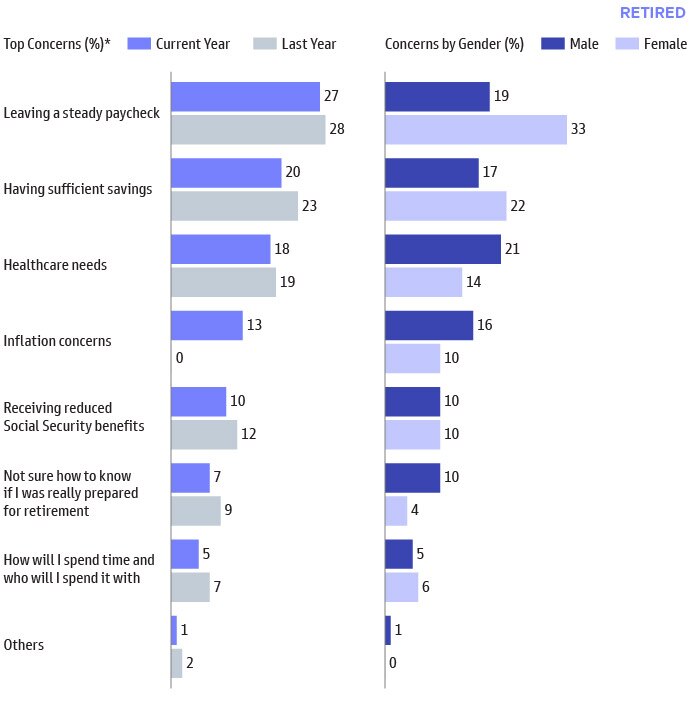

Top Concerns Entering Retirement

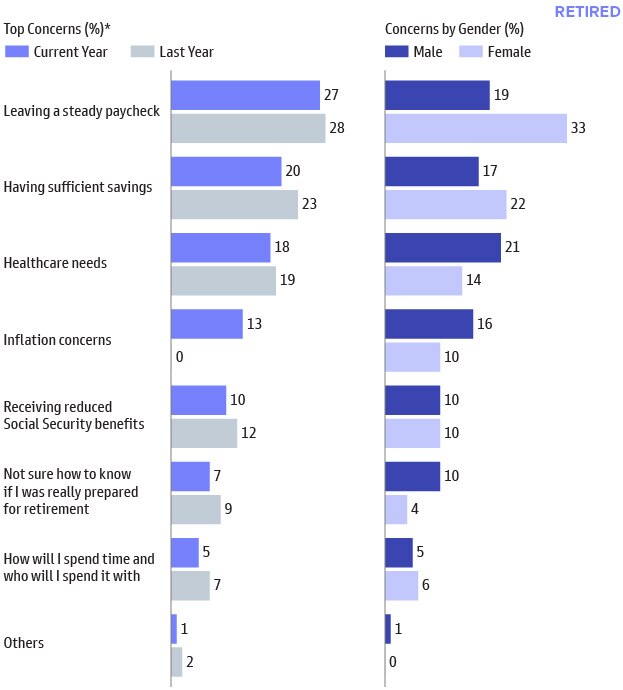

Leaving a steady paycheck is a top concern for those entering retirement, ahead of healthcare, inflation and having sufficient savings.

This concern highlights the importance for retirees to understand what income they will receive and how they will manage their income to support their needs in retirement.

When we break it down by gender, we see a much wider disparity. Women respondents are even more concerned with leaving a steady paycheck than men, while men responding are more focused on healthcare needs and inflation.

What concerns, if any, did you have entering retirement? (Select all that apply)

*Inflation was not an option in last year’s survey.

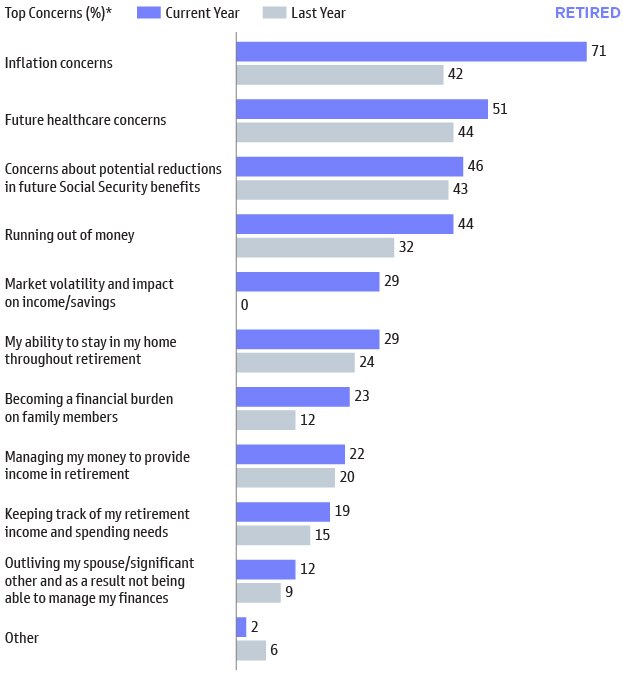

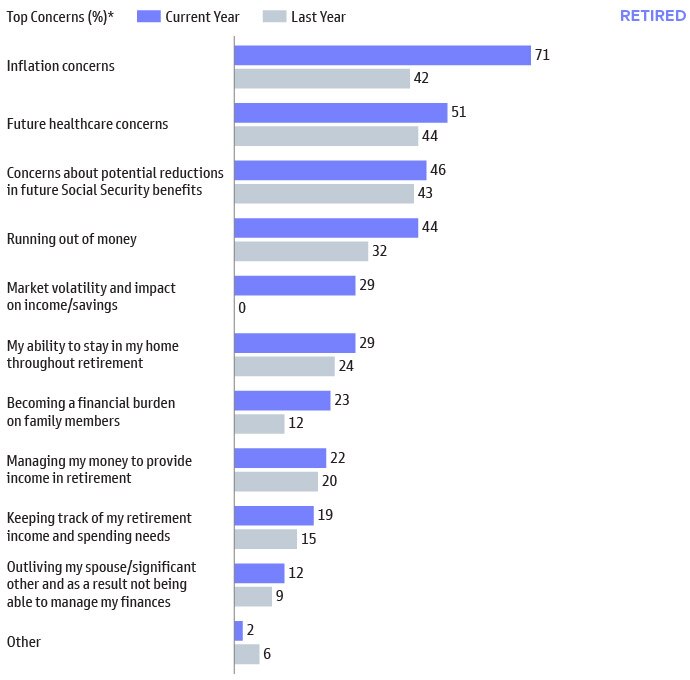

Inflation Is a Top Concern for Retirees

While the level of concerns have increased across the board relative to last year, inflation rose to the top spot in this year’s report for retired respondents.

The challenge with inflation is that it impacts all the key questions retirees need to address, such as:

- How much should I spend (with prices rising)?

- How much income can I withdraw (with markets down)?

- How long will my savings last (with increased spending needs in the future)?

Regardless of future inflationary conditions, the past two years of record inflation alone will have a meaningful impact on retirees’ accumulated savings.

Which of the following, if any, are concerns you have about your retirement at the moment? (Select all that apply)

*Market volatility and impact on income/savings was not an option in last year’s survey.

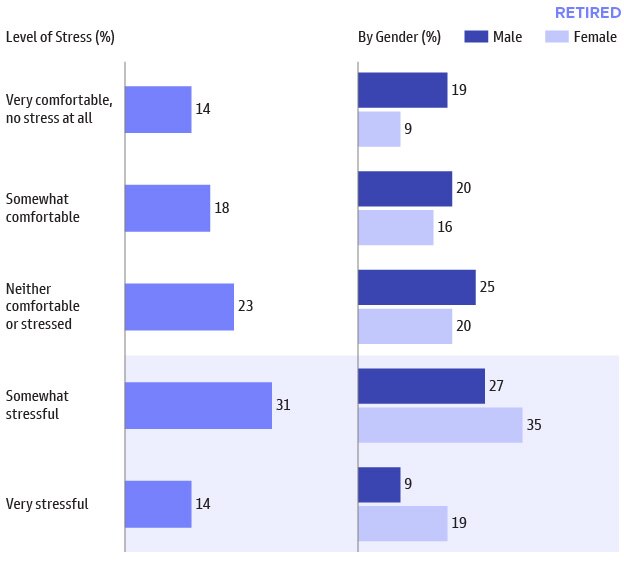

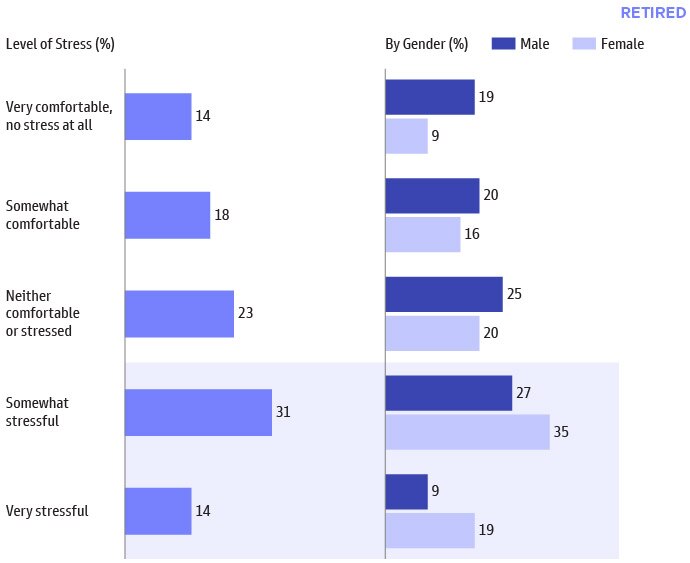

Retirees Entering Retirement with Financial Anxiety

A number of factors contribute to a stressful transition to retirement, including leaving a paycheck behind. There are many difficult questions to answers, such as:

- Do I have enough savings?

- How do I generate income?

- How much can I spend each year?

- How long will it last?

Unfortunately, it is impossible to know these answers with certainty and as a result, some experience financial anxiety as they navigate the trade-offs.

Women respondents report higher levels of stress than men entering retirement. Later in the report we highlight women respondents’ preference to generate retirement income from part-time work, which can alleviate the stress felt during the transition phase.

How much anxiety/stress about your finances did you feel entering retirement?

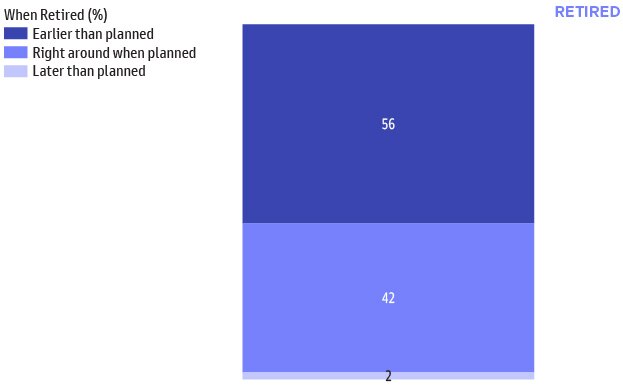

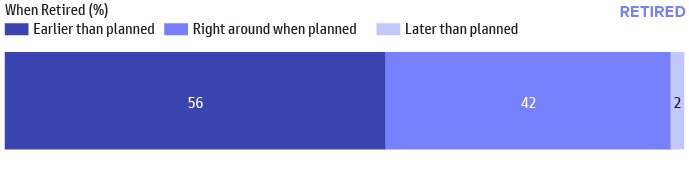

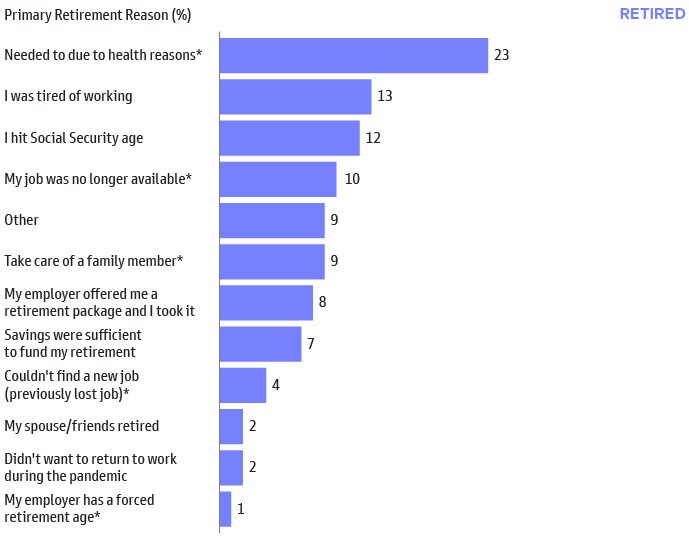

Retiring Earlier than Planned Has a Significant Impact on Retirement Savings

Fifty-six percent of retirees state they retired earlier than planned, which can impact final accumulated savings, savings longevity, and when one claims Social Security, among other things.

Since over half of retired respondents retired earlier than planned, building a strategy that incorporates this reality can help alleviate the impact.

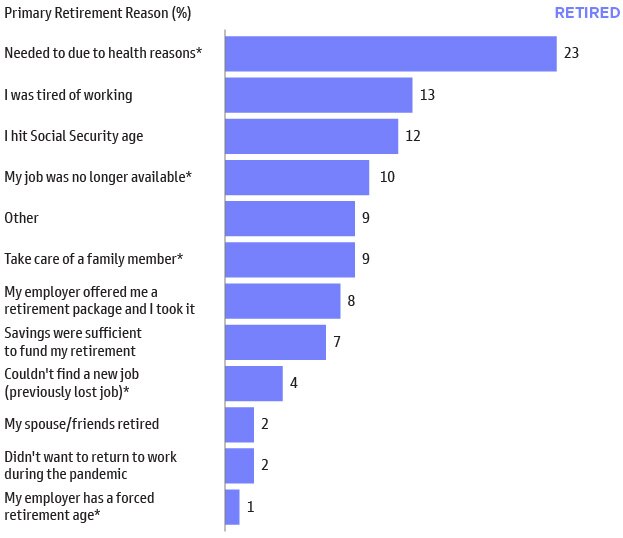

Notably, only 7% state that the primary reason for retirement was having sufficient savings.

However, almost half (47%) retired due to reasons outside of their control with health reasons (23%) being the top factor. The ability to delay retirement to accumulate additional savings or to work part-time in retirement could all be impacted by health or other factors outside one’s control.

Did you retire earlier, right around, or later than planned?

What is the primary reason that you retired? (Select only one)

*Reasons considered outside the individual’s control.

Uncertainty Drives Conservative Spending

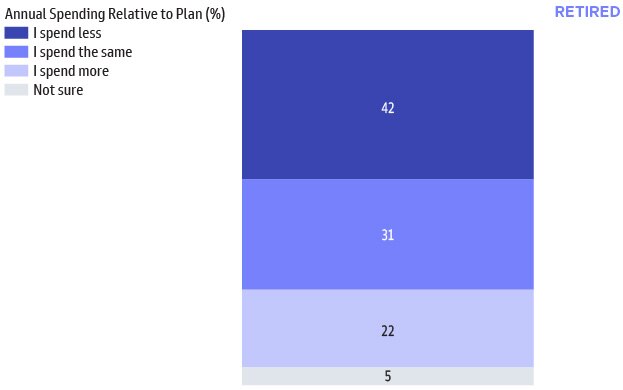

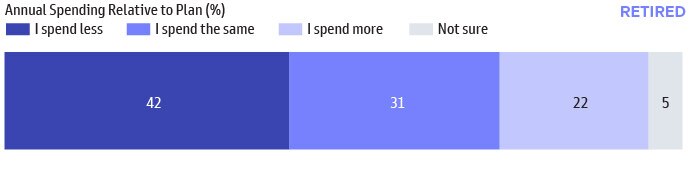

While many enter retirement without sufficient savings, we see a range of spending behaviors.

About four in ten retirees spend less than anticipated or planned, which illustrates that retirees may not have the retirement they had expected. Only 22% spend more than anticipated, which may be impacted by the current inflationary environment and rising costs.

Consistent with these results, the top action retirees have taken in the current environment is to reduce their spending. Controlling what they can control, some retirees are reducing spending to effectively preserve savings and help manage the potential long-term effects of inflation.

Unfortunately, this is not an optimal outcome for retirees.

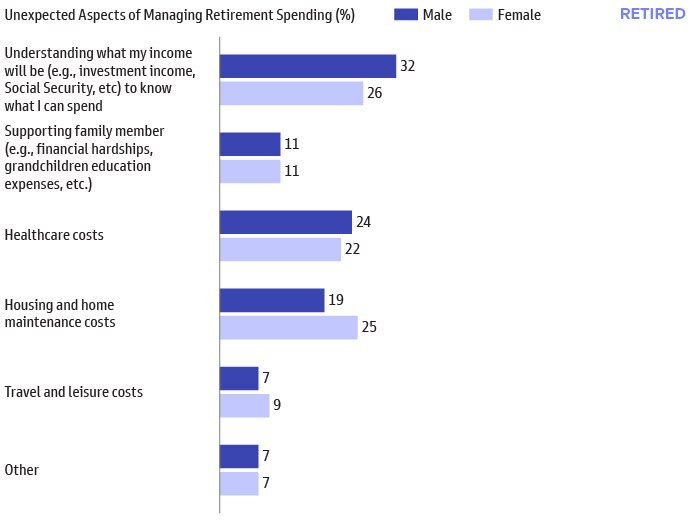

Furthermore, retirees state that the top unexpected challenge of managing their spending is the ability to understand what their income will be, so that they know how much they can spend.

Relative to what you anticipated or planned to be spending in retirement, do you spend more or less money on an annual basis in retirement?

What was the most unexpected aspect of managing your spending in retirement? (Select only one)

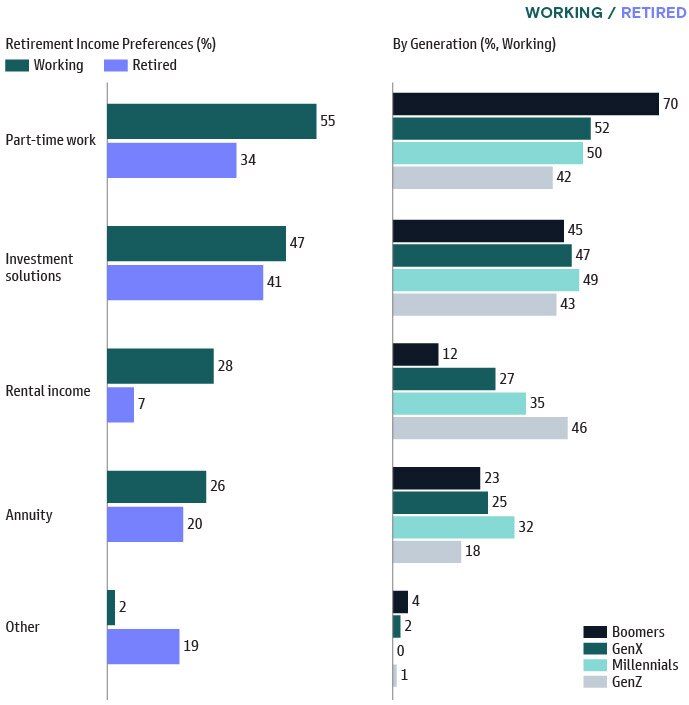

Part-Time Work Is the Preferred Source of Retirement Income

The concern with managing retirement income is evident in the preference of how to generate income. Part-time work rose considerably from last year to overtake investment solutions as the top source of preferred retirement income. However, because many people retire due to health-related issues, that’s not always a realistic solution. Still, the findings highlight the desire to stay involved in the workforce and preserve the option to earn additional income, even if supplemental.

There are also notable generational differences, with working Boomers preferring part-time work and Gen Z most interested in rental income.

In which of the following ways would you prefer to generate income during retirement? (Select all that apply)

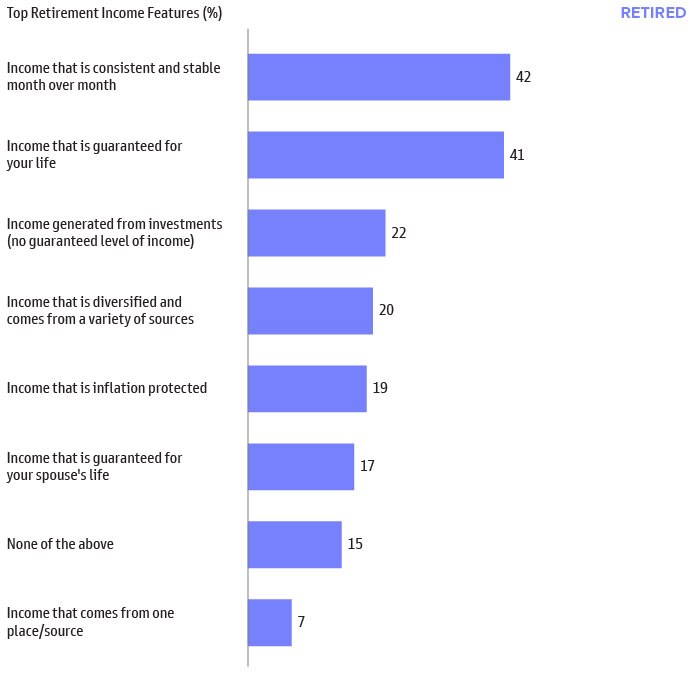

Top Valued Retirement Income Features

Building on the challenges of managing retirement income, retirees prefer income that is consistent and stable (42%), and income guaranteed for life as a close second (41%).

Given the environment, it may be surprising that inflation-protected income wasn’t valued higher, as we view this as a key concern for retirement income strategy.

The top preferences evidence a desire for simplicity in a retirement income strategy: dependable income that one cannot outlive.

What income features are most important to you (Beyond what you may receive from Social Security)? (Select up to three choices)

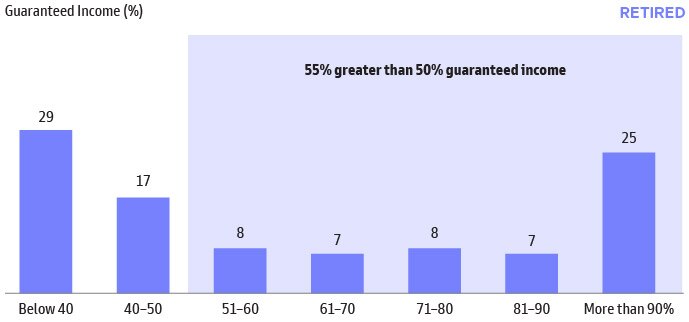

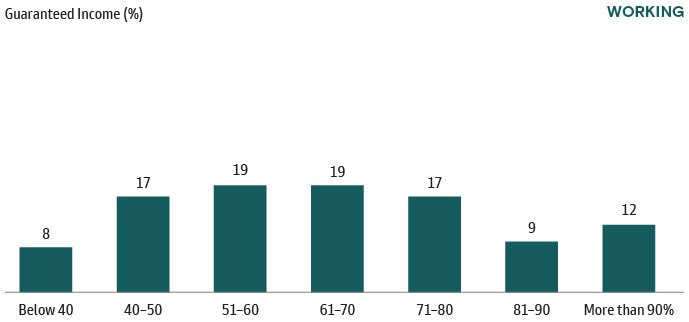

Respondents Seek a Wide Range of Guaranteed Income

A common question for retirees is how much guaranteed income should they have. On one hand, guaranteed income can simplify a retirement income strategy with less ongoing management. However, less guaranteed retirement income (and more in accumulated savings) can offer greater flexibility but require ongoing management. For our retired respondents, we see two polarizing and divergent groups: (i) below 40% guaranteed income and (ii) more than 90% guaranteed income.

When compared to our working respondents, they are more evenly distributed in the level of guaranteed income they desire for retirement, with most responses clustered between 41-80%.

This spectrum of responses highlights that there is no one-size fits all approach to guaranteed retirement income.

What percentage of retirement income do you receive from guaranteed sources (pension, Social Security or annuities)?

What percentage of retirement income do you want to receive from guaranteed sources (pension, Social Security or annuities)?

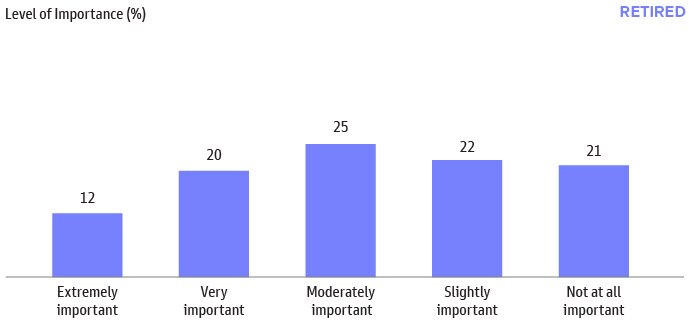

Nearly 80% of Retirees Believe Financial Help is Important to Manage Retirement Income

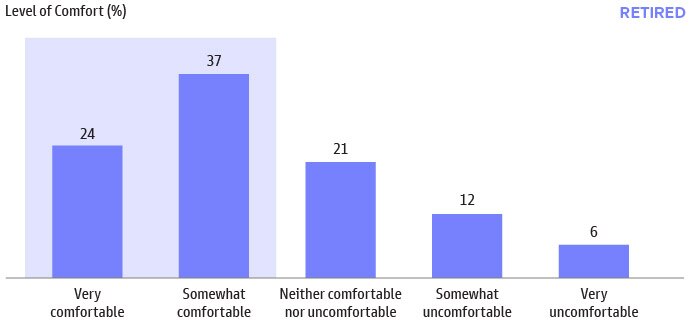

Despite the challenges in managing retirement income, most retirees (61%) feel comfortable managing their own income, and only 18% feel uncomfortable.

However, we still see a strong desire for financial help as 79% of retired respondents reported that financial help is either extremely, very, moderately, or slightly important to successfully manage one’s retirement income and investments.

How comfortable are you managing your retirement income needs?

How important is it to receive financial help (education, advice, counseling) to successfully manage your retirement income and investments?

Percentages may not add up to 100% due to rounding.

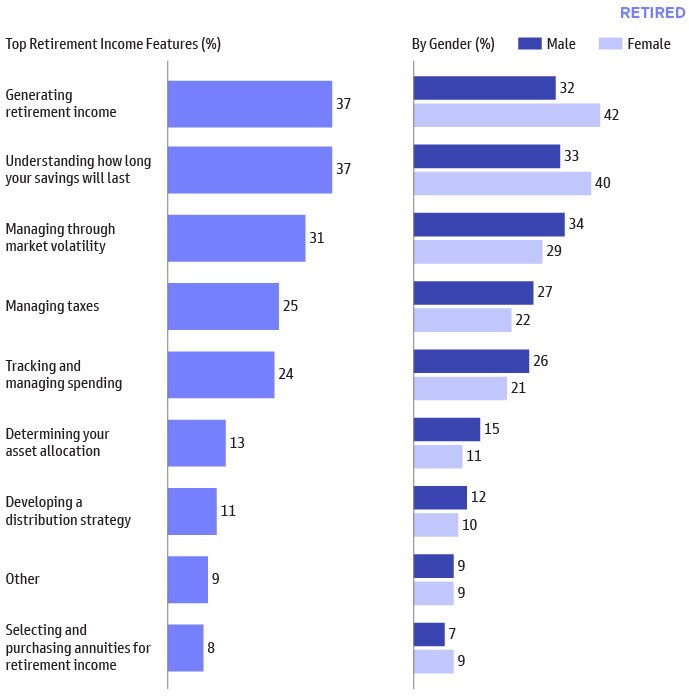

Top Challenges That Retirees Want Help With

Advice and guidance are growing in importance as individuals are forced to manage more financial decisions. Without pensions, retirees are managing income across a variety of accounts. When asked which challenges individuals need advice on to manage their retirement income successfully, generating retirement income and understanding how long your savings will last are the top challenges.

These concerns are more prevalent for retired women respondents seeking to manage retirement income.

What are the top challenges you face managing your retirement income and investments that you would like advice or guidance? (Select up to three choices)

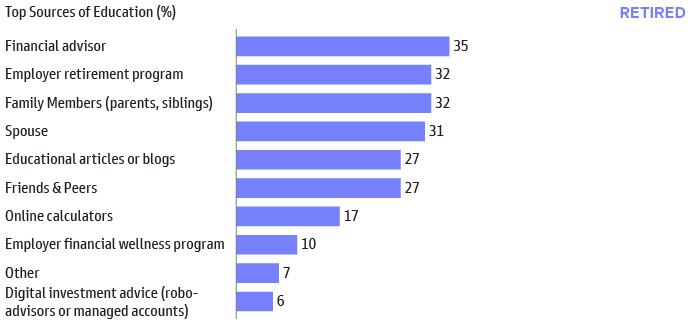

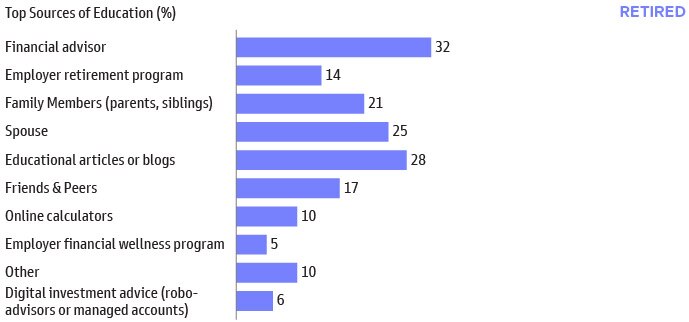

Financial Advisors Are the Top Source of Advice in Retirement

As retirement plan sponsors consider how to enhance their programs to incorporate retirement income features, it is important to acknowledge that while working respondents look to employer programs for education and advice, it is not the same for retirees. The employer retirement plan ranks sixth as a resource for education/advice in retirement, and the financial advisor is the top source instead.

For sponsors seeking to make their retirement plan a destination for retired employees to manage their savings to and through retirement, it appears that some existing plan designs could be falling short of retirees’ needs.

Which of the following would you say were the three most important sources of education and advice you relied upon as part of your retirement planning process? (Select up to three choices)

Since you have been retired, which of the following would you say are the most important sources of education and advice to help you manage your retirement income? (Select up to three choices)

Save a copy as a PDF

Retirement Survey & Insights Report 2022: Navigating the Financial Vortex

Start the Conversation

Committed to providing you with the insights you need to build your practice.