Glossary

Bps or basis point, a basis point is 1/100th of a percent

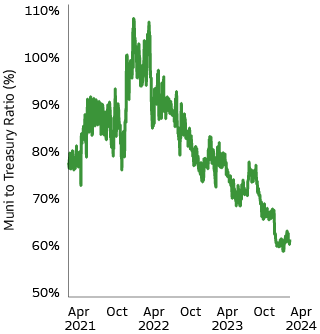

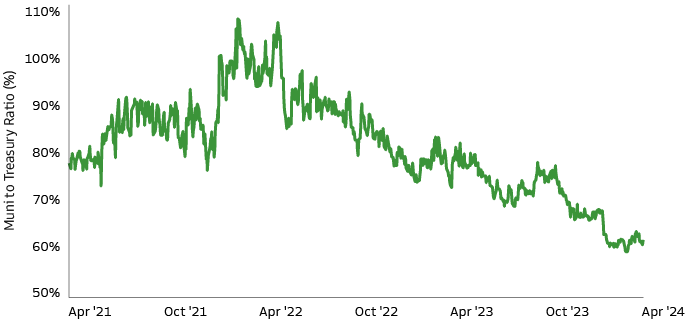

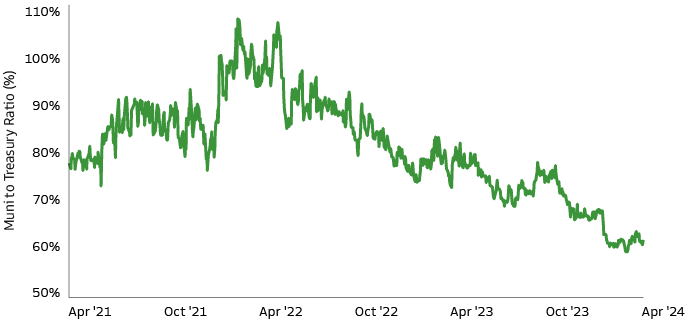

Municipal/Treasury ratio is a comparison of the current yield of Municipal bond to US treasuries. It aims to measure whether or not Municipal bonds are an attractive investment in comparison.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the portfolio will achieve similar results. The index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein.

Portfolios and benchmarks are not rated by an independent ratings agency. Goldman Sachs Asset Management may receive credit quality ratings on the underlying securities of portfolios and their respective benchmarks from the three major rating agencies: Standard & Poor’s, Moody’s and Fitch. Goldman Sachs Asset Management calculates the credit quality breakdown and overall rating for both portfolios and their respective benchmarks according to the client’s preferred method or such other method as selected by Goldman Sachs Asset Management in its sole discretion. The applicable method may differ from the method independently used by benchmark providers. Securities that are not rated by all three agencies are reflected as such in the breakdown. For illustrative purposes, Goldman Sachs Asset Management converts all ratings to the equivalent S&P major rating category when reporting the credit rating breakdown. Ratings and portfolio credit quality may change over time. Unrated securities do not necessarily indicate low quality, and for such securities the investment adviser will evaluate the credit quality.

Municipal 3yr: Bloomberg Municipal 3 Year Index

The Bloomberg Municipal Bond Index is a rules-based, market-value- weighted index engineered for the long-term tax-exempt bond market. To be included in the index, bonds must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody's, S&P, Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment-grade. They must have an outstanding par value of at least $7 million and be issued as part of a transaction of at least $75 million. The bonds must be fixed rate, have a dated-date after December 31, 1990, and must be at least one year from their maturity date. Remarketed issues, taxable Municipal bonds, bonds with floating rates, and derivatives, are excluded from the benchmark. This index is the 3 Year (2-4) component of the Municipal Bond index.

Municipal 1-10yr Blend: Bloomberg Municipal 1-10 Yr Blend Index

The Bloomberg Municipal Bond 1-10 Year Blend Index is a market value- weighted index which covers the short and intermediate components of the Bloomberg Municipal Bond Index, an unmanaged, market value- weighted index which covers the U.S. investment-grade tax-exempt bond market. The Bloomberg Municipal Bond 1-10 Year Blend Index tracks tax-exempt Municipal General Obligation, Revenue, Insured, and Prerefunded bonds with a minimum $5 million par amount outstanding, issued as part of a transaction of at least $50 million, and with a remaining maturity from 1 up to (but not including) 12 years. The index includes reinvestment of income.

Municipal Aggregate: Bloomberg Aggregate Municipal

The Bloomberg Municipal Bond Index is a rules-based, market-value- weighted index Index engineered for the long-term tax-exempt bond market. To be included in the index, bonds must be rated investment- grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody's, S&P, Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment- grade. They must have an outstanding par value of at least $7 million and be issued as part of a transaction of at least $75 million. The bonds must be fixed rate, have a dated-date after December 31, 1990, and must be at least one year from their maturity date. Remarketed issues, taxable Municipal bonds, bonds with floating rates, and derivatives, are excluded from the benchmark.

Municipal High Yield: Bloomberg High Yield Municipal Index

The Bloomberg Municipal High Yield Bond Index is an unmanaged index made up of bonds that are non-investment grade, unrated, or rated below Ba1 by Moody's Investors Service with a remaining maturity of at least one year. The Index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

Risk Considerations

Income from Municipal securities is generally free from federal taxes and state taxes for residents of the issuing state. While the interest income is tax-free, capital gains, if any will be subject to taxes. Income for some investors may be subject to the federal Alternative Minimum Tax (AMT). All investments contain risk and may lose value. Investing in the bond market is subject to certain risks, including market, interest rate, issuer, credit and inflation risk.

Municipal securities are subject to credit/default risk and interest rate risk and may be more sensitive to adverse economic, business, political, environmental, or other developments if it invests a substantial portion of its assets in the bonds of similar projects or in particular types of municipal securities. While interest earned on municipal securities is generally not subject to federal tax, any interest earned on taxable municipal securities is fully taxable at the federal level and may be subject to tax at the state level.

When interest rates increase, fixed income securities will generally decline in value. Fluctuations in interest rates may also affect the yield and liquidity of fixed income securities.

High-yield, lower-rated securities involve greater price volatility and present greater credit risks than higher-rated fixed income securities.

General Fixed Income Disclosure

Investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity, interest rate, prepayment and extension risk. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. The value of securities with variable and floating interest rates are generally less sensitive to interest rate changes than securities with fixed interest rates. Variable and floating rate securities may decline in value if interest rates do not move as expected. Conversely, variable and floating rate securities will not generally rise in value if market interest rates decline. Credit risk is the risk that an issuer will default on payments of interest and principal. Credit risk is higher when investing in high yield bonds, also known as junk bonds. Prepayment risk is the risk that the issuer of a security may pay off principal more quickly than originally anticipated. Extension risk is the risk that the issuer of a security may pay off principal more slowly than originally anticipated. All fixed income investments may be worth less than their original cost upon redemption or maturity.

General Disclosures

United States: In the United States, this material is offered by and has been approved by Goldman Sachs Asset Management, L.P., which is a registered investment adviser with the Securities and Exchange Commission.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

This material is provided at your request for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Portfolios and benchmarks are not rated by an independent ratings agency. GSAM may receive credit quality ratings on the underlying securities of portfolios and their respective benchmarks from the three major rating agencies: Standard & Poor’s, Moody’s and Fitch. GSAM calculates the credit quality breakdown and overall rating for both portfolios and their respective benchmarks according to the client’s preferred method or such other method as selected by GSAM in its sole discretion. The applicable method may differ from the method independently used by benchmark providers. Securities that are not rated by all three agencies are reflected as such in the breakdown. For illustrative purposes, GSAM converts all ratings to the equivalent S&P major rating category when reporting the credit rating breakdown. Ratings and portfolio credit quality may change over time. Unrated securities do not necessarily indicate low quality, and for such securities the investment adviser will evaluate the credit quality.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of April 24th, 2024 and may be subject to change, they should not be construed as investment advice.

Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Goldman Sachs does not provide legal, tax or accounting advice, unless explicitly agreed between you and Goldman Sachs (generally through certain services offered only to clients of Private Wealth Management). Any statement contained in this presentation concerning U.S. tax matters is not intended or written to be used and cannot be used for the purpose of avoiding penalties imposed on the relevant taxpayer. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you may disclose to any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be aware that a determination of the tax consequences to them should take into account their specific circumstances and that the tax law is subject to change in the future or retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

Date of First Use: 4/24/24. 372170-OTU-2034115