Relief valves are one of the most important components of pressurized systems, controlling for excess strains that are caused by fluctuations in operating conditions. Their utility becomes especially apparent as conditions become less predictable. Macro policy and market dynamics can also create conditions where excesses emerge and should be addressed. Global inflation elicited aggressive monetary responses, which led to higher interest rates and, in turn, slowed growth. Meanwhile, higher short-term rates and elevated cost of capital have intensified demand for reliably profitable companies, embodied by the Magnificent 7, and money market funds, which experienced a 46% year-over-year increase in flows.

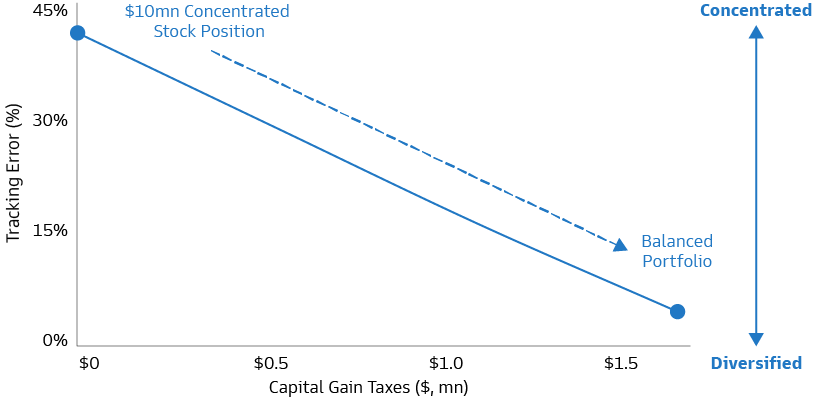

Today, we see two very common shortfalls in portfolio exposure: 1) high cash balances, that may provide excellent liquidity but often leave investors underinvested in risk assets during a favorable macro backdrop, and 2) burgeoning concentrated stock exposures, reflecting extremely narrow stock market leadership. We believe each of these pressures can be actively and efficiently relieved through tactful portfolio design and investment strategy.

In this edition of the Market Know-How, we consider how investors may relieve the pressures of excess cash and single stock concentration by:

- Using exchange funds to swap large single stock positions for a diversified basket without triggering a capital gains tax.

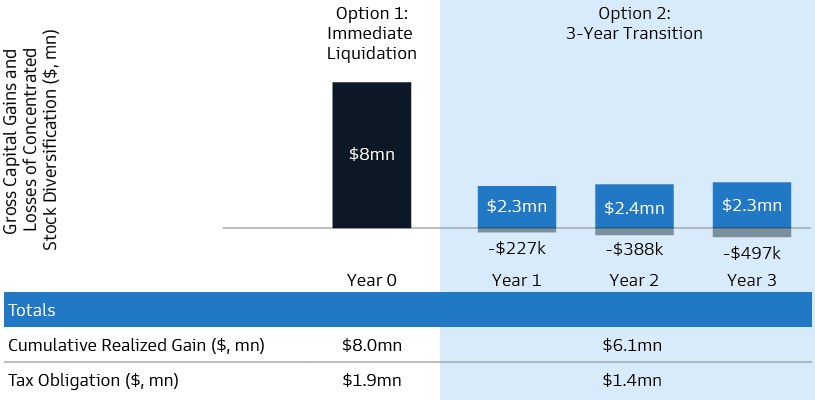

- Transitioning concentrated positions into liquid, diversified portfolios in a tax-efficient manner via tax-advantaged SMAs.

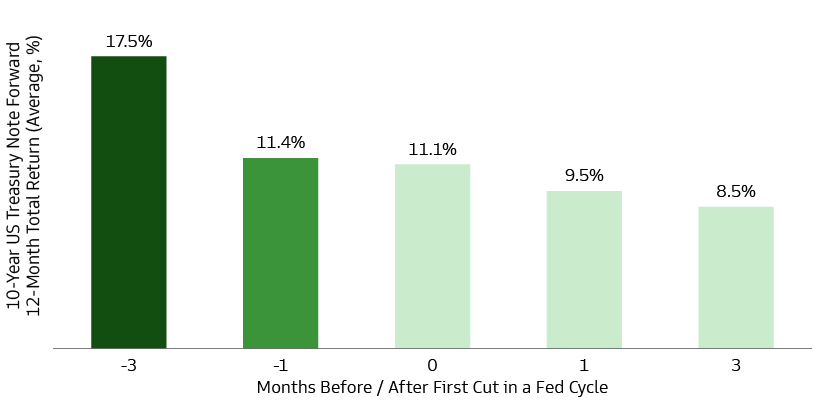

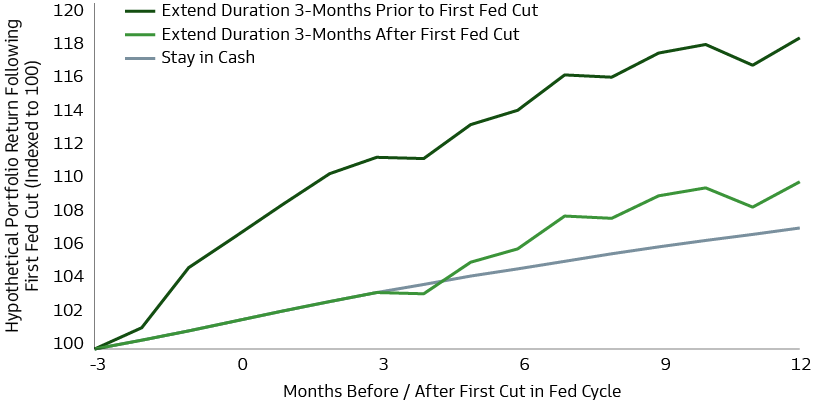

- Extending duration to exploit hedging capacity and low costs of being early with potential Fed cuts on the horizon.