October 31, 2023 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact Us

Valentijn van NieuwenhuijzenGlobal Head of Sustainability for Public Investing Valentijn van Nieuwenhuijzen |

Marco WillnerCo-Head of Dynamic Asset Allocation, Multi-Asset Solutions Marco Willner |

Sebastiaan ReindersHead of Innovation and Research, Sustainable Investing and Innovation Platform Sebastiaan Reinders |

Aviral UtkarshStrategist, Multi-Asset Solutions Aviral Utkarsh |

When the Biden administration marked the first anniversary of the Inflation Reduction Act (IRA) in mid-August this year, it rolled out some big numbers to demonstrate the impact of the legislation. In response to the act’s clean-energy and climate provisions, companies had announced more than $110 billion in new clean-energy manufacturing investments since the IRA became law, according to the White House. That includes over $70 billion in the electric vehicle (EV) supply chain and about $10 billion in solar manufacturing.1

The IRA has been surrounded by big claims—and intense criticism—from the start. When he signed the bill into law in 2022, President Biden hailed it as “the biggest step forward on climate ever.”2 To spur investment, the IRA relies on a package of tax incentives intended to accelerate the deployment of clean energy as well as clean vehicles, buildings and manufacturing.3 These include tax credits for investment in renewable energy projects and facilities that generate clean electricity. The law provides tax breaks for the manufacturing of components for solar and wind energy, inverters,4 battery components and critical minerals. It also sets out production tax credits for renewable and clean electricity as well as power from qualified nuclear facilities.

Republicans have leveled a wide range of criticisms at the law, which passed both houses of Congress in party-line votes.5 Senate Republican Leader Mitch McConnell, for example, has called the IRA a “reckless taxing and spending spree” that will have “no meaningful impact on the world's climate.”6 Other critics charge that the IRA benefits foreign companies in countries such as China.7 In particular, the law's incentives for the purchase of EVs have faced pushback, and not just from Republicans. Sen. Joe Manchin, a Democrat who co-sponsored the IRA but has criticized the administration's implementation of the law, said he would oppose a rush to mass adoption of EVs while China controls the supply of critical minerals required for their production.8

One year from the launch of the IRA, we drilled down into the data to understand the investment response underlying the official optimism. What we found was that—so far at least—the reality is living up to or even exceeding expectations. Analysis based on public announcements tracked by the American Clean Power Association (ACP), Climate Power and E2 show that 280 clean energy projects were announced across 44 US states in the IRA’s first year.9 These projects represent $282 billion in investment and are expected to create nearly 175,000 jobs. To find out which companies are talking about the IRA and what future projects they may be considering, we also examined earnings calls using Natural Language Processing. Solar energy was the clean-energy topic most often mentioned in combination with the IRA on these calls, followed by carbon capture and storage, and batteries and energy storage.10

The evidence of the IRA’s impact is mounting, but if the law is to achieve the goals set out by its supporters, challenges will have to be overcome. These include delays in connecting renewable energy projects to the grid and the potential for rising project costs, which could in turn push up the IRA's final price tag. Estimating the total bill for the IRA is difficult because most of the spending under the law comes in the form of uncapped tax breaks, meaning the cost will increase as more companies and households take advantage of the incentives. Initial cost estimates tended to range between $370 billion, a figure cited regularly by the White House,11 to $391 billion, calculated by the Congressional Budget Office.12

The IRA’s potential to boost US development and production of clean-energy technology critical to the sustainable energy transition has been widely touted since its inception. The law provides the most supportive regulatory environment in clean-tech history, potentially driving results including the first large-scale deployment of green hydrogen and carbon capture, according to Goldman Sachs Global Investment Research (GIR).13 The IRA’s incentives could potentially help the US gain a larger share of the global clean-tech market, where China now dominates the manufacturing and trade of most technologies.14

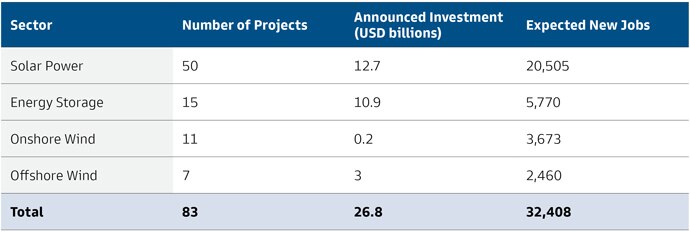

Significant progress has been made in the IRA’s first year. A recent report from ACP, for example, estimates that the clean energy projects announced through July 31, 2023, will add 184,850 megawatts of new clean energy capacity.15 The IRA’s support for manufacturing and job creation is also translating into concrete projects. Of the $282 billion of announced investment, just under $27 billion is earmarked for the construction or expansion of 83 manufacturing facilities devoted to utility-scale clean energy across four main sectors, as shown in the table below. The projects include offshore wind facilities in New York, a battery plant in Kentucky and solar development from Washington to Florida.16

Source: ACP, Climate Power, E2, Goldman Sachs Asset Management. As of August 31, 2023.

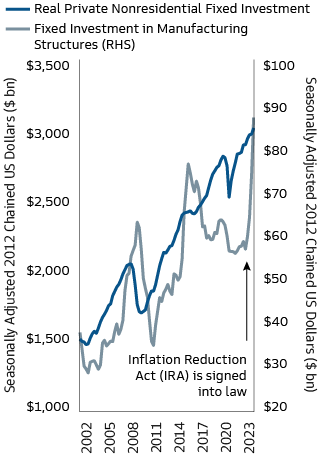

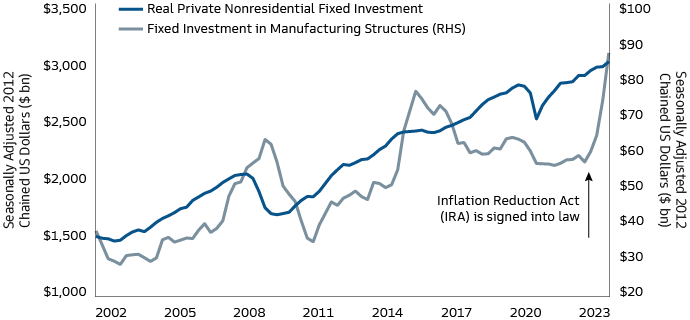

While many of these announced projects will take time to come online, and the capital expenditure to complete them will be spread over months or years, the construction of new facilities is already being reflected in US macroeconomic data. Private fixed investment in manufacturing facilities has surged since April 2022. It was propelled in part by the IRA and another piece of legislation, the CHIPS and Science Act, which provides funding and incentives to support semiconductor research and production.17

Source: Federal Reserve Bank of St. Louis, US Bureau of Economic Analysis, Goldman Sachs Asset Management. Data as of August 30, 2023. Seasonally adjusted 2012 chained US dollars.

The IRA’s tax credits are deliberately broad to encourage investment across a range of clean-energy solutions. Its investment tax credit for energy property, for example, covers projects in the following areas: fuel cell, solar, geothermal, small wind, energy storage, biogas, microgrid controllers, and combined heat and power properties.18 The base credit amount is 6% of qualified investment, though this can be increased by meeting requirements for wages and apprenticeships and for using domestic steel, iron and manufactured products. Similar incentives are built into most of the law’s tax provisions.

The scope of the IRA’s clean-energy incentives has encouraged companies to announce a wide variety of investments in the first year, with more set to come in the years ahead. An analysis of company earnings calls in the year through August 14, 2023, shows that the law has sparked a widespread discussion of clean-energy topics, signaling the potential for future investment. Using Natural Language Processing19 to scan 27,794 calls held between July 2022 and mid-August 2023, we identified three areas of significant interest: carbon capture, utilization and sequestration (CCUS); batteries and energy storage; and hydrogen fuel and infrastructure.20 These findings are consistent with previous Goldman Sachs research, which found that the IRA would be most transformative for products including utility-scale battery storage and green hydrogen, while accelerating investment in longer-term carbon capture projects.21

Three sectors have been most vocal in discussing the IRA and clean-energy topics: energy, industrials and materials. Energy companies have led the conversation when it comes to CCUS. The IRA’s support for the decarbonization of power generation includes extending and expanding an existing CCUS tax credit to include direct air capture and lowering the threshold for some facilities to benefit.22

Materials and industrial companies are the most vocal on batteries and energy storage, which are supported by the IRA’s production tax credit for domestic manufacturing of battery components as well as clean-vehicle and clean-energy incentives. Earnings calls in all three sectors have touched on hydrogen fuel and infrastructure, an area supported by numerous provisions in the IRA, including a hydrogen production tax credit. Mentions of hydrogen in our analysis also had the highest degree of certainty regarding potential investment, with 70% including a target or project numbers, while CCUS came in at 51% and batteries and energy storage at 43%.23

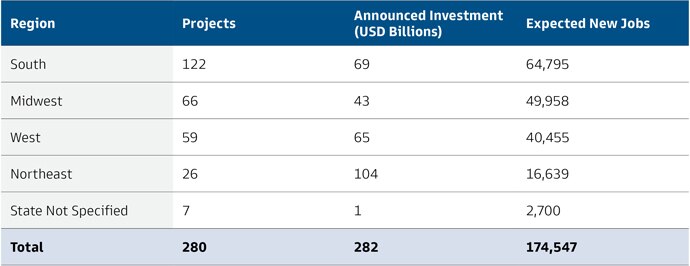

Job creation and economic expansion have been central themes of the rollout of the IRA.24 Our analysis shows that the announced investment linked to the IRA is spread broadly across the US, with the South attracting the largest number of projects and the Northeast in line for the largest investment. The following table provides a regional breakdown of announced projects and investment and the tally of jobs they are expected to create.

Source: ACP, Climate Power, E2, Goldman Sachs Asset Management. As of August 31, 2023.

This regional distribution of announced projects translated into $225 billion of investment planned in Republican congressional districts as of July 25, compared with $38 billion in Democratic districts.25 The jobs count so far also tilts in favor of Republican districts, which were in line for 96,216 new jobs, compared with 64,418 in Democratic districts.

A recent study published in the Brookings Papers on Economic Activity series estimates the total budgetary effects of the IRA’s climate provisions (tax credits and direct expenditures) at $900 billion through 2031.26 It concludes that the climate measures in the IRA will remain cost-effective even with this higher price tag.

This conclusion is based on a comparison of the cost of abating carbon dioxide (CO2) emissions with the “social cost of carbon,” defined as the economic costs, or damages, of emitting one additional ton of CO2 into the atmosphere. Even at the high end of estimated budgetary effects of the IRA’s climate provisions—$1.2 trillion through 2031—the law’s tax credits enable the reduction of CO2 emissions at $83 per metric ton for the power sector, according to the study. That is far less than the damage caused by the emission of additional CO2—about $200 per ton.27 And that’s before benefits including improved air quality are taken into account.

For all the progress made during the IRA’s first year, challenges still remain. One of these is the potential for rising project costs. The authors of the Brookings study show that macroeconomic conditions led by higher interest rates and materials costs could hamper clean energy investment. In fact, the study cautions that “macroeconomic conditions may have larger impacts on IRA investments than IRA investments have on macroeconomic conditions.”28 A recent report from the US Department of Energy, for example, cited inflation along with supply chain constraints, geopolitical uncertainty and warranty provisions as factors hampering “the profitability of western wind turbine manufacturers across their land-based and offshore portfolios in 2022.”29

The growing backlog of renewable power projects seeking to connect to the electric grid also presents a potential hurdle for the expansion of clean energy. A recent study led by Lawrence Berkeley National Laboratory (Berkeley Lab) shows renewable power projects are spending longer in so-called interconnection queues, a term that refers to the impact studies developers must complete before a project can connect to the system.30 The study shows that nearly 2,000 gigawatts of renewable energy and storage capacity was waiting in these queues at the end of 2022, a 40% increase from a year earlier. Entering an interconnection queue is just one step in the development process, but the data nevertheless provides “a general indicator for mid-term trends in developer interest,” according to the study.

Two main issues are causing these delays, according to Berkeley Lab: grid capacity and the design of interconnection evaluation processes. Some progress has been made toward removing these obstacles. The Federal Energy Regulatory Commission has approved reforms to speed up the interconnection evaluation process, and the Infrastructure Investment and Jobs Act contains provisions to support the addition of transmissions lines to the grid.31

The reduction of greenhouse gas (GHG) emissions is a central goal of the IRA, and recent research indicates that it could have a significant impact in this area. A study published in the journal Science, for example, found that the law’s provisions could lead to a reduction in GHG emissions of between 43% and 48% from 2005 levels by 2035.32 Without the IRA, the decline would have been in the range of 27% to 35%. The law may have its greatest effect in the power sector because its incentives “amplify trends already underway and lower decarbonization costs,” according to the study.

The US has set a target for reducing GHG emissions by between 50% and 52% below 2005 levels by 2030.33 While the IRA’s projected impact falls short of this level, the Science study shows that the law helps to narrow the “implementation gap” in reaching the official target by at least 50%.34 One unknown is the IRA’s potential to spur other federal agencies as well as state and local governments and companies to increase their own climate ambitions, which “may be key to closing the 2030 implementation gap,” according to the study.

The IRA’s support for jobs, especially in manufacturing, should support economic growth and consumption, in turn supporting the US equity and credit markets. If four out of five projects already announced finish on time and create the expected number of jobs, this could lead to about 65,000 new jobs, mostly in manufacturing, by the end of 2024, with 50,000 coming in 2024 itself. For context, 106,000 manufacturing jobs were created overall in the US over the past 12 months.35 If job creation continues at this pace, the IRA and the CHIPS and Science Act could spur the creation of half a million manufacturing jobs over the coming decade, pushing the total to 13.5 million—a level last seen in 2008.

In our view, the materials, industrial, energy and utility sectors stand to benefit the most from this boost to manufacturing, though companies will vary widely in their exposure to the IRA. As a result, active stock-picking will be the best way to take advantage of the long-term opportunities created by the IRA in public markets. On the private side, we expect the law to open up an abundance of pure-play opportunities across the spectrum of clean-energy technology, as the law’s tax incentives make the development of new technologies more profitable.

For all the investment the IRA is spurring in the US, its ultimate impact could be much greater. The law has already prompted responses around the world, including from the European Union (EU). In February 2023, EU policy makers responded to the IRA with a Green Deal Industrial Plan to increase the competitiveness of Europe’s net-zero emission industry and speed the transition to climate neutrality. The plan foresees investment in strategic net zero sectors, including through tax benefits.36 India’s government has launched a range of initiatives to spur development of renewable energy technologies under its Production-Linked Incentive Scheme.37 In the race to shape the future of clean energy, we believe this competition among countries can only accelerate global progress toward critical climate goals while expanding opportunities for investors.

Committed to providing you with the insights you need to build your practice.

1 “Fact Sheet: One Year In, President Biden’s Inflation Reduction Act Is Driving Historic Climate Action and Investing in America to Create Good-Paying Jobs and Reduce Costs,” White House press release. As of August 16, 2023.

2 “Remarks by President Biden at Signing of H.R. 5376, The Inflation Reduction Act of 2022,” White House press release. As of August 16, 2022.

3 “Clean Energy Tax Provisions in the Inflation Reduction Act,” White House website. As of September 5, 2023.

4 Inverters are key components of solar energy systems. They convert the direct current electricity generated by solar panels to the alternating current used by the electrical grid.

5 For the vote in the House of Representatives, see “House Passes Inflation Reduction Act, Sending Climate and Health Bill to Biden,” The Washington Post. As of August 12, 2022. For the vote in the Senate, see “Senate Approves Inflation Reduction Act, Clinching Long-Delayed Health and Climate Bill,” The Washington Post. As of August 7, 2022.

6 ”One Year Later, Democrats’ Reckless Spending Spree Is Showering Cash on Foreign Companies,” Mitch McConnell Republican Leader Web Page on Senate Website. As of July 26, 2023.

7 For example, Republican Congressman Jason Smith, who is chairman of the House Ways and Means Committee, has said the IRA is “paying big dividends to big business and China.” See “GOP Case for Repealing Climate Law: China and Wall Street,” E&E News by Politico. As of April 20, 2023.

8 ”Chairman Manchin’s Opening Remarks During a Full Committee Hearing to Examine Opportunities to Counter the People's Republic of China's Control of Critical Mineral Supply Chains,” US Senate Committee on Energy and Natural Resources Website. As of September 28, 2023.

9 Goldman Sachs Asset Management. As of September 4, 2023.

10 Goldman Sachs Asset Management analysis of earnings calls by companies in the MSCI ACWI Investable Market Index. Data as of August 14, 2023. NLP output reviewed by analyst.

11 See for example “Building a Clean Energy Economy: A Guidebook to the Inflation Reduction Act’s Investments in Clean Energy and Climate Action,” The White House. As of January 2023.

12 “CBO Scores IRA With $238 Billion of Deficit Reduction,” Committee for a Responsible Federal Budget. As of September 7, 2022. The CBO estimated the cost of the IRA’s energy and climate provisions over the period 2022-2031.

13 “Carbonomics: The Third American Energy Revolution,” Goldman Sachs Global Investment Research. As of March 22, 2023.

14 “Energy Technology Perspectives 2023,” International Energy Agency. As of January 2023. One of the aims of the IRA was to help make the US a leader in clean-energy technologies. See “Fact Sheet: President Biden Sets 2030 Greenhouse Gas Pollution Reduction Target Aimed at Creating Good-Paying Union Jobs and Securing US Leadership on Clean Energy Technologies,” The White House. As of April 22, 2021.

15 “Clean Energy Investing in America,” ACP. As of August 2023. This report is based on public announcements made from August 16, 2022, through July 31, 2023.

16 “Clean Energy Investing in America,” ACP. As of August 2023. This report is based on public announcements made from August 16, 2022, through July 31, 2023.

17 “Biden Signs Order on $52 Billion Chips Law Implementation,” Reuters. As of August 25, 2022.

18 “Clean Energy Tax Provisions in the Inflation Reduction Act,” White House website. As of September 5, 2023.

19 Natural Language Processing is a branch of artificial intelligence that enables computers to analyze and understand human language.

20 GS Asset Management analysis of earnings calls by companies in MSCI ACWI Investable Market Index. Data as of August 14, 2023.

21 “US Inflation Reduction Act: What's Transformational, What's Supportive, What's Underappreciated,” GS SUSTAIN. As of August 30, 2022.

22 “Building a Clean Energy Economy: A Guidebook to the Inflation Reduction Act’s Investments in Clean Energy and Climate Action,” The White House. As of January 2023.

23 GS Asset Management analysis of earnings calls by companies in the MSCI ACWI Investable Market Index. Data as of August 14, 2023.

24 At a fundraiser in Utah just before the law’s first anniversary, President Biden said he regretted the name given to the legislation, “because it has less to do with reducing inflation than providing alternatives where we generate economic growth.” See “Biden Wishes His Signature Climate Law Was Called Something Else,” Bloomberg News. As of August 10, 2023.

25 Based on “One Year of Our Clean Energy Boom,” a report from Climate Power, and additional analysis by Goldman Sachs Asset Management. Data as of July 25, 2023. Climate Power is an independent strategic communications and paid media operation focused on building support for climate action. It was founded by the Center for American Progress Action Fund, the League of Conservation Voters and the Sierra Club. See “Why Us” on the Climate Power website.

26 John Bistline (Electric Power Research Institute), Neil Mehrotra (Federal Reserve Bank of Minneapolis) and Catherine Wolfram (Harvard University). “Economic Implications of the Climate Provisions of the Inflation Reduction Act,” Brookings Papers on Economic Activity. As of March 29, 2023.

27 Another Brookings publication cites social cost estimates in the latest literature ranging from $100 to $380 per ton of CO2. See Bistline, Mehrotra and Wolfram. “The Inflation Reduction Act Could Energize the Economy,” Brookings. As of May 1, 2023.

28 Bistline, Mehrotra and Wolfram. “Economic Implications of the Climate Provisions of the Inflation Reduction Act,” Brookings Papers on Economic Activity. As of March 29, 2023.

29 “Offshore Wind Market Report: 2023 Edition,” Office of Energy Efficiency and Renewable Energy, US Department of Energy. As of August 2023. The report notes that the IRA “may soften the adverse impact of rising inflation, supply chain constraints, and interest rates on offshore wind project costs for early-stage offshore wind projects.”

30 “Grid Connection Requests Grow by 40% in 2022 as Clean Energy Surges, Despite Backlogs and Uncertainty,” Lawrence Berkeley National Laboratory. As of April 6, 2023.

31 “Grid Connection Requests Grow by 40% in 2022 as Clean Energy Surges, Despite Backlogs and Uncertainty,” Lawrence Berkeley National Laboratory. As of April 6, 2023.

32 John Bistline et al. “Emissions and energy impacts of the Inflation Reduction Act,” Science. As of June 29, 2023. The researchers leveraged results from nine independent models to reach their conclusions.

33 “FACT SHEET: President Biden Sets 2030 Greenhouse Gas Pollution Reduction Target Aimed at Creating Good-Paying Union Jobs and Securing U.S. Leadership on Clean Energy Technologies,” The White House. As of April 22, 2021.

34 Bistline et al. “Emissions and energy impacts of the Inflation Reduction Act,” Science. As of June 29, 2023.

35 “FRED Economic Data,” Federal Reserve Bank of St. Louis. Data as of September 1, 2023.

36 “The Green Deal Industrial Plan: Putting Europe’s Net-Zero Industry in the Lead,” European Commission press release. As of February 1, 2023.

37 “Government incentivizes local development and manufacturing of renewable energy technologies,” Ministry of New and Renewable Energy press release. As of March 22, 2022.

Risk Considerations

All investing involves risk, including loss of principal.

Environmental, Social and Governance (“ESG”) strategies may take risks or eliminate exposures found in other strategies or broad market benchmarks that may cause performance to diverge from the performance of these other strategies or market benchmarks. ESG strategies will be subject to the risks associated with their underlying investments’ asset classes. Further, the demand within certain markets or sectors that an ESG strategy targets may not develop as forecasted or may develop more slowly than anticipated.

The above are not an exhaustive list of potential risks. There may be additional risks that are not currently foreseen or considered.

General Disclosures

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

The views expressed herein are as of the date of the publication and subject to change in the future. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA): This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, a licensed entity regulated by the Securities and Futures Commission of Hong Kong (SFC). This material has not been reviewed by the SFC. © 2023 Goldman Sachs. All rights reserved.

Singapore: Investment involves risk. Prospective investors should seek independent advice. This advertisement or publication material has not been reviewed by the Monetary Authority of Singapore. This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

· Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

· Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

· Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

· Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws.

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

New Zealand: This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar: This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser. The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

East Timor: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds), or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed under any laws or regulations of Timor-Leste. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person or institution without the prior consent of Goldman Sachs Asset Management.

Vietnam: Please Note: The attached information has been provided at your request for informational purposes only. The attached materials are not, and any authors who contribute to these materials are not, providing advice to any person. The attached materials are not and should not be construed as an offering of any securities or any services to any person. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer under the laws of Vietnam. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Cambodia: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds) or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer or investment advisor under The Securities and Exchange Commission of Cambodia. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

337397-OTU-1883762 Date of First Use: October 31, 2023