Menu

Our services in the selected location:

- No services available for your region.

Your browser is out of date.

-

In The Spotlight

Alternatives - Private Credit

Investing globally and across the capital structure, our private credit platform combines deep expertise and long-standing relationships with high caliber sponsors globally with the goal of identifying attractive risk-adjusted return opportunities across the credit spectrum.Read More -

-

- By Asset Class

-

Fixed Income

-

Equities

-

Alternatives

In The Spotlight

Perspectives

In this edition of Perspectives, we explore how investors can seek out potential opportunities across public and private markets as confidence in the macroeconomic outlook continues to build.Read More -

-

- Product Collateral

-

Product Brochures

-

Investment Solutions

-

Fact Cards

-

Fund Commentaries

-

- Documents and Forms

-

Tax Information

-

Forms & Applications

-

Regulatory Documents

-

All Documents

In The Spotlight

Our In-Depth Commentary Could Help You Gain a Competitive Edge

Read MoreStay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

-

-

-

- About Us

-

Overview

-

News and Media

-

Contact Us

-

-

Explore how we can help you

Contact UsPrices rose just about everywhere in 2021. Most of the causes—supply and labor shortages, rising energy prices, pent-up consumer demand, aggressive fiscal stimulus—can be traced directly to the Covid-19 pandemic. And as we're reminded almost daily, the pandemic isn't over. With supplies constrained and demand strong, anxiety about inflation is on the rise.

For much of 2021, many of the forces stoking inflation appeared to be transitory. Supply disruptions, including raw material and labor shortages and congestion at ports, severed key links in global supply chains, forcing up prices at a time when demand for goods was strong. Some of the resulting cost pressures may ease as supply chains are repaired and the effects of pent up demand start to fade.

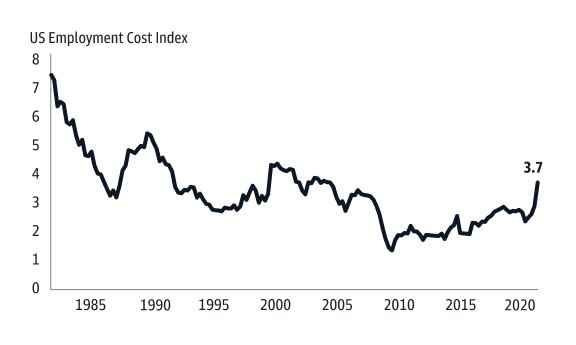

But transitory may not mean the rate of inflation will fall quickly in 2022. Prices for some goods, including shelter, may continue to rise above their pre-Covid-19 levels for some time. Autos are another wildcard; inflation has been high in this sector and could remain so if semiconductor shortages are not resolved until 2023. Solid wage growth and inflation expectations (Exhibits 1, 2) are also likely to prevent a swift return to the low inflation environment that has persisted in recent years, though the effects will vary across economies. Wage pressures in particular appeared to be a key factor behind the US Federal Reserve's late 2021 policy pivot toward tighter monetary policy. If goods prices don't ease and price pressures expand due to the demand for services as economies fully reopen, we could see a further increase in inflation above the Fed's 2% average target. Though it hasn't happened yet, sustained higher inflation could push up intermediate bond yields and take the 10-year US Treasury yield above 2% for the first time since mid-2019, potentially causing problems for longer duration fixed income strategies and growth stocks.

Exhibit 1: US ECI experienced its strongest annual rise since 2001 in Q3

Source: Macrobond, Goldman Sachs Asset Management. As of 2021 Q3.

Exhibit 2: UK private sector wage growth is high but moderating

Source: Macrobond, Goldman Sachs Asset Management. As of September 2021. Three month moving average.

If health concerns fade, we believe an increase in labor force participation may help temper wage growth. A slowdown in commodity price gains may also reduce inflation expectations. Still, in this uncertain environment, investors may want to consider tilting toward strategies that have typically done well when prices rise given the potential for inflation to run warmer than it did during the last cycle, if not quite as a hot as it did in the 1970s.

Equities

Equities have historically given investors the best chance of outperforming inflation over the long term. Even so, we believe active management is essential, as inflation will affect different companies in different ways. For example, managers who can tilt toward companies that are somewhat shielded from rising prices or likely to benefit from them, such as energy producers or firms with low labor costs or resilient supply chains, may be able to generate higher returns relative to strategies that track a benchmark.

Real Assets

More specifically, cyclical equities tend to have a higher representation of sectors that stand to gain from inflation, such as financials, energy and basic materials. Additionally, real asset equities (real estate, infrastructure) may prove resilient as prices rise, since many leases and contracts are linked to inflation and incumbent asset values tend to increase when land, labor and material costs rise.

Multi-Sector Credit and TIPS

Multi sector credit strategies that can tilt toward floating rate bank loans and bonds from companies with robust revenue growth and pricing power may do well in an inflationary environment. Treasury Inflation Protected Securities (TIPS) won't offer the same level of diversification but can protect against unanticipated inflation and offer a potential complement as rates rise and inflation regimes shift.

Read the Next Theme

×

Take a Deeper Dive into Related Content

-

Municipal Outlook 2022: The Journey Home

January 13, 2022 With interest rates projected to head higher and credit spreads at the lower end of historical averages, we believe it is time for investors to pare credit risk back to neutral and re-visit their core municipal allocation by opportunistically extending duration and strategically deploying cash. Learn more in our Municipal Fixed Income Outlook 2022. Read More -

Fixed Income Outlook 1Q 2022: Goldilocks and The Three Bulls or Bears?

January 13, 2022 In 2022, faced with a complex macro backdrop, central banks will be seeking to deliver “goldilocks” policy normalization to keep inflation in check - neither too hot nor too cold. The temperature of financial markets will depend on the balance between bearish and bullish factors. Learn more in our Fixed Income 1Q22 Outlook: Goldilocks & The Three Bulls or Bears? where we discuss growth, inflation, monetary policy, interest rates, sustainability and much more. Read More -

Multi-Asset Solutions Outlook 2022: Intensified Fed Policy Uncertainty Adds Market Volatility as Inflation Path Remains Elusive

January 13, 2022 Until recently, the economic expansion that followed the Global Financial Crisis seemed like it would never end. Then it appeared to do just that when the pandemic hit in early 2020, only to give way to a new cycle of growth and optimism. We invite you learn more in our Multi-Asset Solutions Outlook 2022 where we review our market observations, our outlook, and downside risks to consider. Read More

×

Read Other Investment Ideas Themes

-

Beta Gives Way to Alpha

January 13, 2022 At current high valuations, the ability to generate alpha will be more important. Read More -

Looking Beyond US Equities

January 13, 2022 It may be time to diversify into other regions and global thematic strategies. Read More -

Sustainability Revolution

January 13, 2022 Sustainable strategies have increasingly been able to have a positive impact and generate competitive long term performance. Read More -

China: Too Big to Ignore

January 13, 2022 Even as growth slows, investment opportunities abound in the world's second largest economy. Read More -

Emerging Opportunities in Emerging Markets

January 13, 2022 A diversified emerging market strategy may offer attractive return potential. Read More -

Using Disruption to Your Advantage

January 13, 2022 Investment returns may increasingly be driven by companies that best respond to technological innovation and other disruptive trends. Read More

×

Ready To Learn More About Our 2022 Investment Ideas?