October 31, 2023 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact Us

Jim GarmanGlobal Head of Real Estate Jim Garman |

Kristin KuneyGlobal Co-Head of Liquid Real Assets Kristin Kuney |

Marco WillnerCo-Head of Dynamic Asset Allocation, Multi-Asset Solutions Marco Willner |

Commercial real estate (CRE) continues to adapt to a new paradigm. Interest rates are higher, fundamentals are softer, and the market can no longer rely on a wave of fresh capital. Shifting work and spending habits are also driving supply and demand imbalances. The US office market has been the subject of intense investor focus recently—an area we explored in Commercial Real Estate: Into the Headwinds. Outside of US office real estate, sharp divergences have emerged between asset types across regions. Opportunities are emerging due to mismatches between property prices and potential long-term value, as well as the evolution of technology, demographics, and sustainability megatrends. We think assets at this intersection stand to benefit, while those that are not will likely have a less positive fate. Not all property is created equal, and we think a one-size-fits-all investment approach loses sight of important nuances.

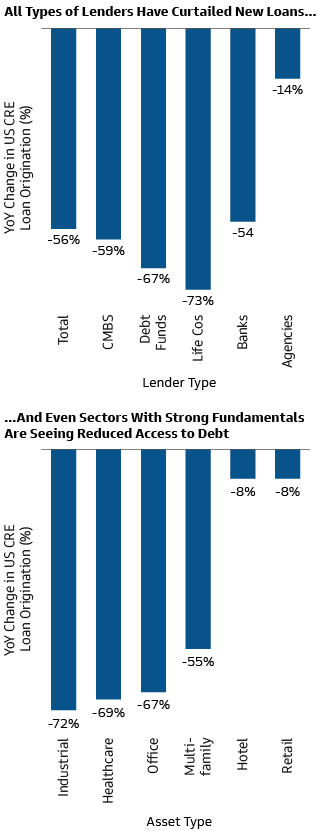

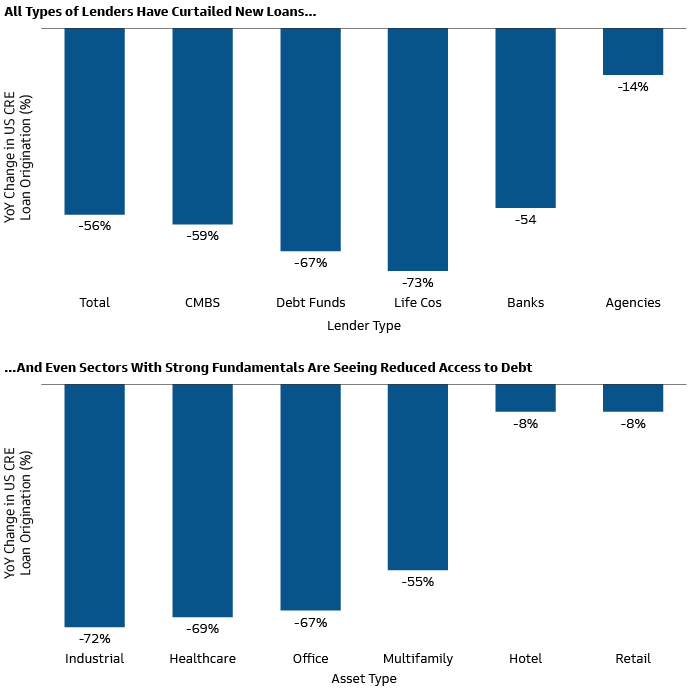

With real estate assets in the process of repricing, and with a more than $2 trillion wall of maturities over the next three years likely to force more revaluations, it’s unsurprising that some investors remain cautious about their real estate allocations. CRE deal activity—a critical metric of the sector’s overall health and liquidity—has continued to grind slower throughout 2023 due to challenged fundamentals and the higher cost and lower availability of credit. The slowdown is widespread. In 2Q 2023, not one of the top 10 largest CRE markets and none of the major sectors recorded an increase in investment activity versus the same period 12 months ago.1

Source: Mortgage Bankers Association Quarterly Survey of Commercial/Multifamily Mortgage Bankers Originations 1Q 2023. Above graphs represent percent change in volume of commercial and multifamily loan origination, 1Q23 vs. 1Q22.

The balance of distress in the US—encompassing financially troubled assets and assets taken back by lenders—rose to $71.8 billion at mid-year, marking the fourth consecutive quarterly increase. In Europe, CRE acquisitions across all sectors fell to their lowest level since 2010. Activity in Asia continues to be undermined by China’s property market, which is undergoing its own significant downward adjustment. Sentiment toward Hong Kong CRE has also suffered. Japan—much like its economy—has been an outlier; activity has held up relatively well, helped by domestic macroeconomic strength.

Any recovery in CRE market activity or capital values is likely to be uneven across regions, and we are seeing divergence in fortunes between prime versus secondary-quality assets across all areas.

The office sector remains in focus given its widespread reliance on debt and bank financing, and the shift to hybrid working. Many occupiers are curbing leasing activity, downsizing staffing and delaying decision making. However, a flight-to-quality trend is boosting prime office rents as tenants seek space in the best buildings in prime locations.

In the US, only 10% of all office buildings accounted for 80% of the occupancy losses between 1Q 2020 and 4Q 2022. These were mostly older buildings in downtown submarkets with relatively high crime rates and few surrounding amenities.2 Urban hubs of Chicago and New York remain among the top office markets in terms of rent growth forecasts, while San Francisco continues to lag due to the combined impact of tech industry cuts and workers moving out of the city. While many of the headlines are concentrated on the fates of major cities with well-established real estate markets, much of the recent growth and opportunity in the US has been coming in less-developed metros and cities between the coasts.

In Europe, although fewer leases are occurring for large blocks of office space in major cities, rent growth for top-quality space in cities including London and Paris is being supported by relatively low availability.3 Return-to-office rates were generally higher in Asia than in North America and Europe in 1H 2023, which has made select markets with higher levels of office-based working, like Seoul, Singapore, and Tokyo, relatively more attractive for investors. Future growth locations for office real estate may depend on factors such as GDP growth, working age populations, and access to highly-skilled workers.

Sustainability is also creating winners and losers across regions and property types, including offices. Tenants increasingly want their spaces to represent their values and they’re willing to pay the premium for green buildings. Many corporate users of office space have committed to carbon neutrality goals; they need their real estate to be consistent with that. The extent of a “green premium” varies across different markets, with studies showing a broad trend among occupiers across regions willing to pay higher rents for space in buildings with sustainability certifications, like Leadership in Energy and Environmental Design (LEED).4 Other evidence suggests a trend for a “brown discount” on properties with relatively weaker environmental performance. While the return premium that can be earned from green buildings is an evolving science, we think the trend will be pervasive across all regions over the long-term, with Europe leading the way.

Retail is another CRE segment enduring significant disruption, largely due to the rise of e-commerce and pandemic-related rent losses. The resumption of international tourism and resilient consumer balance sheets have provided some confidence to occupiers. Foot traffic near stores in major cities globally has also risen again but remains on average 10-20% lower across metropolitan areas than it was before the pandemic—when people come to the office less often, they shop less often. Again, trends vary by location. For instance, studies suggest online spending as a share of retail spending is lower in Japan compared to China, France, Germany, the UK, and the US.5 This may be a result of the country’s higher office attendance rates.

In the US, analysis shows many retailers have shifted their strategies and are beginning to focus their expansion plans outside of traditional urban cores. This has implications for the types of retail assets that will be desirable, as suburban areas have different needs and structures. Grocery stores as anchor tenants, for example, have become increasingly important. The potential for mixed-use has also expanded, as many suburban areas are recognizing the need for additional multifamily housing.6

Data suggests physical stores will remain at the forefront of sales strategies, but their role will continue to evolve to serve omnichannel retail (i.e., a combination of brick-and-mortar and online). More stores may also become comprehensive customer experiences hubs, rather than purely transaction venues. We believe developers of retail space should keep adaptability in mind. For investors, prime assets with high levels of foot traffic leased by tenants with sales channels that satisfy customers who want a firsthand shopping experience may emerge as long-term winners. Some assets that fall into this category may also surprise to the upside in the months ahead on rent growth and yield, given yields entered the current repricing cycle at a higher level. Therefore, cap rate expansion—the market's way of saying that the risk of purchasing CRE assets is rising—could be lower.

While the challenges for parts of the office and retail sectors are significant, certain CRE sub-sectors driven by secular growth trends may prove more resilient in an environment of elevated inflation and higher-for-longer rates. Data centers and industrial warehouses continue to attract capital, for instance. We think these new economy sectors are likely to benefit from long-term technology innovation and e-commerce trends. Other buildings on the right side of demographic changes, such as senior and student housing, may also carry pricing power and look increasingly appealing to investors in a new macroeconomic regime.

The international emergence of 5G networks, blockchain, cloud computing and rapid growth of data are immense catalysts for technology real estate, including modern industrial facilities, towers that transport data and data centers to store it. Artificial intelligence—along with streaming, gaming, and self-driving cars—also has the potential to upend the market for tangible real assets as natural language processing tools work their way into businesses and society. Data centers—which accounted for 8.8% of equity market capitalization of the FTSE Nareit All Equity Index as of June 30, 2023—have shown resilience compared with other CRE sectors.7 Enormous growth in data center supply since early 2022 has been met with strong demand, particularly from large corporations finding it difficult to secure enough capacity.8 While data centers are currently viewed as broadly attractive, ongoing success is predicated on being able to meet the technology needs of the future. Many assets are ill equipped and will need to adapt and enhance power, space, and cooling requirements as AI and automation take hold.

E-commerce is driving robust industrial & logistics property demand, but economic uncertainty, labor shortages and realigned supply chains are impacting occupier sentiment and decision making. Occupiers are willing to pay a premium for modern warehouses and we expect new assets that facilitate quick movement of goods to consumers through use of automation and robotics will perform better than traditional warehouses. E-commerce retail occupiers account for between 35-40% of industrial demand and require 2-3x more space than traditional brick-and-mortar retailers. Higher demand for warehouse space can have ripple effects into other industries, including housing and office buildings supporting operations and employees. A trend towards onshoring of supply chains is—and will likely continue to be—an additional driver of demand for select industrial markets. Investors who recognize these evolutions quickly can potentially gain an early-mover advantage in a space where being first can mean building a high hurdle to competition by getting quality assets in the best locations.

While specialized “new economy” assets may present compelling opportunities, they also carry different risk and return profiles. Rather than rely on CRE labels, we think investors are better served to focus on the underlying fundamentals of the assets. Conducting rigorous analysis of capital structures and cashflows to identify potential opportunities and risks is critical, especially after an era of ultra-loose policy and cheap capital that spurred a rapid run-up in property valuations during and directly after the pandemic. Many real estate companies have taken actions since the end of 2022 to preserve cash and strengthen balance sheets, but additional actions such as equity injections, or in some cases asset disposals at significant discounts, may be necessary. From a public credit perspective, we advocate for issuer selection and prefer high-quality names with lower refinancing needs. Meanwhile, as capital structures adjust, we see opportunities for private credit to fill the void left by traditional CRE lenders, particularly for high-quality assets and sectors.

We believe it is also important to recognize the geographical expansion of the listed real estate investment trust (REIT) market. This growth is creating more investment opportunities around the globe, often in property types that capture secular growth trends, like data centers, towers, and self-storage. Although the US remains the largest listed real estate market, more than 40 countries have now adopted the REIT tax structure. As of 1H 2023, there are approximately 304 listed REITs globally in developed markets, with ~60% of REITs by count sitting outside of the US (~40% by market cap). Much of the REIT expansion in recent years has been concentrated in Asia, with momentum building in markets like Singapore and Japan, presenting attractive opportunities for growth. The Middle East also has demonstrated growth in recent years with the addition of REITs in Saudi Arabia and Oman. Alongside global REIT growth, there is an expanding universe of private market real asset strategies for investors to consider. Many of these strategies allow for more efficient matching between cost of capital and risk/return appetites via a range of core, value-add and opportunistic CRE assets exposed to long-term secular themes.

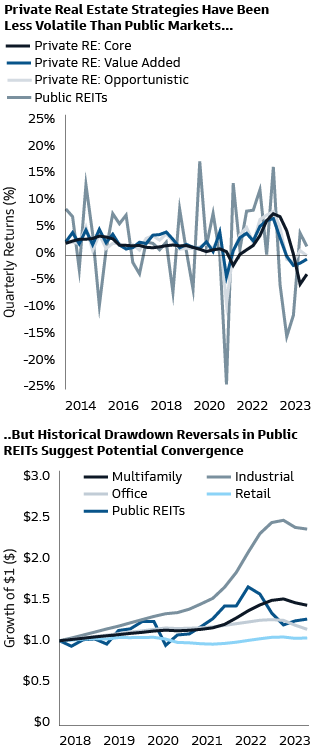

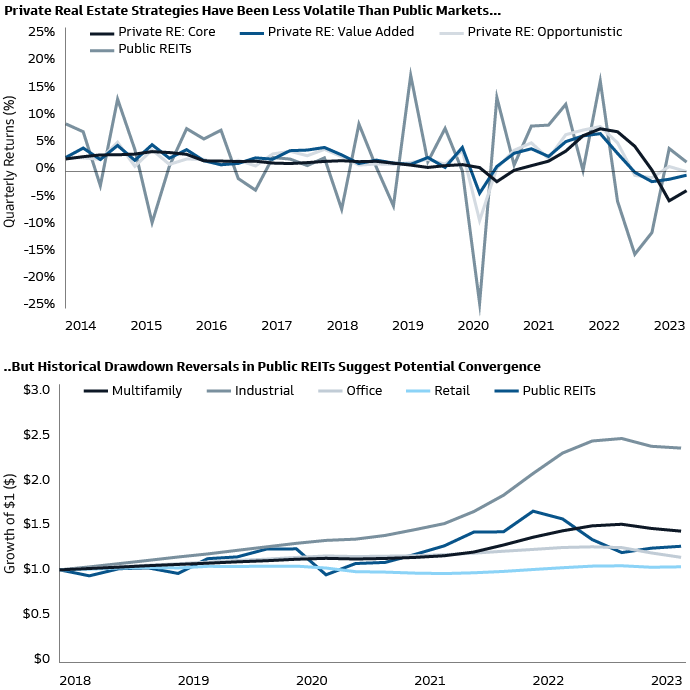

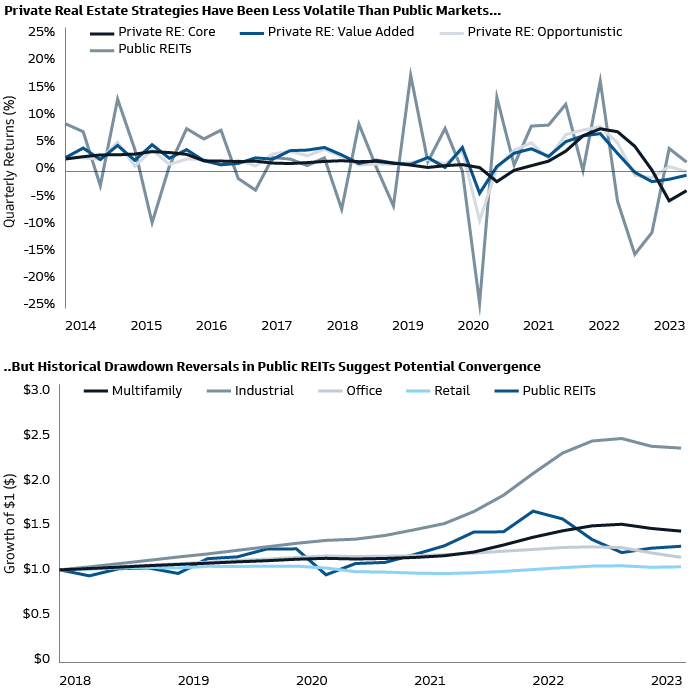

Public REITs began to price in higher interest rates and slower growth in the spring of 2022. In the US, listed REITs valuations are down 29% from the peak, while the developed Europe index, which covers the euro area and the UK, has corrected by 42%. We believe the larger decline in Europe is justified by the CRE sector composition of fewer new economy constituents (e.g., data centers) and a weaker economic growth outlook, which implies lower net operating income (NOI) growth. Markdowns in the private space have been far more muted, although year-to-date private CRE has underperformed public markets by ~9%, with the US slightly ahead of the UK and Europe in terms of valuation adjustments. With the dearth of transactions in recent quarters, some investors are beginning to question how long the public vs. private valuation gap can be sustained. This mismatch is underscored by headlines about redemption limits being reached in semi-liquid vehicles, which has led to more scrutiny of the valuations of underlying positions in private funds.9

Source: Top chart: FTSE Nareit US All Equity REITs Index, NCREIF NFI-ODCE, Cambridge Associates, as of March 31, 2023. Bottom chart: FTSE Nareit US All Equity REITs Index, NCREIF NPI, as of June 30, 2023.

Part of the friction may be that owners of under-performing assets have few options, given current pricing and capital market dynamics. Meanwhile, those with well-performing assets do not feel compelled to realize them—both due to valuations and the advent of infinite-life funds and other means to extend their investment horizon. In the secondary market, sellers have been willing to take discounts given the market backdrop; however, like the primary market, buyers remain cautious of catching a falling knife. History suggests that private market valuations should decline to meet public prices, which typically lead private performance by six to 18 months. However, given steep corrections, public REITs could instead rise to meet private markets partway if sentiment improves. REITs also have low exposure to floating rate debt, with over 87% of the debt held by the industry at fixed rates. In contrast, almost half of all commercial property debt is floating rate. This leaves many private commercial property owners financially stressed as rates adjust upwards, creating immediate capital deployment opportunities for private credit.

We expect slowing inflation, any reduction in rates and tighter credit spreads to be among the key themes that determine the fundamental health of CRE over the next few quarters. We believe interest rate stabilization, potential disposals by forced sellers and the capacity to pass on high inflation to tenants may also emerge as catalysts to spur transaction volumes and bridge buyer and seller expectations. We think more dislocation is likely to occur as the market adjusts to the new economic reality. Eventually, the CRE cycle will turn. In the meantime, investors who can navigate differences in liquidity, asset exposures, and pricing may be able to capitalize on sector and regional divergence. Actively investing in high-quality assets positioned to capitalize on technological innovation, shifting demographics and sustainability may be the optimal strategy in a market where one size does not fit all.

Committed to providing you with the insights you need to build your practice.

1 MSCI. As of July 25, 2023.

2 CBRE, Most US Office Buildings More than 90 Percent Leased. As of August 1, 2023.

3 CBRE, Global Office Rent Tracker. As of June 30, 2023.

4 MSCI. As of November 23, 2022.

5 McKinsey - Empty Spaces, Hybrid Places. As of July 2023.

6 Jones Lang LaSalle, United States Retail Outlook Q2 2023. As of June 30, 2023.

7 Nareit. As of July 5, 2023.

8 CBRE, Global Data Center Trends 2023. As of July 14, 2023.

9 Reuters. As of April 3, 2023.

Glossary:

FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs.

Risk Considerations

Investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity, interest rate, prepayment and extension risk. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. The value of securities with variable and floating interest rates are generally less sensitive to interest rate changes than securities with fixed interest rates. Variable and floating rate securities may decline in value if interest rates do not move as expected. Conversely, variable and floating rate securities will not generally rise in value if market interest rates decline. Credit risk is the risk that an issuer will default on payments of interest and principal. Credit risk is higher when investing in high yield bonds, also known as junk bonds. Prepayment risk is the risk that the issuer of a security may pay off principal more quickly than originally anticipated. Extension risk is the risk that the issuer of a security may pay off principal more slowly than originally anticipated. All fixed income investments may be worth less than their original cost upon redemption or maturity.

When interest rates increase, fixed income securities will generally decline in value. Fluctuations in interest rates may also affect the yield and liquidity of fixed income securities.

Mortgage-related and other asset-backed securities are subject to credit/default, interest rate and certain additional risks, including extension risk (i.e., in periods of rising interest rates, issuers may pay principal later than expected) and prepayment risk (i.e., in periods of declining interest rates, issuers may pay principal more quickly than expected, causing the strategy to reinvest proceeds at lower prevailing interest rates).

An investment in Real Estate Investment Trusts ("REITs") involves certain unique risks in addition to those risks associated with investing in the real estate industry in general. REITs whose underlying properties are focused in a particular industry or geographic region are also subject to risks affecting such industries and regions. The securities of REITs involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements because of interest rate changes, economic conditions, tax code adjustments, and other factors.

General Disclosures

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Neither MSCI nor any other party involved in or related to compiling, computing, or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability, or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, a licensed entity regulated by the Securities and Futures Commission of Hong Kong (SFC). This material has not been reviewed by the SFC. © 2023 Goldman Sachs. All rights reserved.

Singapore: Investment involves risk. Prospective investors should seek independent advice. This advertisement or publication material has not been reviewed by the Monetary Authority of Singapore. This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

· Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

· Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

· Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

· Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws.

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

New Zealand: This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar: This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser. The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

East Timor: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds), or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed under any laws or regulations of Timor-Leste. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person or institution without the prior consent of Goldman Sachs Asset Management.

Vietnam: Please Note: The attached information has been provided at your request for informational purposes only. The attached materials are not, and any authors who contribute to these materials are not, providing advice to any person. The attached materials are not and should not be construed as an offering of any securities or any services to any person. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer under the laws of Vietnam. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Cambodia: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds) or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer or investment advisor under The Securities and Exchange Commission of Cambodia. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

337461-OTU-1888439 Date of First Use: October 31, 2023