The Mona Lisa is universally regarded as one of the most renowned works of art, yet one question has sparked a chasmic divide across the spectrum of art enthusiasts: is she smiling? How one perceives her expression is dictated by which cells in the retina view the image and through what neural pathway that image is transmitted to the brain. In other words, Mona Lisa’s smile, like the state of the global economy, is entirely dependent on the lens that one views it through.

Many of the world’s central banks have cooled inflation measurably without recessionary growth shocks, and a return

to respective inflation targets is possible in 2024. Still, mixed signals, such as positive earnings expectations at odds with an inverted yield curve, foster a wide dispersion of macro views. Through a balanced assessment of the full picture, we believe the hard part is over.

Importantly, our optimism around the avoidance of a global recession should not be confused with a full risk-on tilt. Rather, a balanced portfolio of equities, fixed income, and alternatives may serve as a hedge to inflation and growth risks, while maintaining robust return targets. We expect 2024 to mark the beginning of the return to a normalized investing environment.

In this edition of the Market Know-How, we explore how investors may capitalize on a resilient macro backdrop while also accounting for tail risks, with emphasis on:

- Navigating a higher interest rate regime with balanced equity and core fixed income positioning.

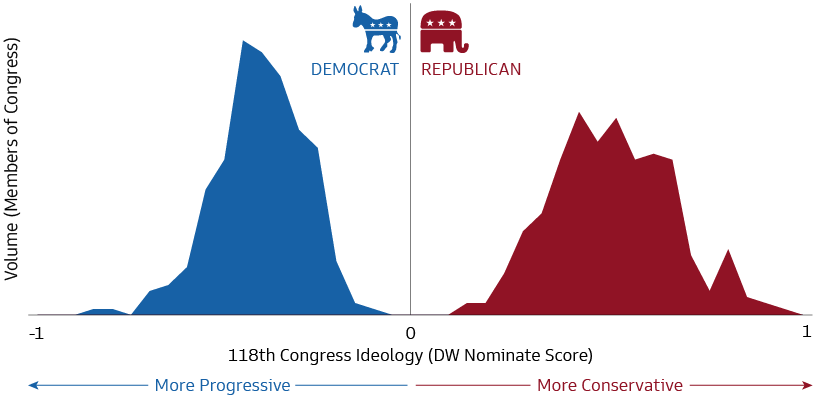

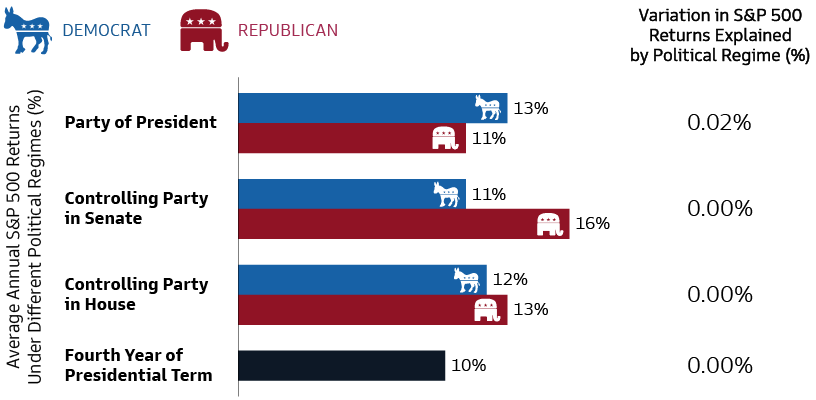

- Positioning for a potentially turbulent US election year that may feature heightened market volatility.

- Adding the potential risk-reduction benefits of liquid alternatives while maintaining competitive return targets.