Many predicted a technical recession, earnings recession, or both heading into this year, reflected by portfolios positioned tactically defensive. In reality, growth has surprised to the upside, inflation has moderated, and investor sentiment has been overtly risk on. Though the direction of monetary policy remains uncertain, growth risks have partially faded, and thus, we feel that now is the time to focus on long-term positioning.

Unexpected strong market returns have been driven in part by a seminal moment in technology: the advent of generative artificial intelligence. The recent run-up in equities informs our view, however, that markets may be pricing in perfection. While mega-cap tech stocks have been those commanding headlines of today, strategic thinking in other asset classes may generate returns of tomorrow.

In recent years, strong performance may have been generated by viewing the investment landscape through a telescope and positioning around macro trends. But now more than ever, we see the need for analyzing and building portfolios with a microscope. In our view, the next investment cycle will be defined by micro differentiation, enhanced risk-awareness, and an increased focus on alpha.

In this edition of the Market Know-How, we explore how investors may consider participation in a global recovery while maintaining a focus on risk management, with emphasis on:

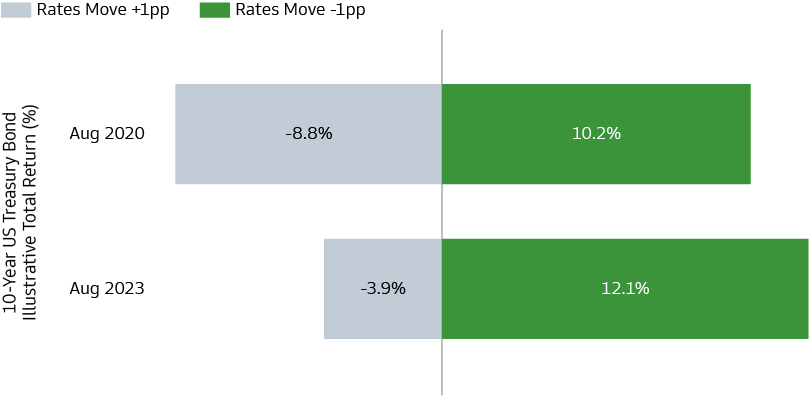

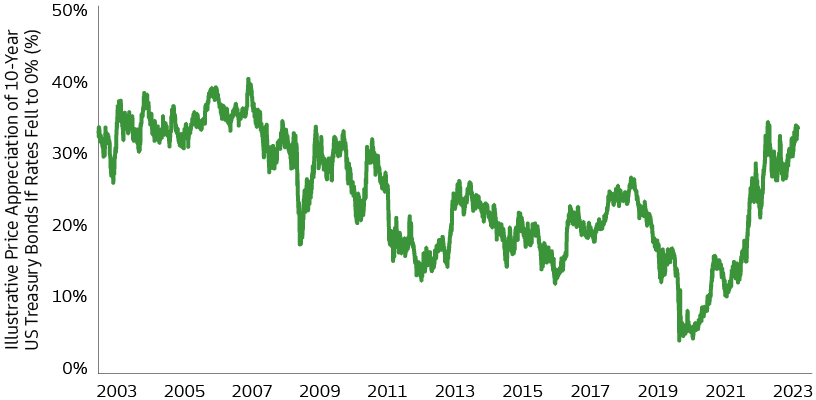

- Extending duration with the goal of hedging against the risk of an equity market drawdown.

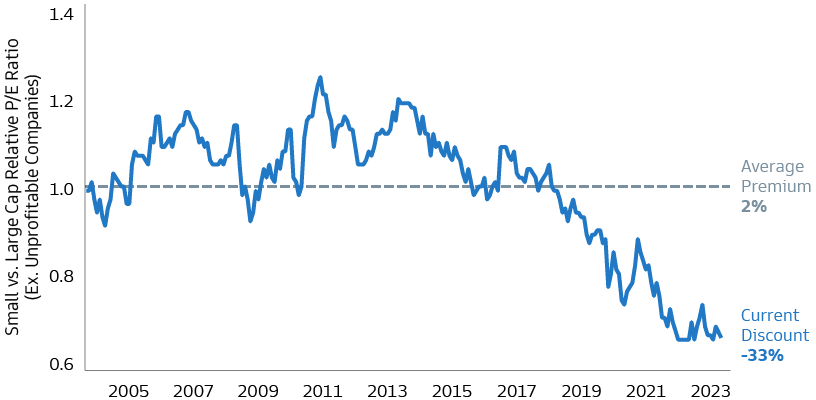

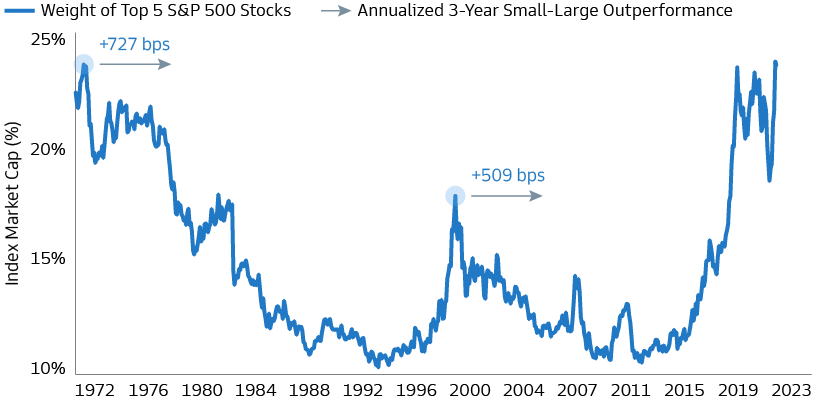

- Positioning for a broadening equity market while taking advantage of an attractive entry point in US small caps.

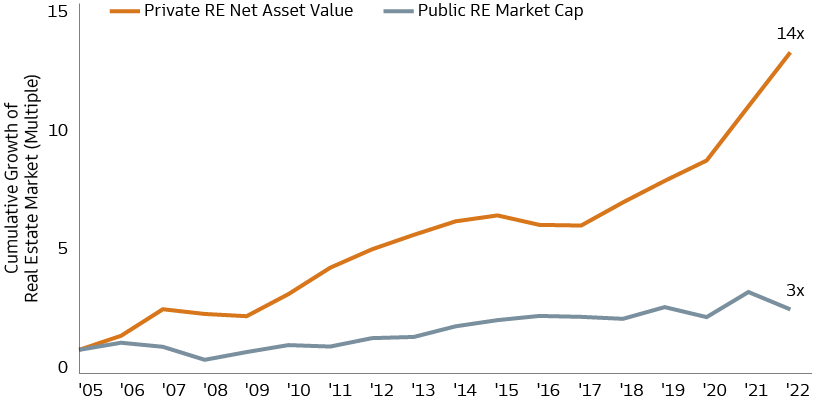

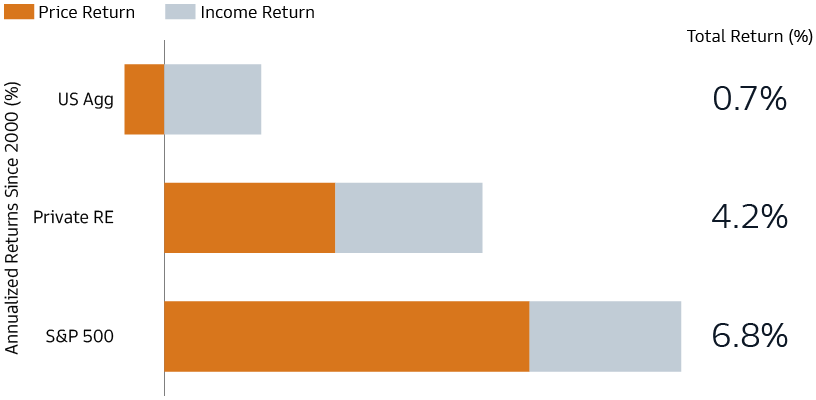

- Diversifying public market exposures and seeking a balanced return distribution via private real estate.