August 14, 2023 |

Muni Market Views

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsAugust 17, 2023 | 4 Minute Read

Michael ZinmanHead of High Yield Municipal Bond Research Michael Zinman |

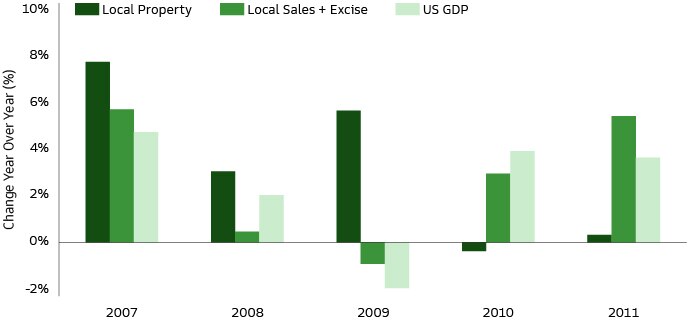

Making up nearly 40% of annual revenues on average, property taxes play a critical role in local government finance and tend to act as a stabilizing revenue source for municipalities during periods of fiscal stress. Property tax revenues generated in a particular fiscal year are based off valuations calculated one or two years prior to that budget cycle. This in effect, provides municipalities the luxury of weathering the fiscal storm created by near-term declines in more economically sensitive revenue streams such as income and sales taxes. In fact, it’s not uncommon for property taxes to increase during the first years of a recession while other revenues fall and then reverse the pattern during recovery (Exhibit 1). Consequently, the timing lag affords municipal management teams the flexibility to downwardly adjust expense budgets and/or potentially increase tax rates to offset upcoming tax base declines, provided the political will exists to do so.

Source: U.S. Bureau of Economic Analysis (BEA), as of March 31, 2023.

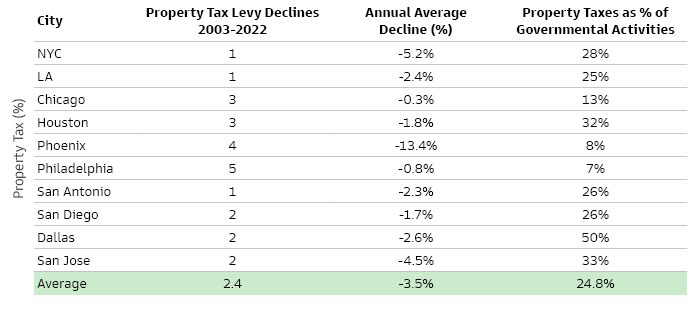

The relative stability of property tax revenues becomes more apparent when examining city-specific data. The top 10 most populous cities in the US saw their property tax levies decline, on average, just over 2 times over the 20-year period from 2003-2022. Furthermore, the severity of those declines was just -3.5% on average with only one city (Phoenix, -13.4%) experiencing double-digit average declines. As an aside, it’s worth noting that property taxes only accounted for 8% of Phoenix’s governmental activity revenues in fiscal year 2022.

Source: Various City Comprehensive Annual Financial Reports (CAFR) (2002-2022). As of December 31, 2022.

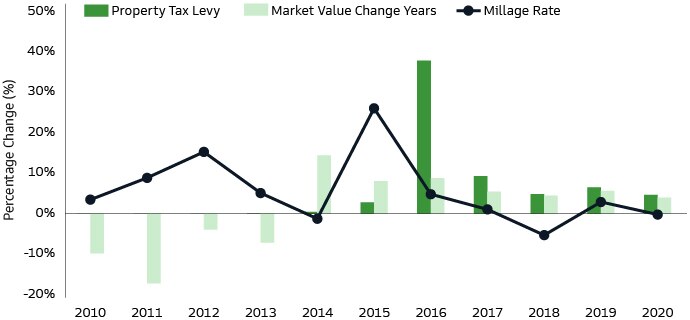

Spurred in part by Moody’s downgrade to non-investment grade in 2015, Illinois’ legislature and Chicago’s City Council took various actions that culminated in a multi-year property tax hike including a ~38% property levy increase in 2016. Along with various other revenue increases, the jump in Chicago’s property taxes—roughly 85% of which went towards pension contributions last year—eventually led to a material improvement in the city’s finances and the return of its investment grade rating by Moody’s in late 2022.

Source: City of Chicago Comprehensive Annual Financial Reports (CAFR) (2010-2020). As of December 31, 2020.

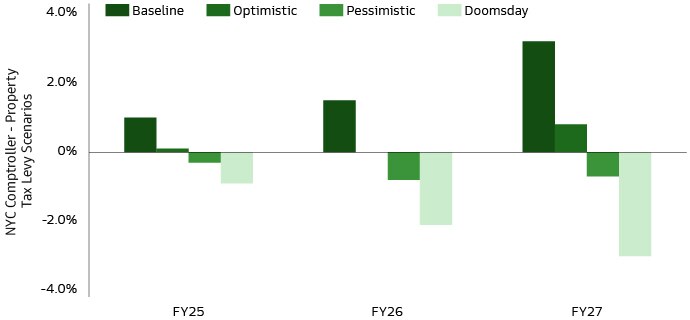

The impact that remote work arrangements has had on commercial real estate, particularly office buildings, has garnered significant headlines post-pandemic. While many office building appraisals have come under pressure as of late, we do not expect valuation declines to have a materially negative impact on property tax revenues or the fiscal health of municipalities. While property tax revenues generally make up the single largest revenue stream for local governments, municipal taxbases tend to be dominated by residential, not commercial property. Interestingly, the direct impact of office-generated property taxes tend to be relatively muted in some of the most business concentrated cities. Case in point, office buildings account for 18% and 21% of San Francisco and New York City tax bases, respectively. Given that property taxes make up roughly 28% of San Francisco’s total revenues and 25% of New York City’s, only ~5% of each city’s revenues are directly generated from office properties. In fact, the New York City Comptroller recently released a “doomsday” scenario for the Manhattan office market which concluded that a decline of -40% in the market value of office properties from pre-pandemic levels would result in a drop of just 3% of the city’s property tax levy in fiscal year 2027.

Source: New York City Comptroller, "Spotlight: What Risks Does the Office Market Pose for the City's Finances?" As of June 13, 2023.

Overall, municipal bond credit fundamentals remain strong. Between the financial flexibility that property tax revenues afford localities, manageable challenges related to office building valuation pressures and robust cash reserves bolstered by federal stimulus monies, we believe that localities remain well positioned from a credit perspective.

Committed to providing you with the insights you need to build your practice.

Risk Considerations

The economic and market forecasts presented herein are for informational purposes as of the date of this webpage. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this webpage.

Municipal Securities are subject to credit/default risk, interest rate risk and certain additional risks. High-yield, lower-rated securities involve greater price volatility and present greater credit risks than higher-rated fixed income securities. Investments in fixed-income securities are subject to credit and interest rate risks. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. Credit risk is the risk that an issuer will default on payments of interest and principal. All fixed income investments may be worth less than their original cost upon redemption or maturity. Income from municipal securities is generally free from federal taxes and state taxes for residents of the issuing state. While the interest income is tax-free, capital gains, if any, will be subject to taxes. Income for some investors may be subject to the federal Alternative Minimum Tax (AMT).

All investments involve risk including possible loss of principal. Individual asset classes involve unique risks. Bonds and fixed income investing are subject to interest rate risk. When interest rates rise, bond prices fall. Equity securities are more volatile than bonds and greater risks. Small cap company stocks involve greater risks than those customarily associated with larger companies. International securities entail special risks such as currency, political, economic, and market risks. These risks are heightened in emerging markets securities which may be less liquid and more volatile.

These risks should be fully evaluated before making an investment decision.

THESE MATERIALS ARE PROVIDED SOLELY ON THE BASIS THAT THEY WILL NOT CONSTITUTE INVESTMENT ADVICE AND WILL NOT FORM A PRIMARY BASIS FOR ANY PERSON'S OR PLAN'S INVESTMENT DECISIONS, AND GOLDMAN SACHS IS NOT A FIDUCIARY WITH RESPECT TO ANY PERSON OR PLAN BY REASON OF PROVIDING THE MATERIAL OR CONTENT HEREIN. PLAN FIDUCIARIES SHOULD CONSIDER THEIR OWN CIRCUMSTANCES IN ASSESSING ANY POTENTIAL INVESTMENT COURSE OF ACTION.

Disclosures

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Goldman Sachs does not provide legal, tax or accounting advice, unless explicitly agreed between you and Goldman Sachs (generally through certain services offered only to clients of Private Wealth Management). Any statement contained on this webpage concerning U.S. tax matters is not intended or written to be used and cannot be used for the purpose of avoiding penalties imposed on the relevant taxpayer. Notwithstanding anything in this page to the contrary, and except as required to enable compliance with applicable securities law, you may disclose to any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be aware that a determination of the tax consequences to them should take into account their specific circumstances and that the tax law is subject to change in the future or retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this webpage and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this webpage and may be subject to change, they should not be construed as investment advice.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

Portfolio holdings and/or allocations shown above are as of the date indicated and may not be representative of future investments. The holdings and/or allocations shown may not represent all of the portfolio's investments. Future investments may or may not be profitable.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. It should not be assumed that investment decisions made in the future will be profitable or will equal the performance of the securities discussed in this page.

Date of First Use: August 21, 2023. 331440-OTU-1856200.