August 7, 2023 |

GSAM Perspectives

In The Spotlight

In The Spotlight

In The Spotlight

Stay on top of the latest market developments, key themes, and investment ideas affecting your portfolio and practices.

Explore how we can help you

Contact UsAugust 7, 2023 | 12 Minute Read

Greg ShellHead of Inclusive Growth Strategy, Goldman Sachs Asset Management Greg Shell |

Salome MakharadzeHead of Private Market Sustainability Client Solutions and Product Strategy Salome Makharadze |

Greg Shell, the Head of Inclusive Growth Strategy, recently sat down with Salome Makharadze, Head of Private Market Sustainability Client Solutions and Product Strategy, to discuss his views on inclusive growth trends and opportunities in private markets after more than a decade of leading impact investing initiatives.

Greg Shell: I’m a capitalist and I believe deeply in the potential for private capital to improve people’s standard of living. My entire career has been as an investment professional, seeking out themes and opportunities to challenge the orthodoxy that companies only exist in service to increasing profits. Concurrently, I've dedicated significant time to civic society—as a board member, mentor, and volunteer across numerous not-for-profit organizations.

I believe in the transformative power of education and the need to take a deep interest in solving challenges within society. This comes from my experience growing up outside of Boston, where I had the opportunity to be part of an accelerated academic program that had a huge impact on my ultimate trajectory.

Working in the field of inclusive growth investing provides me with an opportunity to use the power of investment capital to scale private companies whose business models help address societal challenges that are affecting people's lives in a real way. I often ask myself, “what could be better than for an investment professional to marry their profession and vocation with a personal passion in something that gives meaning to their life?”

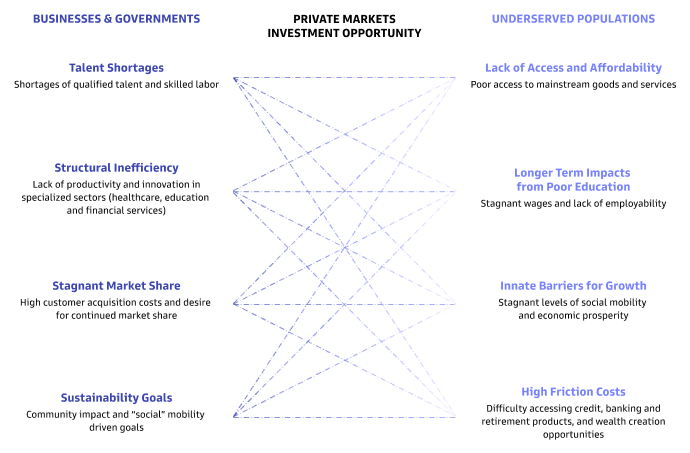

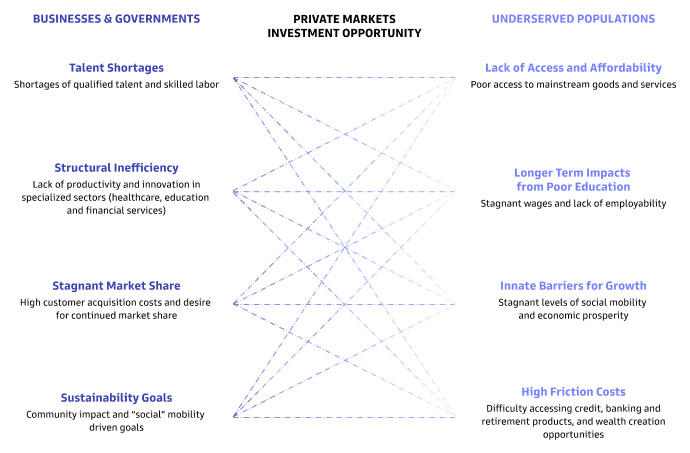

Shell: Inclusive growth investing is an acknowledgement that our economy would be larger, faster-growing, and more sustainable if we could bring more economic participants into the mainstream economy. There is a strong economic case to close access gaps for underserved populations because these gaps and overall inequality result in decreased aggregate demand and slower economic growth than what could be realized if these groups could be fully engaged. At the same time, many motivated stakeholders, such as businesses and governments, are recognizing the material costs of inequality and are seeking cost-effective solutions to address pain points and opportunities to grow in new markets. We believe private markets are able to bridge the gap for the two groups of stakeholders with the attractive market opportunity to invest in companies that improve outcomes by driving accessibility, affordability and quality healthcare, education and financial services.

Shell: My highest ambition since entering the field of impact investing has been for it to come off the sidelines and into the mainstream, which is something we’ve seen happen with the climate and energy transition thesis. It wasn't that long ago when the notion of investing in clean technology was an untouchable, un-investable universe. In the early days of climate investing, many opportunities were too early in development or capital intensive to attract investors; a virtuous cycle of demand was required to generate investable opportunities.1 When I think about how far we’ve come, it's quite remarkable.

While the climate thesis was predicated on declining cost curves to spur increased demand, funding for inclusive growth solutions already exists thanks to a large ecosystem of payors—including federal programs and agencies, governments, and private businesses—that are willing and able to fund initiatives to meet the needs of underserved populations. The limiting factor—and opportunity—has been a lack of economically viable solutions, but that is beginning to change with rise of new business models and technologies.

Shell: We believe that inclusive growth investing requires an approach that is accessible, innovative, and affordable, centered on three critical areas that also present significant commercial opportunities: healthcare, education, and financial services. We believe it is important to prioritize the very bottom of the hierarchy of needs, by addressing basic healthcare for underserved populations, as well as to invest in the infrastructure and systems to affordably improve health outcomes. It’s also clear that education is essential for people to be prepared for—and be able to access—the jobs of the future, especially given the increasing pace of digitization and automation, ongoing training is required to propel people to higher levels. Lastly, with progress on these measures, inclusive financial services can accelerate efforts to capture and build wealth over time.

When put together, these themes cover a staggering number of people who are not able to participate in the economy to their fullest potential, reducing potential growth that is needed to meaningfully improve social mobility. Not only is the investment opportunity very large, but there are sub-themes in those three categories that contain high-growth businesses with innovative business models.

Shell: Healthcare, for example, is a very large market and there are a significant number of people unable to access healthcare services that many of us take for granted. Some of this is due to cost, but another major factor is lack of access—the care is located far from where they live or work and there is a lack of accessible and affordable transportation. An increasing number of new tools, solutions, and business models are focused on addressing these issues to allow medical treatment to be delivered in a more efficacious manner, increasing the number of people able to access high-quality, affordable care.2 Secular tailwinds have been a catalyst to change how healthcare solutions are developed and delivered, including the forward adoption of telehealth solutions.

In education and workforce development, the current supply-demand mismatch in the labor market is only expected to widen in the coming years due to automation and digitization.3 As this happens, many pathways—from early childcare and K-12 education, to post-secondary schooling, through to corporate training—will be required to supply the future labor force that the economy will need, particularly in highly technical areas. While the need is significant, the US federal government has announced billions of dollars in funding to support workforce initiatives,4 and private companies have made significant in-house investment and/or partnered with educational institutions to develop educational programs.5

For underserved populations, healthcare and education services often are inaccessible due to high costs or lack of access/proximity; however, access to basic financial services and products that have become a requirement to fully participate in the economy continues to elude many Americans. Financial technology (FinTech) is one of the fast-growing areas for venture capital investment, averaging more than 2,000 deals and $80 billion of investment annually over the last three years.6 Fintech has the ability to democratize access to finance given its potential to lower costs, increase speed and accessibility, and allow for more tailored financial services.7 But given the history of financial service providers steering vulnerable populations to extractive products, as well as the increasing use of potentially-biased algorithms and data to drive these businesses, a sustainable investing lens is required to ensure that the most underserved populations are not exploited.

What is your response to investors who assume inclusive growth investing is concessionary?

Shell: While many investors still assume that accessing the inclusive growth space requires a concessionary approach, over the last decade annual startup investment by inclusive growth funds seeking market-rate returns has steadily increased from about $2 billion to about $20 billion in recent years.8 We have conviction that market-rate returns are not only possible to achieve for inclusive growth, but that the strategy is advantaged relative to more generalist strategies. The large addressable markets and secular-trend growth of the sub-themes offer potentially attractive opportunities. In addition, the business models that we’re looking for tend to deliver above-average profitability and cash-generating characteristics due to the large ecosystem of payors—including federal programs and agencies, governments, insurers, and private businesses—that are willing and able to fund initiatives to meet the needs of underserved populations.

We believe that success in the space will require not only domain expertise and deep knowledge of sustainable themes, but also significant operational resources and value creation capabilities to scale businesses. In addition to the traditional private equity toolkit, we will look to catalyze value creation by driving broad-based employee ownership while improving job quality and employee wellness. Together, we believe that these activities will help us to drive attractive returns, support companies to become leaders in their various industries, and deliver significant and measurable impact to all stakeholders.

Widening inequality pushes down aggregate demand and results in underinvestment in human capital, damaging productivity by shrinking capacity for innovation. Many motivated stakeholders, including large corporates as well as the public sector, recognize the material costs of inequality, such as a shortage of skilled labor, sub-optimal productivity, and chronic health conditions. However, they have historically lacked viable options to address the pain points and shortcomings. Private capital provides the bridge between these two large groups by investing in innovative companies that improve outcomes by driving accessibility, affordability, and quality services. We believe the inclusive growth theme—centered on increasing accessibility and affordability of fundamental goods and services—has matured in recent years due to heightened focus, increasing institutionalization, and an initial wave of private capital investment that is leading to technological developments and commercial innovation.

Source: Goldman Sachs Asset Management. For illustrative purposes only.

The cycle of inequality is exacerbated by systemic barriers to healthcare, education, and financial services, which requires a comprehensive approach that is accessible, innovative, and affordable. Here are a few examples of potential commercial solutions:

| Needs & Drivers | Potential Investment Examples |

|---|---|

Maternity Care Deserts in the US Continue to Grow

Maternity care deserts are increasing, especially in rural areas of the US, and disproportionately impact underserved women.9 Lack of access to high quality maternal care leads to worse clinical outcomes (e.g., maternal & infant mortality, c-sections, NICU admissions, etc.) with higher associated costs for patients, hospitals, health systems, and payors. Hospitals and payors are increasingly investing in preventative measures to mitigate maternal health risks and reduce costs. |

Maternal Care / OB-GYN-Focused Provider Enablement Platform

Platform focused on maternal health providers and OB-GYNs that provides technology, resources, and contracts to reduce administrative burden and improve patient outcomes. |

COVID-19 Exacerbated the Existing US Mental Health Crisis

COVID-19 exacerbated the US mental health crisis. More than a third of Americans reported symptoms of anxiety or depression in June 2022 vs. 11% in 2019, yet high out-of-pocket costs and provider shortages prevent many from receiving the care they need.10 One in four Americans choose between mental health treatment and paying for daily necessities, and more than two-thirds of Americans live in an area with a shortage of mental health professionals.11,12 Likewise, US health systems have more patients in need of mental health referrals than available providers in their communities; their inability to direct patients to providers, in turn, drives high rehospitalization rates and associated costs for patients with serious mental illness. |

Virtual Mental Health Care

Virtual mental health platform that provides comprehensive care across age and acuity spectrum, accepts commercial and government insurance, and trains providers. |

For illustrative purposes only. Not representative of any actual, or contemplated, investments.

| Needs & Drivers | Potential Investment Examples |

|---|---|

Supply-Demand Mismatch in the Labor Market

Businesses are having difficulty hiring technology workforce today and are concerned about decreasing levels of retention. Employees increasingly value employer-offered opportunities to upskill and reskill themselves, especially as some job functions are expected to be automated in the future. Driven by the need for talent and to improve retention, businesses are spending more on learning & development, but due to a lack of internal capacity to provide workforce training efficiently and effectively, businesses are increasingly outsourcing to workforce training companies with proven track records. |

Technology Workforce Training

A company that provides technology workforce training solutions that help employers and governments to source and train as well as to upskill and reskill existing employees. |

Increased Government Funding Available to Address Increasing Achievement Gaps in K-12 Students

The COVID-19 pandemic erased more than 20 years of progress on the Nation’s Report Card assessments, with the impact on underserved students much more severe.13 While the Elementary and Secondary School Emergency Relief Fund allocated $130 billion to schools and districts to support the safe reopening of schools and address student needs,14 many school districts across the US are struggling to retain or find teachers. This is increasing the demand for solutions to supplement the core curriculum, especially targeting students who are falling behind. |

K-12 Supplemental Curriculum Provider

A company that develops an evidence-based supplemental reading curriculum and connects teachers or tutors to assist students who are falling behind to deliver it, paid for by the school districts. |

For illustrative purposes only. Not representative of any actual, or contemplated, investments.

| Needs & Drivers | Potential Investment Examples |

|---|---|

Limitations of Traditional Underwriting Models

Traditional credit underwriting models have difficulty underwriting the 49 million Americans without credit scores, impairing lenders’ addressable market. Lenders see value in alternative underwriting models that have the potential to enhance credit decision-making at a lower cost, enabling them to profitably extend responsible and fair credit access to historically underserved consumers. However, many AI-driven models risk noncompliance with the Equal Credit Opportunity Act.15 |

AI-Enabled Alternative Underwriting

AI-driven credit underwriting SaaS platform that helps lenders identify and mitigate biases in the credit underwriting process, leading to increased credit quality and profitability for lenders while maintaining fair lending compliance. |

Costs of Poor Employee Financial Health

Employee financial wellbeing is top of mind for companies and HR leaders across the US. Employees who experience financial stress are far less productive than peers who feel confident in their financial situation—costing employers an estimated 13-18% in annual salary on average.16 In an effort to attract quality talent and combat employee attrition, 84% of employers are deploying resources to financial wellness tools.17 |

Employee Financial Wellness

Business-to-business-to-consumer (B2B2C) platform providing financial wellness programs as an employee benefit, including financial coaching, employer-sponsored savings plans and 0% APR emergency loans, improving employee productivity, job satisfaction and retention. |

For illustrative purposes only. Not representative of any actual, or contemplated, investments.

Committed to providing you with the insights you need to build your practice.

1 Goldman Sachs Global Investment Research, 2023.

2 Goldman Sachs Global Investment Research. 2023

3 McKinsey Global Institute Global Automation Impact Model. 2022.

4 The White House, “FACT SHEET: White House Announces over $40 Billion in American Rescue Plan Investments in Our Workforce – With More Coming” As of July 12, 2022.

5 US News and World Report, “Companies Invest in Partnerships, Workforce Training to Bridge Skills Gap” As of February 20, 2020.

6 PitchBook. As of 2022.

7 World Bank – On Fintech and Financial Inclusion, 2021

8 PitchBook. As of 2022.

9 March of Dimes, Maternity Care Deserts Report 2022. As of December 2022.

10 Association of American Medical Colleges - A growing psychiatrist shortage and an enormous demand for mental health services, 2022.

11 Cohen Veterans Network & National Council for Behavioral Health - America’s Mental Health, 2018.

12 Association of American Medical Colleges Research & Action Institute - Exploring Barriers to Mental Health Care in the U.S. 2022.

13 McKinsey: COVID-19 Learning Delay and Recovery: Where do US States Stand?, January 11, 2023.

14 US Department of Education, As of 2023.

15 CFPB – Adverse Action Notification Requirements in Connection with Credit Decisions Based on Complex Algorithms, May 26, 2022

16 Salary Finance – Inside the Wallets of Working Americans. As of February 2023.

17 BofA – 2022 Workplace Benefits Report, February 2022.

Glossary

Payors: federal programs and agencies, governments, and private businesses that fund healthcare, education, and financial services

Concessionary: an investment that accepts a lower return to achieve social impact

Market-rate: an investment intended to deliver the target (i.e., market) return for a given strategy

Risk Considerations

All investing involves risk, including loss of principal.

Private equity investments are speculative, highly illiquid, involve a high degree of risk, have high fees and expenses that could reduce returns, and subject to the possibility of partial or total loss of fund capital; they are, therefore, intended for experienced and sophisticated long-term investors who can accept such risks.

Alternative Investments often engage in leverage and other investment practices that are extremely speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested. There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. Similarly, interests in an Alternative Investment are highly illiquid and generally are not transferable without the consent of the sponsor, and applicable securities and tax laws will limit transfers.

Investors should also consider some of the potential risks of alternative investments:

- Alternative Strategies. Alternative strategies often engage in leverage and other investment practices that are speculative and involve a high degree of risk. Such practices may increase the volatility of performance and the risk of investment loss, including the entire amount that is invested.

- Manager experience. Manager risk includes those that exist within a manager’s organization, investment process or supporting systems and infrastructure. There is also a potential for fund-level risks that arise from the way in which a manager constructs and manages the fund.

- Leverage. Leverage increases a fund’s sensitivity to market movements. Funds that use leverage can be expected to be more “volatile” than other funds that do not use leverage. This means if the investments a fund buys decrease in market value, the value of the fund’s shares will decrease by even more.

- Counterparty risk. Alternative strategies often make significant use of over- the- counter (OTC) derivatives and therefore are subject to the risk that counterparties will not perform their obligations under such contracts.

- Liquidity risk. Alternatives strategies may make investments that are illiquid or that may become less liquid in response to market developments. At times, a fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all.

- Valuation risk. There is risk that the values used by alternative strategies to price investments may be different from those used by other investors to price the same investments.

Infrastructure investments are susceptible to various factors that may negatively impact their businesses or operations, including regulatory compliance, rising interest costs in connection with capital construction, governmental constraints that impact publicly funded projects, the effects of general economic conditions, increased competition, commodity costs, energy policies, unfavorable tax laws or accounting policies and high leverage.

Alternative Investments - Hedge funds and other private investment funds (collectively, “Alternative Investments”) are subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains and an individual’s net returns may differ significantly from actual returns. Such fees may offset all or a significant portion of such Alternative Investment’s trading profits. Alternative Investments are not required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of such Alternative Investments.

Investments in real estate companies, including REITs or similar structures are subject to volatility and additional risk, including loss in value due to poor management, lowered credit ratings and other factors.

Alternative investments are suitable only for sophisticated investors for whom such investments do not constitute a complete investment program and who fully understand and are willing to assume the risks involved in Alternative Investments. Alternative Investments by their nature, involve a substantial degree of risk, including the risk of total loss of an investor’s capital.

The above are not an exhaustive list of potential risks. There may be additional risks that are not currently foreseen or considered.

Conflicts of Interest

There may be conflicts of interest relating to the Alternative Investment and its service providers, including Goldman Sachs and its affiliates. These activities and interests include potential multiple advisory, transactional and other interests in securities and instruments that may be purchased or sold by the Alternative Investment. These are considerations of which investors should be aware and additional information relating to these conflicts is set forth in the offering materials for the Alternative Investment. A fund, underlying funds, and/or portfolio assets may utilize leverage which could have significant adverse consequences. In particular, a fund will lose its investment in a leveraged portfolio investment more quickly than a non-leveraged portfolio investment if the portfolio investment declines in value. Money borrowed for the purpose of leveraging investments will also be subject to interest costs as well as financing, transaction and other fees and costs that may not be recovered. You should understand fully the risks associated with the use of leverage before making an investment in a fund.

General Disclosures

The views expressed herein are as August 1, 2023 and subject to change in the future. Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security, they should not be construed as investment advice.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

Examples are for illustrative purposes only and are not actual results. If any assumptions used do not prove to be true, results may vary substantially.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

THESE MATERIALS ARE PROVIDED SOLELY ON THE BASIS THAT THEY WILL NOT CONSTITUTE INVESTMENT ADVICE AND WILL NOT FORM A PRIMARY BASIS FOR ANY PERSON’S OR PLAN’S INVESTMENT DECISIONS, AND GOLDMAN SACHS IS NOT A FIDUCIARY WITH RESPECT TO ANY PERSON OR PLAN BY REASON OF PROVIDING THE MATERIAL OR CONTENT HEREIN. PLAN FIDUCIARIES SHOULD CONSIDER THEIR OWN CIRCUMSTANCES IN ASSESSING ANY POTENTIAL INVESTMENT COURSE OF ACTION.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. It should not be assumed that investment decisions made in the future will be profitable or will equal the performance of the securities discussed in this publication.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the portfolio will achieve similar results. The index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark.

This material represents the views of Goldman Sachs Asset Management. It is not financial research or a product of Goldman Sachs Global Investment Research (GIR). It was not a product nor financial research of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed herein may vary significantly from those expressed by GIR or any other groups at Goldman Sachs. Investors are urged to consult with their financial advisers before buying or selling any securities. The information contained herein should not be relied upon in making an investment decision or be construed as investment advice. Goldman Sachs Asset Management has no obligation to provide any updates or changes.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

European Economic Area (EEA):This material is a financial promotion disseminated by Goldman Sachs Bank Europe SE, including through its authorised branches ("GSBE"). GSBE is a credit institution incorporated in Germany and, within the Single Supervisory Mechanism established between those Member States of the European Union whose official currency is the Euro, subject to direct prudential supervision by the European Central Bank and in other respects supervised by German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufischt, BaFin) and Deutsche Bundesbank.

Switzerland: For Qualified Investor use only – Not for distribution to general public. This is marketing material. This document is provided to you by Goldman Sachs Bank AG, Zürich. Any future contractual relationships will be entered into with affiliates of Goldman Sachs Bank AG, which are domiciled outside of Switzerland. We would like to remind you that foreign (Non-Swiss) legal and regulatory systems may not provide the same level of protection in relation to client confidentiality and data protection as offered to you by Swiss law.

Asia excluding Japan: Please note that neither Goldman Sachs Asset Management (Hong Kong) Limited (“GSAMHK”) or Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H ) (“GSAMS”) nor any other entities involved in the Goldman Sachs Asset Management business that provide this material and information maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, India and China. This material has been issued for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited, in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H) and in or from Malaysia by Goldman Sachs (Malaysia) Sdn Berhad (880767W).

This material is distributed in New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978, fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA),and fall within the definition of a wholesale investor under one of clause 37, clause 38, clause 39 or clause 40 of Schedule 1 of the Financial Markets Conduct Act 2013 (FMCA) of New Zealand (collectively, a “NZ Wholesale Investor”). GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person is a NZ Wholesale Investor. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA.

Australia: This material is distributed by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (‘GSAMA’) and is intended for viewing only by wholesale clients for the purposes of section 761G of the Corporations Act 2001 (Cth). This document may not be distributed to retail clients in Australia (as that term is defined in the Corporations Act 2001 (Cth)) or to the general public. This document may not be reproduced or distributed to any person without the prior consent of GSAMA. To the extent that this document contains any statement which may be considered to be financial product advice in Australia under the Corporations Act 2001 (Cth), that advice is intended to be given to the intended recipient of this document only, being a wholesale client for the purposes of the Corporations Act 2001 (Cth). Any advice provided in this document is provided by either of the following entities. They are exempt from the requirement to hold an Australian financial services licence under the Corporations Act of Australia and therefore do not hold any Australian Financial Services Licences, and are regulated under their respective laws applicable to their jurisdictions, which differ from Australian laws. Any financial services given to any person by these entities by distributing this document in Australia are provided to such persons pursuant to the respective ASIC Class Orders and ASIC Instrument mentioned below.

- Goldman Sachs Asset Management, LP (GSAMLP), Goldman Sachs & Co. LLC (GSCo), pursuant ASIC Class Order 03/1100; regulated by the US Securities and Exchange Commission under US laws.

- Goldman Sachs Asset Management International (GSAMI), Goldman Sachs International (GSI), pursuant to ASIC Class Order 03/1099; regulated by the Financial Conduct Authority; GSI is also authorized by the Prudential Regulation Authority, and both entities are under UK laws.

- Goldman Sachs Asset Management (Singapore) Pte. Ltd. (GSAMS), pursuant to ASIC Class Order 03/1102; regulated by the Monetary Authority of Singapore under Singaporean laws

- Goldman Sachs Asset Management (Hong Kong) Limited (GSAMHK), pursuant to ASIC Class Order 03/1103 and Goldman Sachs (Asia) LLC (GSALLC), pursuant to ASIC Instrument 04/0250; regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws

No offer to acquire any interest in a fund or a financial product is being made to you in this document. If the interests or financial products do become available in the future, the offer may be arranged by GSAMA in accordance with section 911A(2)(b) of the Corporations Act. GSAMA holds Australian Financial Services Licence No. 228948. Any offer will only be made in circumstances where disclosure is not required under Part 6D.2 of the Corporations Act or a product disclosure statement is not required to be given under Part 7.9 of the Corporations Act (as relevant).

Canada: This presentation has been communicated in Canada by GSAM LP, which is registered as a portfolio manager under securities legislation in all provinces of Canada and as a commodity trading manager under the commodity futures legislation of Ontario and as a derivatives adviser under the derivatives legislation of Quebec. GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts in Manitoba and is not offering to provide such investment advisory or portfolio management services in Manitoba by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

South Africa: Goldman Sachs Asset Management International is authorised by the Financial Services Board of South Africa as a financial services provider.

Malaysia: This material is issued in or from Malaysia by Goldman Sachs (Malaysia) Sdn Bhd (880767W)

Hong Kong: This material has been issued or approved for use in or from Hong Kong by Goldman Sachs Asset Management (Hong Kong) Limited.

Singapore: This material has been issued or approved for use in or from Singapore by Goldman Sachs Asset Management (Singapore) Pte. Ltd. (Company Number: 201329851H).

Israel: This document has not been, and will not be, registered with or reviewed or approved by the Israel Securities Authority (ISA”). It is not for general circulation in Israel and may not be reproduced or used for any other purpose. Goldman Sachs Asset Management International is not licensed to provide investment advisory or management services in Israel.

Jordan: The document has not been presented to, or approved by, the Jordanian Securities Commission or the Board for Regulating Transactions in Foreign Exchanges.

Colombia: Esta presentación no tiene el propósito o el efecto de iniciar, directa o indirectamente, la adquisición de un producto a prestación de un servicio por parte de Goldman Sachs Asset Management a residentes colombianos. Los productos y/o servicios de Goldman Sachs Asset Management no podrán ser ofrecidos ni promocionados en Colombia o a residentes Colombianos a menos que dicha oferta y promoción se lleve a cabo en cumplimiento del Decreto 2555 de 2010 y las otras reglas y regulaciones aplicables en materia de promoción de productos y/o servicios financieros y /o del mercado de valores en Colombia o a residentes colombianos. Al recibir esta presentación, y en caso que se decida contactar a Goldman Sachs Asset Management, cada destinatario residente en Colombia reconoce y acepta que ha contactado a Goldman Sachs Asset Management por su propia iniciativa y no como resultado de cualquier promoción o publicidad por parte de Goldman Sachs Asset Management o cualquiera de sus agentes o representantes. Los residentes colombianos reconocen que (1) la recepción de esta presentación no constituye una solicitud de los productos y/o servicios de Goldman Sachs Asset Management, y (2) que no están recibiendo ninguna oferta o promoción directa o indirecta de productos y/o servicios financieros y/o del mercado de valores por parte de Goldman Sachs Asset Management.

Esta presentación es estrictamente privada y confidencial, y no podrá ser reproducida o utilizada para cualquier propósito diferente a la evaluación de una inversión potencial en los productos de Goldman Sachs Asset Management o la contratación de sus servicios por parte del destinatario de esta presentación, no podrá ser proporcionada a una persona diferente del destinatario de esta presentación.

United Kingdom: In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Bahrain: This material has not been reviewed by the Central Bank of Bahrain (CBB) and the CBB takes no responsibility for the accuracy of the statements or the information contained herein, or for the performance of the securities or related investment, nor shall the CBB have any liability to any person for damage or loss resulting from reliance on any statement or information contained herein. This material will not be issued, passed to, or made available to the public generally.

Kuwait: This material has not been approved for distribution in the State of Kuwait by the Ministry of Commerce and Industry or the Central Bank of Kuwait or any other relevant Kuwaiti government agency. The distribution of this material is, therefore, restricted in accordance with law no. 31 of 1990 and law no. 7 of 2010, as amended. No private or public offering of securities is being made in the State of Kuwait, and no agreement relating to the sale of any securities will be concluded in the State of Kuwait. No marketing, solicitation or inducement activities are being used to offer or market securities in the State of Kuwait.

Oman: The Capital Market Authority of the Sultanate of Oman (the "CMA") is not liable for the correctness or adequacy of information provided in this document or for identifying whether or not the services contemplated within this document are appropriate investment for a potential investor. The CMA shall also not be liable for any damage or loss resulting from reliance placed on the document.

Qatar This document has not been, and will not be, registered with or reviewed or approved by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or Qatar Central Bank and may not be publicly distributed. It is not for general circulation in the State of Qatar and may not be reproduced or used for any other purpose.

Saudi Arabia: The Capital Market Authority does not make any representation as to the accuracy or completeness of this document, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this document. If you do not understand the contents of this document you should consult an authorised financial adviser.

The CMA does not make any representation as to the accuracy or completeness of these materials, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of these materials. If you do not understand the contents of these materials, you should consult an authorised financial adviser.

United Arab Emirates: This document has not been approved by, or filed with the Central Bank of the United Arab Emirates or the Securities and Commodities Authority. If you do not understand the contents of this document, you should consult with a financial advisor.

Cambodia: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds) or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer or investment advisor under The Securities and Exchange Commission of Cambodia. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

Vietnam: Please Note: The attached information has been provided at your request for informational purposes only. The attached materials are not, and any authors who contribute to these materials are not, providing advice to any person. The attached materials are not and should not be construed as an offering of any securities or any services to any person. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed as a dealer under the laws of Vietnam. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person without the prior consent of Goldman Sachs Asset Management.

East Timor: Please Note: The attached information has been provided at your request for informational purposes only and is not intended as a solicitation in respect of the purchase or sale of instruments or securities (including funds), or the provision of services. Neither Goldman Sachs Asset Management (Singapore) Pte. Ltd. nor any of its affiliates is licensed under any laws or regulations of Timor-Leste. The information has been provided to you solely for your own purposes and must not be copied or redistributed to any person or institution without the prior consent of Goldman Sachs Asset Management.

Confidentiality

No part of this material may, without Goldman Sachs Asset management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director or authorized agent of the recipient.

Date of First Use: August 7, 2023 329016-OTU-1848494