Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsNearly all asset classes have benefitted from strong beta returns over the past 18 months, but beta returns are likely to be lower in the coming years. In today’s environment, we believe focusing on alpha generation is part of the answer.

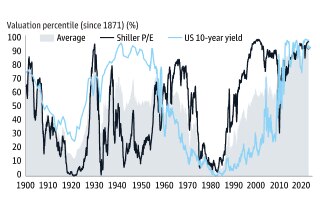

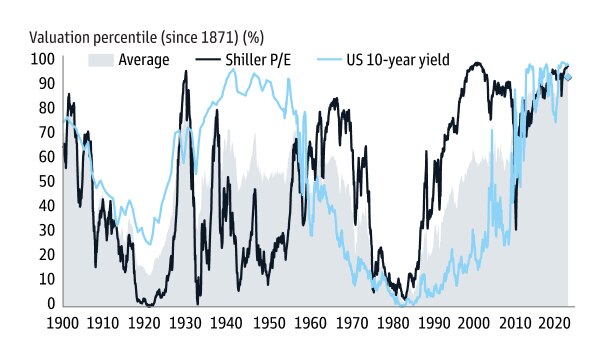

Valuations across all asset classes are near record highs, limiting room for further upside and making asset prices more vulnerable to negative news or sentiment. (Exhibit 4)

After nearly two years of developed market (DM) policy rates trending lower and currently hovering at all time lows, interest rates will likely rise in 2022. At the same time, bond buying by major central banks is set to fall. Low interest rates have supported higher public and private equity valuations while quantitative easing (QE) has tightened spreads for many fixed income securities. Easy monetary policy has also contributed to strong corporate earnings and margins, which now have less room for improvement. Policy normalization may not immediately reverse these trends, but it leaves less room for asset prices to move higher and potentially chips away at valuation support. (Exhibit 5)

Being positioned on the right side of inflation and disruption will be critical to outperformance. We believe recent trends such as growth versus value, the US versus the rest of the world and the technology sector versus diversified exposure are likely to be less pronounced than in the previous cycle as technological innovation spreads across industries and regions. At the same time, low commodity prices, which contributed to lower earnings and valuations for commodity oriented companies in recent years, have risen significantly. As a result, we expect a modest level of overall earnings growth that is more balanced across regions and sectors. We believe this environment will have a higher dispersion of returns driven by companies that are able to benefit from or withstand an inflationary environment and that have secular growth drivers.

Exhibit 4: Expensive valuations after the bull market in every major asset class, similar to the Golden 1920s and 1950s

Source: Robert Shiller, Datastream, Goldman Sachs Global Investment Research. As of November 17, 2021.

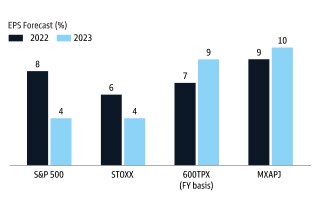

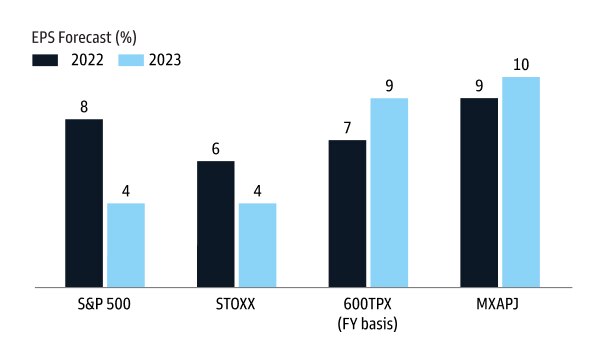

Exhibit 5: EPS GS top-down forecasts

Source: STOXX, Goldman Sachs Global Investment Research. As of December 13, 2021.

Alpha's Return Potential

Weighing risk versus reward favors alpha strategies. The ability to generate alpha becomes even more important in a lower-return environment as alpha will comprise a greater portion of an investor's total returns.

Alpha strategies have the ability to pick securities or assets across an opportunity set that can span all sectors and regions around the world, potentially adding the benefit of diversification to a portfolio.

In addition to these offensive benefits, active security selection also offers defensive benefits by managing risks. For example, we believe market cap-weighted passive indices leave investors overexposed to various risks: five stocks contribute about 23% of the market cap of the S&P 500, state owned enterprises account for roughly 18% of the MSCI EM Index and about a third of companies in the US small cap universe are unprofitable.

The Importance of Being Active

Being active across asset classes may be critical in this environment, though it requires focus on manager and strategy selection. For some investors taking a very long-term view and recognizing that beta returns over the past few years have been above average, active strategies with a moderate amount of alpha generation may help them achieve long-term goals, without necessarily adding a high degree of marginal risk.

Investors who need to continue to generate higher levels of return could consider taking more risk, potentially through long-term, less liquid alternative investments that are driven by factors less correlated to market beta, such as private secondary offerings and more complex opportunities in the private markets.

Alternatives and Private Assets

We prefer strategies with a wide opportunity set, such as absolute return strategies in the alternatives universe, unconstrained fixed income strategies, or global and thematic strategies within public equities. These strategies can benefit from security specific opportunities and regional differences in valuations, as well as changes in broader market conditions such as growth, interest rates or inflation. Pairing private and public investments can take advantage of differentials in valuation, growth opportunities or access.

The secular shift toward alternatives is likely to continue as investors look for asset classes and strategies that may offer higher returns than public markets. A combination of skilled managers and fewer constraints allow hedge funds and private market strategies to take advantage of alpha opportunities across many time horizons and transaction types. Hedge funds can further amplify their alpha generation ability with shorting.

Read the Next Theme

×

Take a Deeper Dive into Related Content

-

Municipal Outlook 2022: The Journey Home

January 13, 2022 With interest rates projected to head higher and credit spreads at the lower end of historical averages, we believe it is time for investors to pare credit risk back to neutral and re-visit their core municipal allocation by opportunistically extending duration and strategically deploying cash. Learn more in our Municipal Fixed Income Outlook 2022. Read More -

Fixed Income Outlook 1Q 2022: Goldilocks and The Three Bulls or Bears?

January 13, 2022 In 2022, faced with a complex macro backdrop, central banks will be seeking to deliver “goldilocks” policy normalization to keep inflation in check - neither too hot nor too cold. The temperature of financial markets will depend on the balance between bearish and bullish factors. Learn more in our Fixed Income 1Q22 Outlook: Goldilocks & The Three Bulls or Bears? where we discuss growth, inflation, monetary policy, interest rates, sustainability and much more. Read More -

Multi-Asset Solutions Outlook 2022: Intensified Fed Policy Uncertainty Adds Market Volatility as Inflation Path Remains Elusive

January 13, 2022 Until recently, the economic expansion that followed the Global Financial Crisis seemed like it would never end. Then it appeared to do just that when the pandemic hit in early 2020, only to give way to a new cycle of growth and optimism. We invite you learn more in our Multi-Asset Solutions Outlook 2022 where we review our market observations, our outlook, and downside risks to consider. Read More

×

Read Other Investment Ideas Themes

-

Sustainability Revolution

January 13, 2022 Sustainable strategies have increasingly been able to have a positive impact and generate competitive long term performance. Read More -

China: Too Big to Ignore

January 13, 2022 Even as growth slows, investment opportunities abound in the world's second largest economy. Read More -

Emerging Opportunities in Emerging Markets

January 13, 2022 A diversified emerging market strategy may offer attractive return potential. Read More -

Using Disruption to Your Advantage

January 13, 2022 Investment returns may increasingly be driven by companies that best respond to technological innovation and other disruptive trends. Read More -

-

Rising Rates and The Policy Unwind

January 13, 2022 The era of rock bottom interest rates may finally be ending. Read More

×