- No services available for your region.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsREINFORCING RETIREMENT READINESS

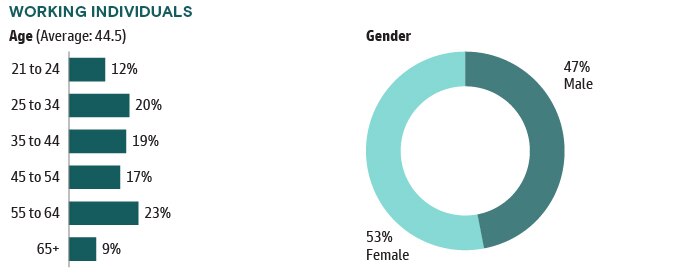

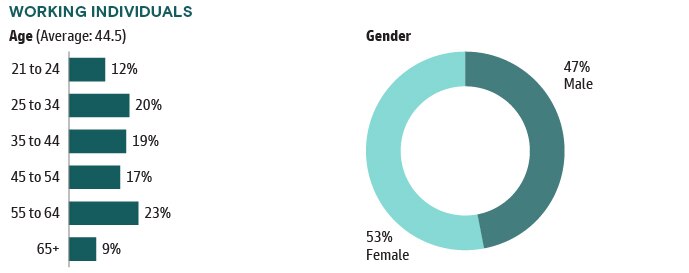

Are working individuals prepared to live a comfortable life in retirement? Unfortunately, we see from our retired respondents that many do not. And the data from our working respondents further suggests many are on the same path of falling behind on their savings, feeling stressed and working hard to navigate retirement savings obstacles.

The “financial vortex” refers to a myriad of financial priorities, life events, and planning assumptions, which often impact a working individual’s ability to contribute to their retirement savings. These competing financial needs were limited when Boomers were saving, but generations that have followed are forced to choose between retirement savings and other financial obligations.

Various factors impact one’s ability to save successfully, but having realistic expectations, knowing when to adjust your strategy to account for life events and applying conservative planning assumptions can be key steps in the right direction.

This section focuses on retirement planning needs for working individuals and highlights key factors such as the realities of retirement, top concerns and growing appetite for financial advice and education.

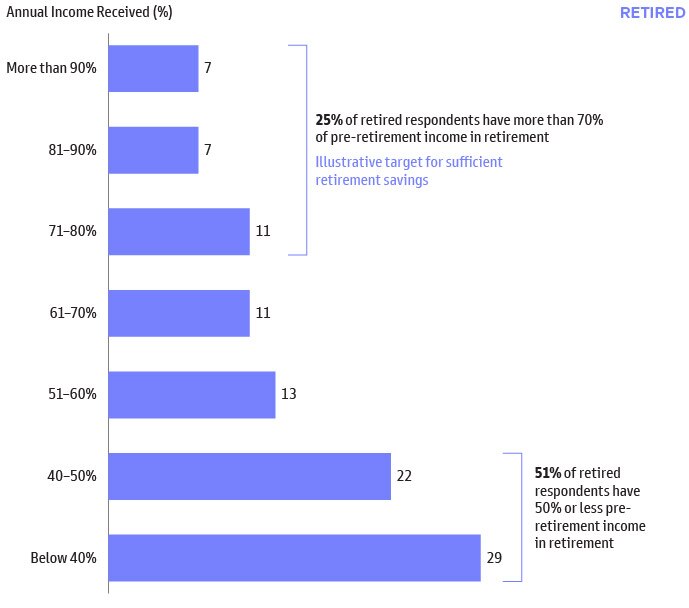

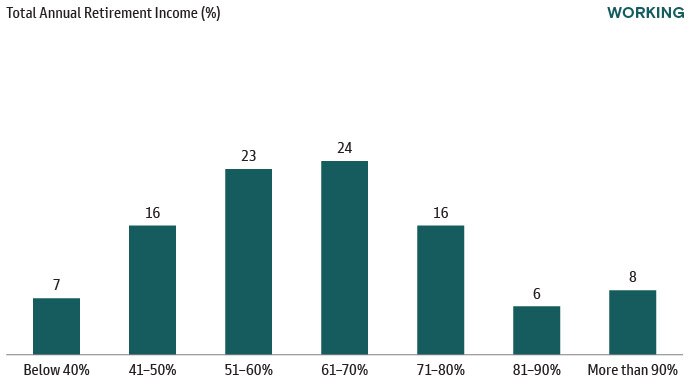

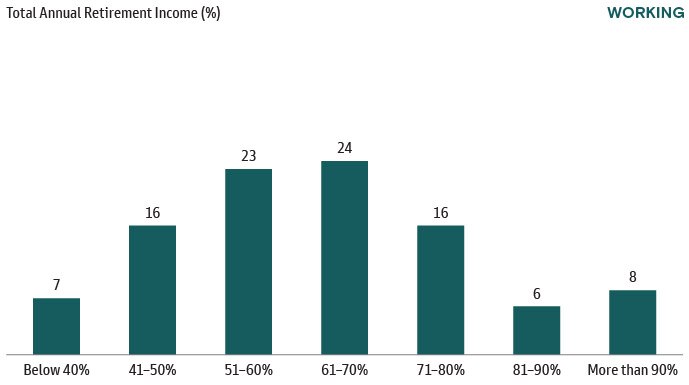

Reality Check for Working Individuals: Over Half of Retired Survey Respondents (51%) Receive Income Less than 50% of Their Pre-Retirement Income

As we explore the working population’s retirement readiness, it’s useful to consider responses from retirees as a benchmark for what workers might experience when they reach retirement.

When considering how well individuals are preparing for retirement, our first question is to understand whether retirees are successfully preparing to maintain their standard of living. Based on survey findings, that answer is no. Only 25% reach retirement with at least 70% pre-retirement income and more than half (51%) have less than 50% of their pre-retirement income.

How much total annual income do you receive in retirement (including Social Security) relative to your pre-retirement income (e.g., your final annual compensation prior to retirement, such as salary, bonus, etc.)?

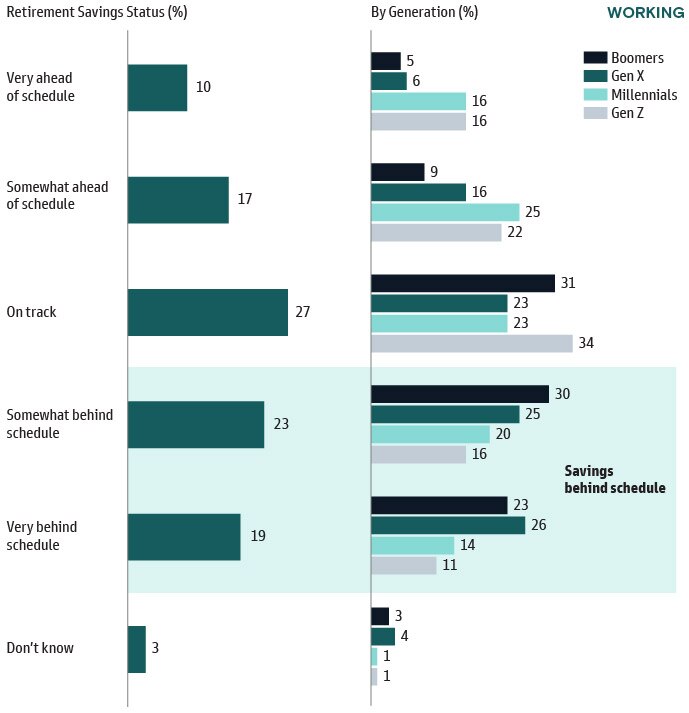

More than 40% of Working Respondents Believe Their Savings are Behind Schedule

Many workers today are on a similar trajectory of not having sufficient savings.

About four in ten working respondents feel their savings are behind schedule. Boomers and Gen X are the furthest behind and Millennials and Gen Z are most likely to report their savings are ahead of schedule.

The generational difference supports the notion that as one progresses through different stages of life and career, it may be difficult to keep savings on track. This is the “financial vortex” that can push retirement savers off course and impact so many savers.

Where would you say your retirement savings are at this moment?

Percentages may not add up to 100% due to rounding.

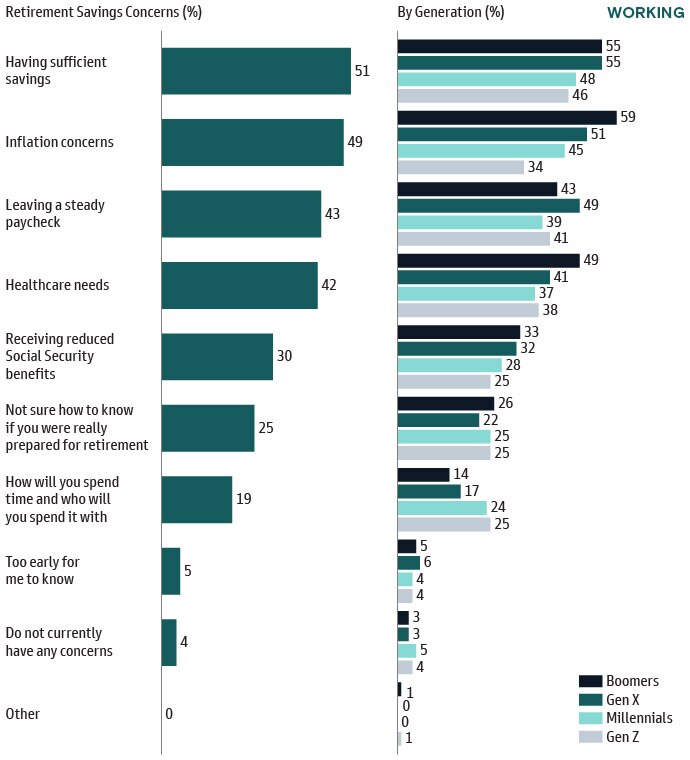

Workers’ Top Retirement Concerns: Having Sufficient Savings, Inflation and Leaving a Steady Paycheck

The top retirement concern for working respondents is having sufficient savings. Inflation is another factor that can drag savings behind over the course of one’s career. Rounding out the top three concerns is leaving behind a steady paycheck as people transition to retirement.

Unfortunately, the effects of inflation are not equally felt across wages, the stock market and cost of goods at the same time. So, individuals struggle to understand the impact on their savings and how to adjust to keep their savings on track.

Furthermore, inflation is a larger concern for those nearing retirement (Boomers and Gen X) because their accumulated savings will be impacted most. They worry if they have sufficient time to close the savings gap created by inflation.

What concerns, if any, do you have about preparing for retirement? (Select all that apply)

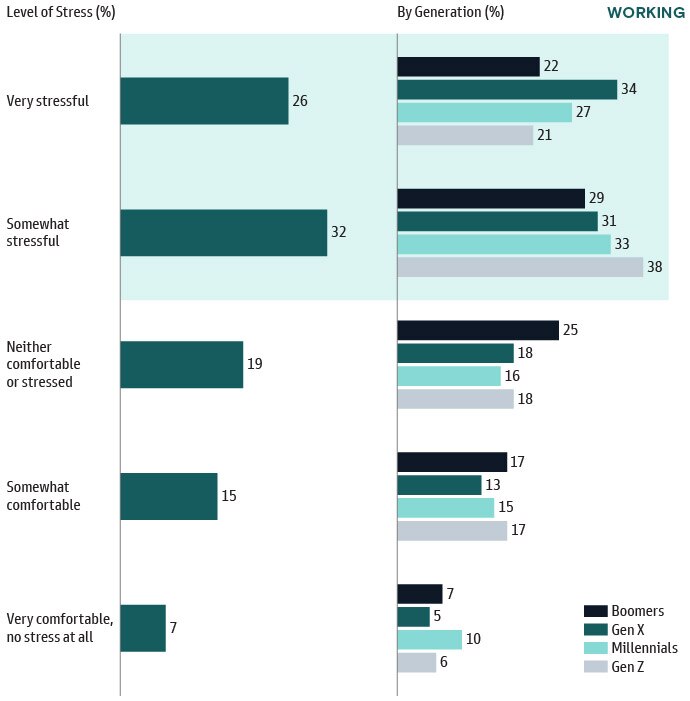

Financial Stress from Managing Retirement Savings

Financial stress felt by working respondents is another key factor in understanding how well individuals can manage their savings. Most respondents (58%) report feeling stressed about managing their retirement savings.

On a generational level, Gen X reports the highest levels of stress in managing their retirement savings. They are at a life stage with more challenging financial circumstances, in the critical years before retirement, and report feeling the highest levels of anxiety.

How much financial anxiety/stress do you feel managing your retirement savings?

Percentages may not add up to 100% due to rounding.

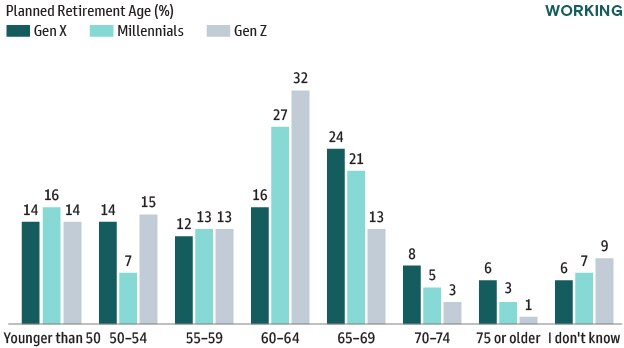

Workers May Underestimate Their Retirement Income Needs

Various factors impact one’s ability to save successfully but having realistic expectations and applying conservative planning assumptions can be a key step in the right direction.

Our findings indicate that nearly three quarters of working respondents plan for too little retirement income.

Similarly, the age of retirement can also impact overall savings. Planning for the realities of retirement can help an individual understand how much they need to accumulate and may offer motivation to save more while working.

How much total annual income do you anticipate needing entering retirement (including Social Security) relative to your pre-retirement income (e.g., your final annual compensation prior to retirement, such as salary, bonus, etc.)?

At what age are you planning to retire?

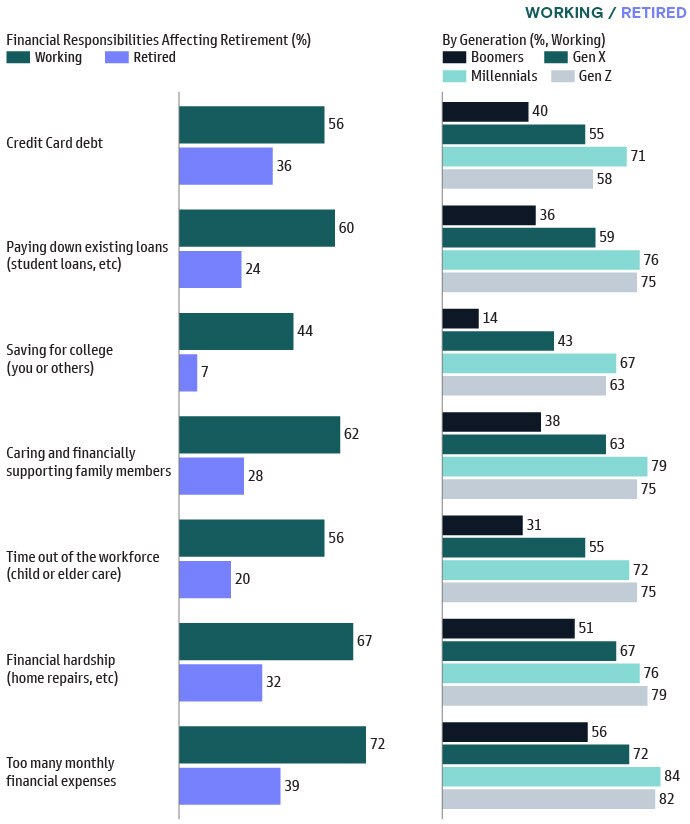

Competing Financial Responsibilities Have a Major Impact on the Ability to Save for Retirement

Competing financial priorities can significantly impact workers’ ability to save for retirement. Comparing working respondents to retired respondents, we can see how significantly saving for retirement has changed. Balancing these competing financial needs and evaluating the trade-offs is a key concern for savers.

Looking specifically at the generational impact, we further see how saving for retirement is complicated by managing other more immediate financial needs. Gen X was the first generation to significantly experience the challenge and now Millennials and Gen Z are feeling the largest impact.

How strongly did the below affect your ability to save for retirement? (Select from extremely, very, moderately, slight and did not affect)

Survey participants were asked to select responses based on what has extremely, very, moderately, slightly or no impact on their ability to save for retirement. We are reporting extremely, very and moderate responses.

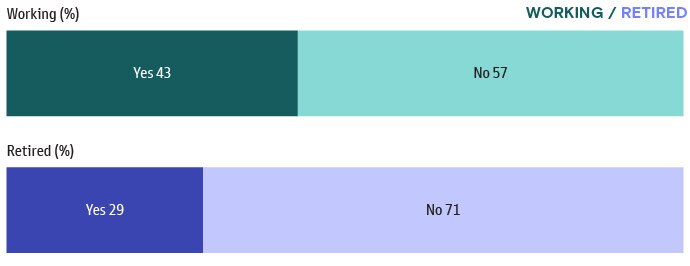

Working Respondents are More Likely to Take Time Away from the Workforce to Provide Care

Caregiving is a significant challenge coming out of the COVID-19 pandemic, but more broadly, we see the trend across retired and working populations.

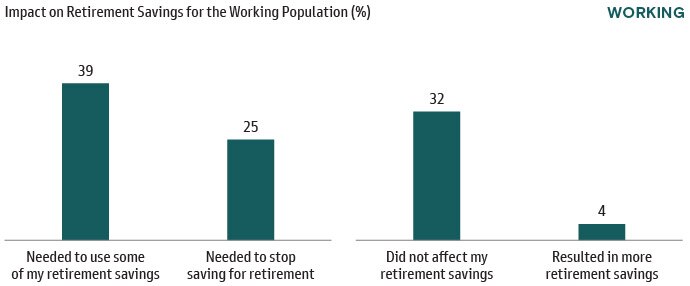

According to the survey’s findings, 43% of working respondents have reported needing to take time away from work (up from 29% for retired respondents). As a result, in the bottom chart, 64% have reported needing to either stop saving or access their retirement savings during this period.

Since most retirement plans are offered through an employer, when people are caregiving and not working, they no longer have access to a retirement plan, making savings more difficult.

This can cause many to fall behind on their retirement savings.

Have you ever needed to take time away from the workforce to provide care for a family member?

What effect did taking time away from the workforce have on your retirement savings?

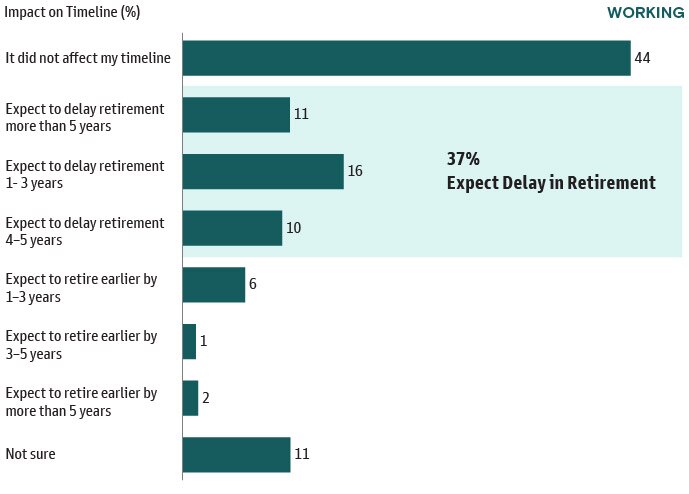

The Effect of COVID-19 on Retirement Savings

The COVID-19 pandemic has been a unique global event with a wide range of financial impacts. That impact obviously increased for those who lost a source of income.

A quarter of working respondents needed to withdraw money from their 401(k) plan to cover immediate expenses, taking advantage of the one-time opportunity to access their retirement savings while not yet retired. The majority of those impacted (70%) state they plan to repay their 401(k) plan account.

Thirty-seven percent of working respondents expect to delay retirement because of the effects of the pandemic on their finances. One in five (21%) believe they will need to delay retirement by four or more years.

While the pandemic had wide-spread impact, it also provides insight into how impactful losing a job can be on one’s finances. These events are much more common and can meaningfully push retirement savings behind schedule.

During the pandemic, did you withdraw money from your 401(k) without penalty to cover immediate expenses?

How, if at all, did COVID-19 affect your expected retirement timeline?

Percentages may not add up to 100% due to rounding.

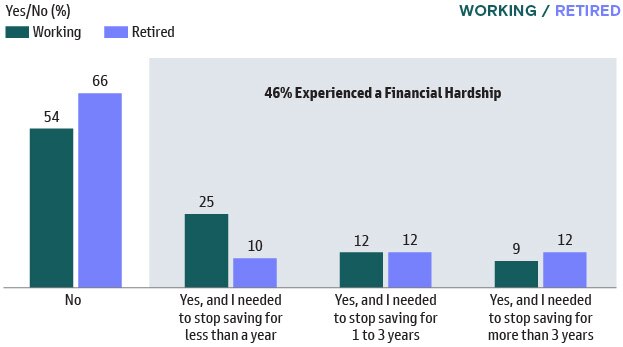

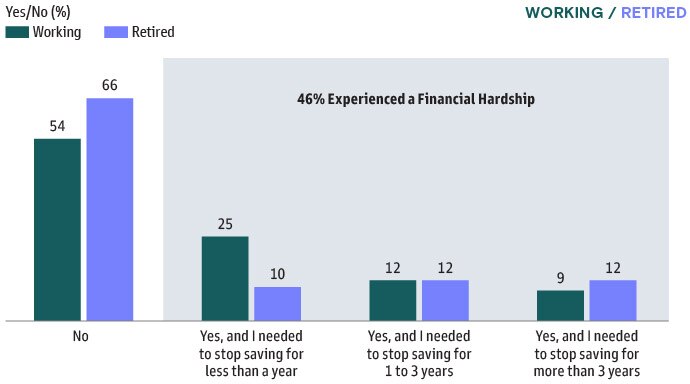

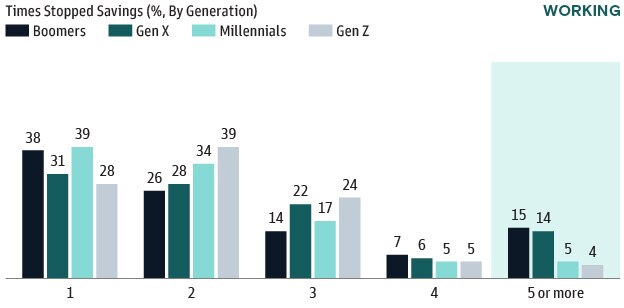

Financial Hardships Increase among Working Respondents

Those in the retirement industry often think of financial hardships as specific situations that allow individuals to take in-service distributions from their 401(k) plan. However, individuals experience hardships of all types.

Financial hardship is a growing trend with 46% of working respondents facing some type of challenge that causes them to stop saving for retirement.

This is another example of how the “financial vortex” can impact retirement preparation.

The bottom chart details how each generation has paused savings for retirement due to financial hardship.

While the majority of those impacted stopped saving once or twice in their career, we also see a generational divide when comparing the younger generations to Boomers and Gen X, both of which are further along in their career are more likely to report having stopped savings five or

more times.

Have you experienced a financial hardship that caused you to stop saving directly for retirement (e.g., in your 401(k))?

How many times do you recall needing to stop saving for retirement because of a financial hardship or other financial needs (e.g., paying for a child’s college)?

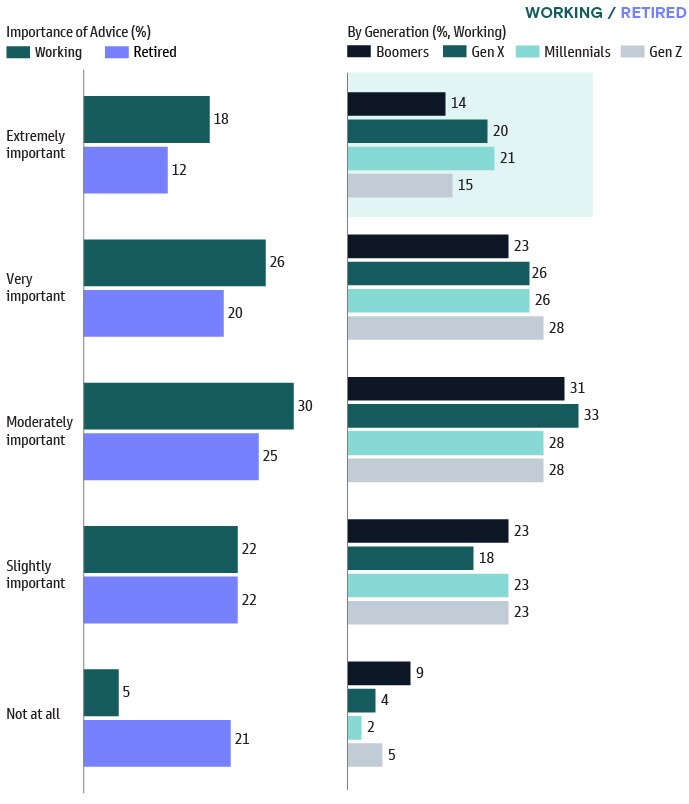

Growing Appetite for Financial Help

Given the complexity and financial uncertainty of retirement, it is understandable that 95% of working individuals state receiving financial help is important to successfully manage their retirement savings.

Overall, working respondents value financial help more than retiree respondents.

Looking across the generations, financial help is valued by almost all respondents; however, those in the primary saving years (Gen X and Millennials) are most likely to state that financial help is extremely important.

How important is it to receive financial help (education, advice, counseling) to successfully manage your retirement savings/income and investments?

Percentages may not add up to 100% due to rounding.

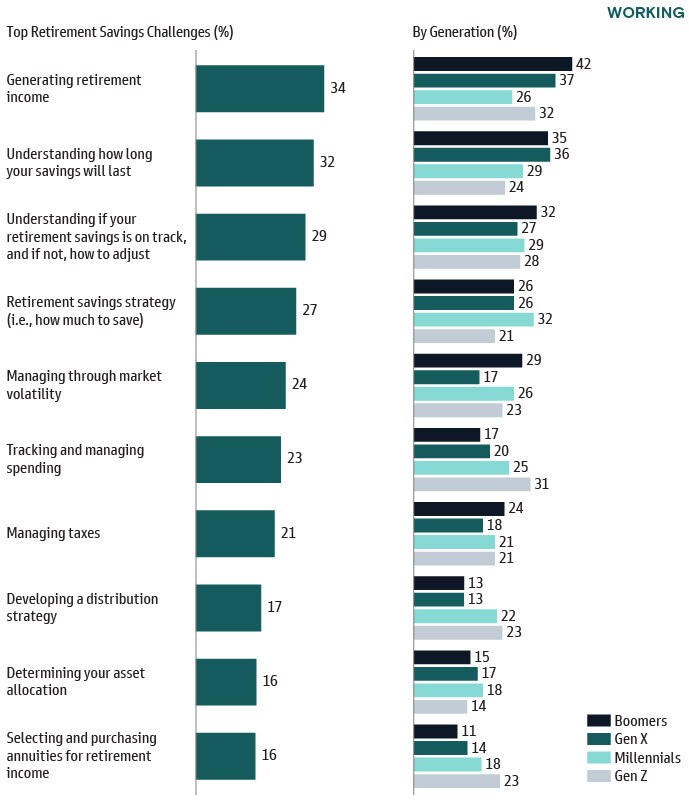

Workers Want Help in Generating Retirement Income

While there are a variety of supporting tools and resources available to retirement savers (e.g., calculators, asset allocation models), generating retirement income is the top challenge for working respondents. This highlights how individuals are focused on how their retirement savings will translate to retirement income.

At the generational level, the challenge of generating retirement income was most predominantly felt by Boomers (42%) and Gen X respondents (37%).

For Millennials, establishing a retirement savings strategy (e.g., how much to save) was the top challenge (32%).

For Gen Z, generating retirement income (32%) and tracking and managing spending (31%) were top challenges.

What are the top challenges you face managing your retirement savings and investments where you would like advice/guidance? (Select up to three choices)

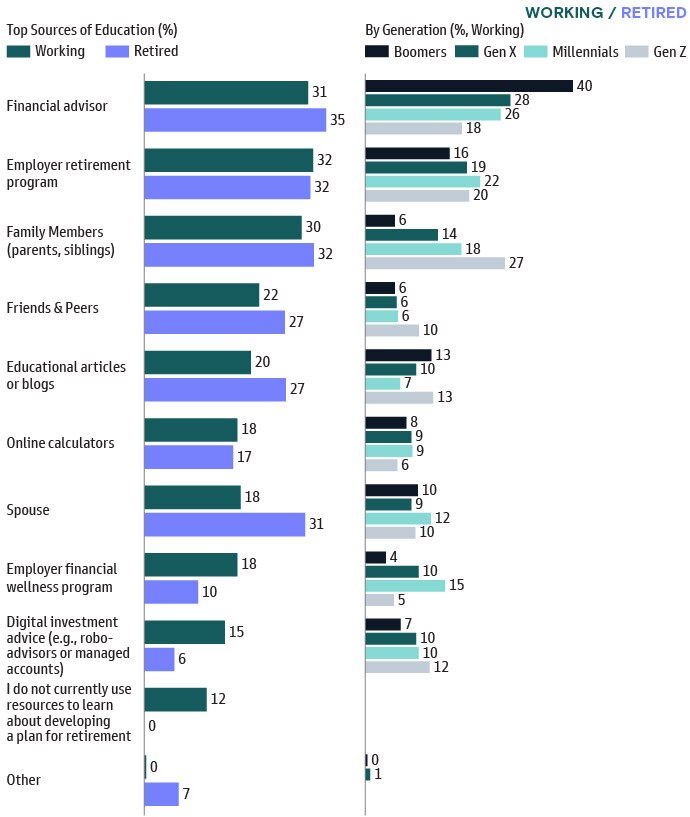

Top Sources of Help and Advice for Workers

Employer-sponsored retirement programs continue to be a critical source of education and advice that workers rely upon.

Workers also report financial advisors, and family members as top sources of education.

Notably, as we look across the generations, Boomers and Gen X respondents feel that financial advisors are their most important source of advice.

Which of the following sources of education and advice do you currently leverage to learn about developing a plan for retirement? (Select up to three choices)

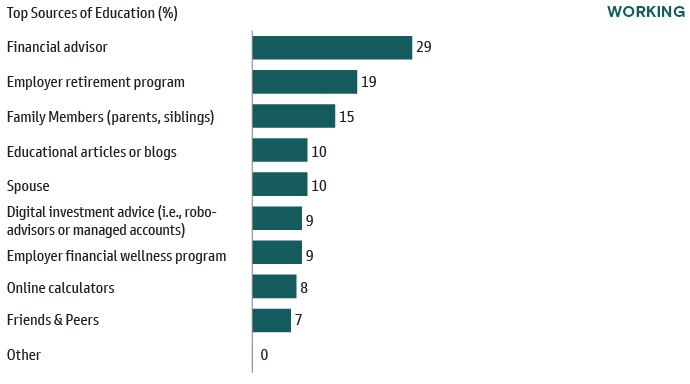

Financial Advisors Are Viewed as the Most Important Source of Education and Advice

While there are a variety of sources individuals use to prepare and educate themselves, financial advisors are viewed as top source of education and advice (29%).

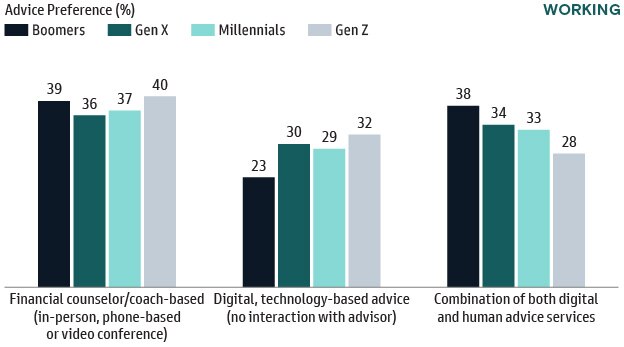

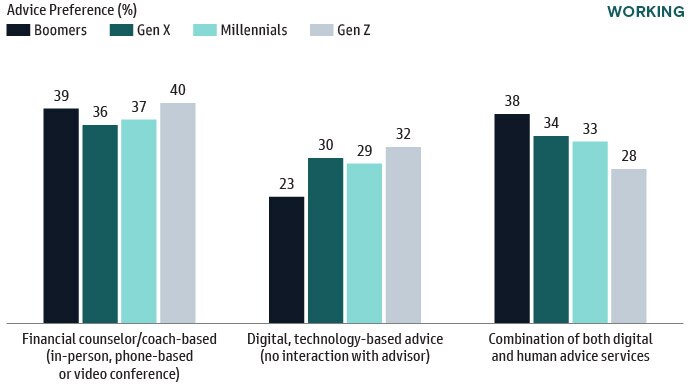

Working respondents are roughly split between how to receive financial advice: human-based advice, digital advice or a combination of both. As needs and preferences differ among individuals, offering a multi-channel sources of education can better align to how people seek their advice.

Which of the following sources of education and advice do you feel is the most important in preparing for retirement? (Select all that apply)

How do you prefer to receive financial advice and guidance? By Generation (Select only one)

Percentages may not add up to 100% due to rounding.

Save a copy as a PDF

Retirement Survey & Insights Report 2022: Navigating the Financial Vortex

Start the Conversation

Committed to providing you with the insights you need to build your practice.